The chief executive of a European equipment manufacturer recently faced a tough centralization decision: should he combine product management for the company’s two business units—cutting and welding—which operated largely independently of each other but shared the same brand? His technical leader believed that an integrated product range would make the company’s offerings more appealing to businesses that bought both types of equipment. These customers accounted for more than 70 percent of the market but less than 40 percent of the company’s sales. “You cut before you weld,” he explained. “You get a better weld at lower cost if the cutting is done with the welding in mind.” Managers in both divisions, though, resisted fiercely: product management, they believed, was central to their business, and they could not imagine losing control of it.

The CEO’s dilemma—were the gains of centralization worth the pain it could cause?—is a perennial one. Business leaders dating back at least to Alfred Sloan, who laid out GM’s influential philosophy of decentralization in a series of memos during the 1920s, have recognized that badly judged centralization can stifle initiative, constrain the ability to tailor products and services locally, and burden business divisions with high costs and poor service.1 Insufficient centralization can deny business units the economies of scale or coordinated strategies needed to win global customers or outperform rivals.

Timeless as the tug-of-war between centralization and decentralization is, it remains a dilemma for most companies. We heard that point loud and clear in some 50 interviews we conducted recently with heads of group functions at more than 30 global companies. These managers had found that the normal financial and strategic analyses used for making most business decisions do not resolve disagreements about, for example, whether to impose a group-wide performance-management system. What’s more, none of the executives volunteered an orderly, analytical approach for resolving centralization decisions. In its absence, many managers fall back on benchmarks, politics, fashion—sometimes centralization is in vogue and sometimes decentralization is—or instinct. One head of IT, for example, explained that in his experience the lowest-cost solution was always decentralization. Another argued the opposite.

To help senior managers make better choices about what to centralize and what to decentralize, we have been refining a decision-making framework based on our research and experiences in the corporate trenches. It is embodied in three questions that can help stimulate new proposals, keep emerging ones practical, and turn political turf battles into productive conversations.

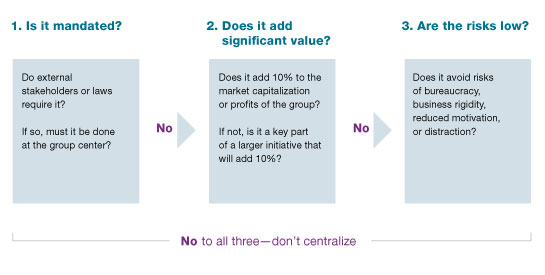

Three questions

Each question defines a hurdle that a centralization proposal must meet. A decision to centralize requires a yes to at least one of them. While the questions set a high bar for centralization, they do not produce formulaic answers; considerable judgment is still required. They benefit companies by allowing advocates and opponents of centralization to conduct a debate in a way that helps CEOs and their senior teams make wiser choices. The questions can be asked in any order, but the one presented here is often natural to follow (exhibit).

A decision to centralize requires a yes to at least one of three questions.

Is centralization mandated?

The first step is to ask whether the company has a choice. A corporation’s annual report and consolidated accounts, for example, are required by law and must be signed by the CEO, so it is impossible to delegate this task to the business divisions. In this case, the answer is yes to centralization.

By contrast, centralization is not essential for compliance with health and safety laws; each division can manage its own compliance. So a proposal to appoint a head of group health and safety would get a no for this question and would need a yes from question two or three.Does centralization add significant value—10 percent?

If centralization is not mandated, it should be adopted only if it adds significant value. The problem, however, as illustrated by the product-management example, is how to judge whether it will do so. This point is particularly difficult because corporate strategies rarely provide clarity about the major sources of additional value that underpin the argument for bringing different business activities together in a group. The solution, we find, is to set a hurdle high enough so that the benefits of centralization will probably far outweigh the disadvantages, making the risks worth taking.

Specifically, we suggest asking: “Does the proposed initiative add 10 percent to the market capitalization or profits of the corporation?” This hurdle is sufficiently high to make it difficult for advocates of centralization to “game” the analysis, and thus saves the top team’s time by quickly eliminating small opportunities from discussion. Start by considering whether the activity meets the 10 percent hurdle on its own. If not, which is most often the case, you should assess whether it is a necessary part of some larger initiative that will meet the 10 percent hurdle. In practice, the answer to the 10 percent question does not require fine-grained calculations. What is required are judgments about the significance of the activity, either on its own or as part of a larger initiative.Are the risks low?

Most centralization proposals will not pass either of the two previous hurdles: they will not be mandated and will not represent major sources of additional value. More often, the prize will be smaller improvements in costs or quality. In these cases, the risks associated with centralization—business rigidity, reduced motivation, bureaucracy, and distraction—are often greater than the value created. Hence, the proposals should go forward only if the risks of these negative side effects are low.

An initiative to centralize payroll is likely to get a yes on this hurdle. Costs can clearly be saved through economies of scale, and the risks of negative side effects are low. Payroll operations are not important to the commercial flexibility of individual business units, nor are their managers likely to feel less motivated by losing control of payroll. Moreover, the risks of bureaucratic inefficiency and distraction can be reduced to a minimum if the payroll unit is led by a competent expert who reports to the head of shared services and doesn’t take up the time of finance or HR leaders.

Any centralization proposal that does not survive at least one of our three questions should be abandoned or redesigned. To see how our approach works in practice, let’s look at two companies that recently applied it—starting with the automated cutting- and welding-equipment manufacturer, which we’ll call European Automation.

In practice: European Automation’s product-management problem

Since centralized product management was clearly not mandated, the centralization proposal failed the first test. The CEO then skipped to the third test— is the risk of negative side effects low?—and quickly concluded that it wasn’t. Centralization would reduce commercial flexibility. Moreover, it could make managers in the businesses less motivated, since they would lose authority over an activity they considered important. And if done badly, centralized product management could lead to delays, additional costs, and uncompetitive products.

So the proposal would succeed or fail on the second question—the 10 percent hurdle. The CEO sat down with the heads of the technical function and the two businesses (cutting and welding) to assess whether centralized product management could reasonably deliver an additional 10 percent in value through increased sales, higher prices, or some combination of both. (It was unlikely, in anyone’s estimation, to yield major cost savings.)

After considerable discussion based on estimates of likely profit margins and on additional sales volumes from customers who might be influenced by an integrated product range, the group judged that if the centralized product-management function was properly managed it could add 10 percent to the company’s performance. In other words, the opportunity was big enough to surmount the 10 percent hurdle.

Yet the business heads still resisted. The downside of getting it wrong, they argued, could make things worse rather than better. But the CEO, emboldened because the proposal passed the 10 percent hurdle, responded: “Well, all the more reason for us to work together to get it right. At our next meeting, let’s have a plan for how you are going to do this.”

Nearly two years later, European Automation’s centralization of product management has been largely successful: market share is up, and the product offerings of the cutting and welding units are better aligned. But this example also illustrates the hard work and real risks involved. The company had to replace some of its original product managers because they did not have the skills to understand both cutting and welding products. Also, with product managers reporting to the technical function rather than to business units, some new products have been technically strong but less tailored to market needs, and some product launches have been delayed. To solve these problems, the executive committee is reviewing product-development plans in more detail and asking for regular progress reports.

In practice: Extreme Logistics’ performance-management issue

Sometimes, addressing the three questions can spark meaningful conversations that take managers in unexpected—and beneficial—directions. This happened at a company we’ll call Extreme Logistics, a global provider of food services to drilling, mining, and other operations in out-of-the-way locations.

Anticipating slower growth and lower margins from increased competition, the company’s CEO asked the HR leader to consider imposing a single performance-management system on all of the five geographical divisions. Historically, each had its own. The CEO felt that a common one might enable him to have closer control of costs and management quality.

The head of HR proposed a centralized system that would link a balanced scorecard of metrics to incentives. Knowing that the CEO supported the initiative, skeptical division heads nodded the proposal through the concept stage. Once HR began to work out the details, however, vocal resistance emerged. One division head said he was prepared to “play the game” of this new system if he had to, but only to ensure that his people got the bonuses they deserved. Another worried that the system would undermine her management style, which was to “lead from the front rather than to treat people as units of accounting.”

To deal with the emerging political impasse, the CEO and the head of HR turned to the three questions. The initiative clearly did not qualify as a mandated item. It was also hard to see it as a major contributor to the key sources of value added by the corporate center. Management had recently identified these as encouraging entrepreneurial initiative, coordinating global customers, managing local governments, and centralizing common operating activities.

So, if the proposal was to get a yes to the second question, it would have to clear the 10 percent hurdle on its own. This, too, seemed unlikely. True, the CEO and HR head could imagine scenarios in which the hurdle could be met: a 5 percent cost reduction, plus a 10 percent improvement in the quality of managers, they reckoned, would suffice. Yet the pair ultimately concluded that a central performance-management system would hardly achieve such goals on its own.

Nonetheless, the discussion of scenarios prompted the CEO to consider other ways of achieving a significant cost reduction and an increase in management quality. He considered launching cost reduction projects and using existing business review meetings to create more demanding profit budgets and to monitor cost reduction plans, for example. With regard to management quality, the head of HR suggested developing a leadership program and setting targets for the businesses to improve or change the bottom 20 percent of their management talent.

Was a centralized performance-management system, with a balanced scorecard tied to incentives, essential to either a cost or management-quality campaign of the type the CEO and the head of HR were considering? They were inclined to think it was. But in discussions with some of the business presidents, the CEO and the HR head became convinced that most of what they wanted could be achieved without centralizing the performance-management system.

That conclusion led to the third question: how likely was a centralized performance-management system to cause negative side effects? The proposal failed this hurdle as well. Some of the business presidents thought it would make their managers less motivated. Moreover, the head of HR, the CEO, and the CFO all lacked experience running a system of the type proposed. Hence, it might become bureaucratic and distract the corporate center from the four areas that had previously been identified as places where it could add value, and from the two new initiatives—cost reduction and management-quality improvements—both of which are currently being evaluated to see if they meet the 10 percent hurdle.

Is centralization mandated? Can it add 10 percent to a corporation’s value? Can it be implemented without negative side effects? A proposal to centralize only needs a yes to one of these three questions. Yet they provide a high hurdle that helps managers avoid too much centralization. Moreover, they stimulate open and rational debate in this highly politicized area. By giving those in favor of centralization and those opposed to it a level playing field for building a case, these questions help companies strike the right balance between centralization and decentralization today and to evolve their organizations successfully as conditions change over time.