Talking about wealthy consumers in China may seem odd during the middle of a global economic crisis. Yet for many companies around the world, wealthy Chinese represent a rare opportunity in an otherwise dismal picture.

Despite the global downturn, the number of wealthy households in China continues to grow. By 2015, the country will hold the world’s fourth-largest concentration of wealthy people. Companies that better understand the factors behind their purchases could steal a march on the competition. Our research shows that their behavior is very different from that of their counterparts in other countries and of consumers in other income classes inside China.1 Indeed, the pool of luxury consumers has become large enough to form distinct segments, each with its own behavior and needs.

Our work included face-to-face interviews in 16 cities with 1,750 wealthy Chinese consumers—people in households earning more than $36,500 annually, which gives them the spending power of a US household making roughly $100,000 a year. These wealthy Chinese households, with an average annual income of about $80,000, represented the top 1 percent of earners in China’s cities. We supplemented the interviews with home visits by our researchers, who also accompanied many respondents on shopping trips. In addition, we talked with brand managers and marketing specialists in China who serve this sector, visited luxury brand stores, and conducted exit interviews there.

To succeed, marketers selling luxury brands or the premium end of mainstream brands must understand what makes these consumers pick one over another. Indeed, they vary sharply in their preferences: for example, some wealthy consumers in China are still looking for status labels, while others try not to display their wealth. Companies that fail to understand such distinctions could end up wasting millions in marketing dollars and missing big opportunities.

Big—and getting bigger

Even in the downturn, China remains one of the world’s few growth markets, with GDP expected to expand by 6 to 8 percent in 2009, according to official and private estimates. The crisis has affected all of the country’s income levels, however, and data on reactions to it remain inconclusive because the situation is changing so rapidly. Anecdotal evidence, particularly discussions with luxury marketers serving China, suggests strongly that spending by wealthy Chinese is growing more slowly but hasn’t dropped overall. Indeed, in early 2009 there were tentative signs that growth rates might be edging up again.

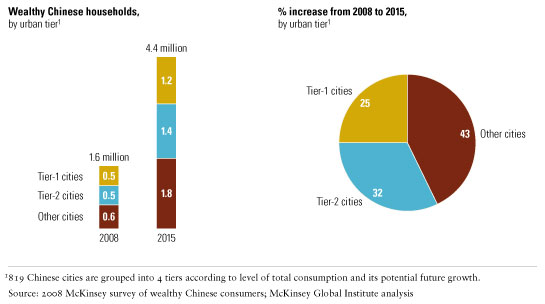

The number of China’s wealthy households, which hit 1.6 million in 2008, will climb to more than 4.4 million by 2015, trailing only the United States, Japan, and the United Kingdom in sheer size (with definitions of wealth adjusted for purchasing-power parity). Even allowing for the current economic slowdown, the number of wealthy households in China is likely to expand at an annual rate of about 16 percent for the next five to seven years.2 In developed markets, by contrast, this group is expected to grow largely in line with GDP.

To illustrate how quickly marketers must move to keep pace with China’s wealthy consumers, about half of the Chinese who are wealthy today weren’t four years ago, and more than half of those who will be wealthy in five to six years aren’t today. Spending habits can change quickly when a market grows so explosively. Only a few years ago, for example, Chinese consumers purchased most of their luxury goods outside the country. Today, they make 60 percent of these purchases in mainland China.

In such a fast-growing market, companies can do much to shape the taste, spending habits, and loyalty of consumers in a wide range of industries—automotive, real estate, banking services, consumer electronics, and other luxury consumer goods and services, for example. Over half of the wealthy Chinese consumers who now buy luxury fashion goods started doing so in the past four years, and only a minority can name as many as three luxury brands in any category.

As expected, a disproportionate number of China’s wealthy households currently live in its biggest and most developed cities, in the east and central south regions. China’s four richest cities—Shanghai, Beijing, Guangzhou, and Shenzhen—account for about 30 percent of all wealthy consumers; the top ten cities are home to some 50 percent of them. (By comparison, the top ten cities in the United States are home to only about 25 percent of its wealthy consumers.) But this concentration is changing.

Our research indicates that over the next five to seven years, three-quarters of the growth in the number of China’s wealthy consumers will occur outside the largest metropolises (Exhibit 1). Indeed, much of the growth will occur in the smaller second-tier cities, bringing them on par with the larger second-tier ones. The wealthy class will grow even in the next rung of cities, the third tier. Because many of these new wealthy will be entrepreneurs and other people with strong ties to the places where they live, we expect little migration to the largest cities as incomes rise.

Geographic evolution

This shift must force a change in approach for those marketers in China who still focus on Shanghai and Beijing, where competition is fiercest. Companies hoping to seize the full opportunity of the country’s growing number of wealthy households can’t overlook China’s smaller cities, as they often do today. Some of the biggest names in luxury goods have several retail outlets in Beijing, for instance, but are absent in places like Chengdu or Wenzhou, even though Chengdu has more wealthy consumers than Detroit, and Wenzhou has as many as Atlanta, where luxury outlets abound.

China’s wealthy are different

How best to target China’s wealthy consumers? If they decide to buy a watch or a leather bag, will they want a genuine high-end brand or be content with a look-alike? When the time comes to buy a car, are they more impressed by the endorsement of a young, glitzy celebrity or of an older, more sophisticated one? Are they more likely to buy a mobile phone deliberately positioned as a luxury brand?

Such questions weigh on the minds of marketers trying to reap profits from China’s wealthy consumers. For companies selling luxury brands in other markets, particularly developed ones, the key issue is how the rich in China differ from their counterparts elsewhere. Companies already catering to the mainstream in China and hoping to stretch their brands to the premium market must primarily understand how the country’s wealthy differ from other domestic income groups.

Our research shows that these differences abound. They will be critical for any brand targeted at wealthy Chinese.

Different from their global peers

One of the clearest factors distinguishing China’s wealthy consumers from their foreign counterparts is their youth: some 80 percent are under 45 years of age, compared with 30 percent in the United States and 19 percent in Japan. Because they are newer to the consumer market and to wealth, they are less knowledgeable about luxury brands. In addition, China’s wealthy value the functional benefits of any particular purchase (the quality, material, design, or craftsmanship, for instance) more than wealthy consumers elsewhere do. The emotional benefits of a purchase—what it says about its owner’s taste, for example—count, but for the moment they matter less than they do for consumers in developed markets.

Such differences have clear marketing implications. To capture younger consumers, for example, Lancôme emphasizes the importance of taking early action to prevent manifestations of aging when the company promotes its range of anti-aging skin care products in China. That approach significantly lifted sales among younger consumers, helping to make Lancôme the largest luxury cosmetics and skin care brand in the country. The manufacturer of the luxury cognac Louis XIII countered its low brand awareness by replacing its traditional ads, featuring luxury images such as pianos, horses, and yachts, with simpler ads that often focus solely on the bottle and packaging. Other brands acknowledge the Chinese consumer’s appreciation of functional benefits by emphasizing product quality. When the Italian fashion brand Ermenegildo Zegna, for example, opens stores in China, it conducts demonstrations of how its ties are made in order to emphasize the craftsmanship.

But there is also danger in radically changing a brand’s global positioning for the Chinese market. When the Swiss watchmaker Longines first came to China, in the 1980s, it launched a special, brasher product line meant to appeal to the country’s wealthy consumers. This line failed. The company’s vice president of marketing for China, Li Li, later explained that Chinese consumers felt suspicious when they discovered that Longines products offered in other countries were drastically different. In 1994, the company repositioned itself in China as a classic, elegant brand, in line with its global positioning, and today China is its largest market.

Different from other Chinese

Our research also shows that wealthy Chinese are very different from the country’s other consumers. The gap in attitudes and behavior is particularly stark when we compare them with the mainstream: for example, 52 percent of wealthy consumers said that they trusted foreign brands, compared with only 11 percent of mainstream ones. The wealthy also are more willing to try new technology, more amenable to borrowing, and more likely to have difficulty maintaining a satisfactory work–life balance.

Like Chinese consumers in general, the wealthy watch a lot of television: 77 percent of them—the highest percentage among all the activities cited. What’s more, they spend a good deal more time surfing the Internet than do members of other income groups. Such differences in leisure behavior are important to help marketers design the right media mix for reaching these consumers. Wealthy people also spend more time than others do outside their homes, engaging in sports, visiting health spas, and drinking and dining out. Indeed, the wealthy spend 17 percent of their household income dining out (compared with 7 percent for mainstream consumers) and 10 percent on leisure and entertainment (compared with 3 percent for the mainstream).

Such behavior not only confirms that television remains an important medium for reaching wealthy consumers but also suggests that Internet ads, blogs, and other online channels could have a greater impact on them than on other consumers. Companies should also bear in mind the amount of time that the wealthy spend outside their homes. Some premium whiskies, for example, hold marketing events in bars and clubs frequented by the wealthy, but more brands could take advantage of such opportunities. A wider range of sports sponsorships, beyond a focus on activities traditionally embraced by the wealthy, such as golf, could also help companies reach wealthy consumers. The watch maker Omega, for example, has been the leading sponsor of the Shanghai Golden Grand Prix.

Targeting the right wealthy

China’s wealthy consumers differ not only from their global peers and from other Chinese consumers but also from one another: as this attractive group has grown and continues to grow, stark differences have appeared within it. Marketers must understand them to take full advantage of the growth of these segments.

Easily obtained demographic information—age, gender, and income, for instance—offers little help in separating China’s wealthy into segments with differing attitudes toward, say, borrowing, fashion, or obvious displays of wealth. Wealthy Chinese may generally be younger than their global counterparts, for example, but their attitudes are shaped less by age than by other differences. The one exception to the relative unimportance of standard demographic data was location. Rather surprisingly, wealthy consumers living in the four largest cities have more conservative attitudes toward saving and are more focused on family than their peers in smaller cities. Less surprisingly, they are more trusting of foreign brands.

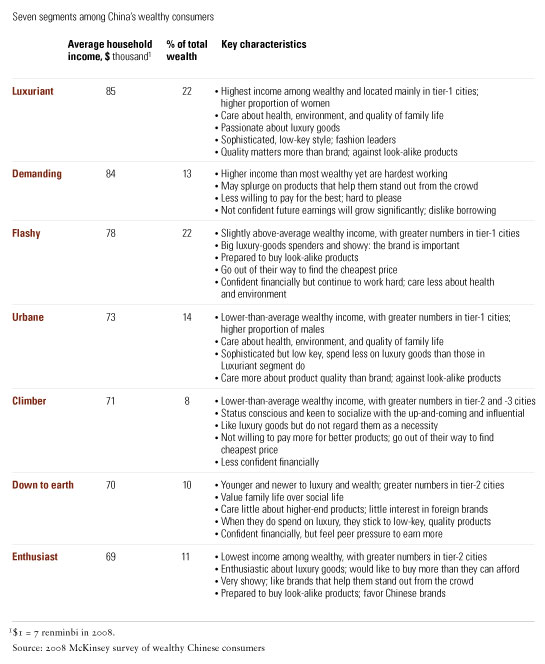

More meaningful differences emerged when we considered what respondents said about their needs—the need to feel unique, for example, or to feel financially secure. This needs-based analysis uncovered seven distinct segments among China’s wealthy consumers (Exhibit 2).

Seven segments

Consumers in the Luxuriant segment, for example, are among the country’s wealthiest people, passionate about luxury. They never settle for less than the best and gravitate toward high-end, high-fashion brands, such as Hermès and Chanel. These consumers are a brand’s best friend, buying frequently and talking with friends about their purchases. They avoid the brash—opting instead for understated, sophisticated chic—and are seen as trend setters. Although they work hard, they find time to socialize, travel, and be with their families and to visit gyms and health spas.

Compare this segment with the Demanding one: self-made men and women who have more money than they need and are satisfied with their success, although they still work hard. They don’t have a taste for luxury goods, especially fashion; rarely buy the very best; often content themselves with look-alikes; and make an effort to compare prices before buying, even at prices they can easily afford. When they do splurge, they like something flashy that sets them apart. In general, though, they settle for products that are more functional, less showy, such as televisions and sound systems.

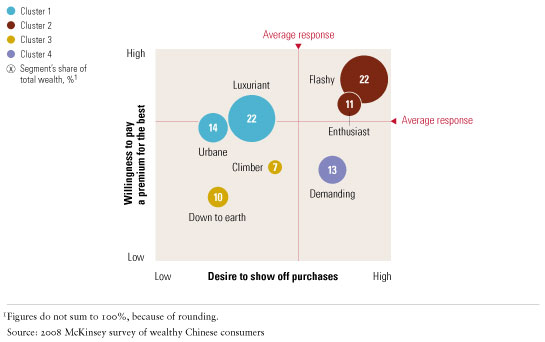

A company must also understand how the different segments relate to one another and craft strategies appealing to several of them to gain the greatest benefit from its efforts. Companies in most industries would gain, for example, from analyzing each segment according to the willingness of its members to pay a premium for what they regard as the best and their desire to flaunt their purchases, a characteristic we call “showiness.” Such an analysis, which groups the seven segments into four clusters (Exhibit 3), suggests, for example, that Chinese consumers in the two wealthiest are willing to pay a premium for what they regard as the best but that people in one cluster are more interested in showing off their purchases than people in the other.

Optimal impact

Together, the two largest clusters account for about 70 percent of the total wealth held by China’s wealthy consumers. This degree of economic importance means that these two will probably be the primary targets for many brands. Digging further, companies should also understand how the relative weight of each cluster varies among regions and among cities of different sizes and even within individual cities. For example, the cluster composed solely of Demanding consumers is much less important in the largest cities, where they account for about 10 percent of the wealth held by wealthy families, than in other cities, where they account for about 17 percent of it.

The weight of the clusters will change over time. Companies that want to build an early brand advantage will need to consider investing in segments that are relatively small today but will grow in importance. Over the next five to seven years, the fastest-growing cluster, for example, will consist of Climbers and Down-to-earth consumers, who live mostly in the fast-growing cities outside the big four.

For many brands, a better understanding of these clusters can lead to more effective marketing spending. Advertising, for instance, can be targeted at a number of segments within a cluster, because they share important attributes. Consumers in the Enthusiast and Flashy segments both tend to be willing to pay for the best and enjoy showing off what they buy. For them, brands matter and should be noticed; logos and marketing generally ought to be bold. And because these consumers are very attached to their favorite labels, brand extensions across consumer categories could pay off. Their intense brand knowledge makes them challenging customers, however: they insist on the latest products and styles and expect salespeople to reflect the brand image in appearance and behavior.

BMW, for example, has a brand position that would appeal to this cluster. The German carmaker offers its full line of products (with design changes catering to wealthy Chinese) and advertises them across a range of channels, such as glossy magazines, television, and the Internet, to create wide brand awareness. Annual BMW Experience Days rotating from city to city offer groups of buyers a first look at the coming year’s models, giving these customers a luxurious experience, along with an opportunity to test-drive the new cars.

Consumers in a separate cluster comprising the Luxuriant and Urbane segments, though also willing to pay more for the brands they prefer, are far less interested in showing off. They want the latest and the best from brands they like and are more loyal. Yet they place greater importance on the attributes of a product or service than on the glamour of brands.

Companies serving the cluster should offer a strong product line and excellent service, but for these customers the product must be less conspicuous and the marketing more subtle. VIP programs and special marketing events, such as previews of new seasonal lines for only a few customers at a time, rather than large events, can be effective. Celebrities endorsing such brands should reflect their sophistication, and overexposure to them could be harmful. In China, the watchmaker Patek Philippe’s strategy would appeal to these consumers: for example, the company’s two flagship stores in mainland China are at locations (one of them the historic former US embassy) that exude a sense of heritage and tradition.

The rapid growth in the number of China’s wealthy consumers makes them targets for any luxury and premium brand. But that’s no secret, and many companies are setting their sights on this attractive group. To maximize the value of their marketing efforts and to create a lasting relationship with customers, they must understand how these consumers differ from wealthy households in other markets, from other Chinese consumers, and from one another. Only then can companies win the trust and loyalty of China’s wealthy and play a role in shaping their evolving tastes and buying behavior.