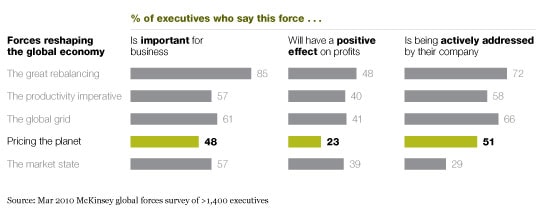

The tension between rapidly rising resource consumption and environmental sustainability is sure to prove to be one of the next decade’s critical pressure points. Natural resources and commodities account for roughly 10 percent of global GDP and underpin every single sector in the economy. No one will sit on the sidelines in this debate.

The interplay of three powerful forces will determine what resources we use, how we use them, and what we pay for them:

- Growing demand. Even the most conservative projections for global economic growth over the next decade suggest that demand for oil, coal, iron ore, and other natural resources will rise by at least a third. About 90 percent of that increase will come from growth in emerging markets.

- Constrained supply. As easy-to-tap and high-quality reserves are depleted, supply will come from harder-to-access, more costly, and more politically unstable environments.

- Increased regulatory and social scrutiny. Around the world, political leaders, regulators, scientific experts, and consumers are gravitating to a new consensus that is based on fostering environmental sustainability. Climate change may be the most highly charged and visible battleground, but other issues loom: water scarcity, pollution, food safety, and the depletion of global fishing stocks, among other things. For businesses, this new sensibility will present itself in two ways: stricter environmental regulations and increasing demands from consumers—and employees—that companies demonstrate greater environmental responsibility.

To understand how the world is likely to change as these forces collide, start by distinguishing between resource stocks, which are not likely to change much over the next decade, and resource flows, which will change enormously.

The fossil fuel consumption infrastructure is so large that, despite recent clean-energy investments, the ratio of fossil fuel to renewable and nuclear power use in 2020 will still be 80 percent, as it is today.

Despite huge investments in clean energy, in 2020 the ratio of fossil fuel consumption to renewable and nuclear power will remain largely as it is today—roughly 80 percent. No realistic scenario will move the needle: the embedded resource infrastructure is so large that any transition away from fossil fuels will take decades.

But the view changes dramatically when you look beneath the supply stock to the flows of new investment. Suddenly, clean tech emerges as one of the next decade’s biggest growth industries. Upward of $2 trillion will probably be invested in building clean-energy capacity globally over the next ten years. In the United States, 90 percent of this expanded capacity will be in renewable or nuclear energy—66 percent in the European Union and China. Before 2020, this investment will probably create a clean-tech industry generating well over $1 trillion a year in sales.

No country better epitomizes this contradictory dynamic than China, which in recent years has emerged as both the world’s biggest carbon emitter and—if future actions speak louder than words—arguably its leading clean-energy champion. Buoyed by strong economic tailwinds, Chinese electricity demand is growing by 15 percent a year, creating the world’s largest market for power generation equipment. To date, China has kept pace by adding a slew of coal-burning power plants that emit a lot of carbon. But motivated both by the huge costs of environmental degradation and by fears of overdependence on Middle Eastern oil, Beijing has moved decisively to support the development of clean-energy technologies. China may be the world’s number-one polluter, but it is also the world’s largest consumer—and manufacturer—of wind turbines and solar panels. And it will soon take a commanding lead in the use of clean-coal and nuclear technology.

In fact, China is building the clean-energy businesses of the 21st century—not just locally but globally too. Suntech Power, China’s largest manufacturer of solar panels, now commands 12 percent of the US solar market. The company, which will soon open its first factory in the United States, hopes to capture 20 percent of the US solar-panel market over the next two years.

As a result of this enormous shift in flows, some business models will be obliterated, others will thrive, and yet others, especially outside the resource sector, may barely change. For CEOs, understanding their true exposure to energy and environmental risk will require more sophistication than ever and will emerge for many as a—if not the—decisive factor determining the long-term viability of their companies.

Commodity prices will rise higher—and fall harder

For most resource commodities, the question is not whether supply will be sufficient but rather what will happen to the price. And that depends in part on what it takes to gain access to resources.

With 12 percent of the US solar market, China’s Suntech Power leads the country in solar-panel manufacturing and in building the 21st century’s clean-energy businesses, both at home and abroad.

Just four countries—Iran, Iraq, Saudi Arabia, and Venezuela—hold some 50 percent of known oil and gas reserves. Nationally owned oil companies now control over 85 percent of them. Many of the key providers are highly exposed to broader geopolitical instability, which makes security of supply a major risk. Meanwhile, new supply is proving harder to find. Most new sources, such as deep-sea reserves or oil sands, require high-priced, environmentally controversial approaches to extraction.

These factors all suggest that oil prices will be both higher and more volatile. Adding to the complexity is the fickle nature of global commodities markets. The number of “virtual” barrels of oil, in the form of futures and derivatives, traded on global exchanges each day exceeds the number of real barrels by an estimated ratio of 30 to 1. This “market effect,” enabled by the global grid, amplifies any market tremor—a key reason oil prices collapsed to just 20 percent of pre-crisis levels in the immediate wake of the financial crisis, falling from above $150 to roughly $30 a barrel. Few other industries could experience such pricing changes in just six months.

Yet oil isn’t the only commodity susceptible to wild price swings. For example, more than half of the world’s copper production is concentrated in a handful of countries with limited infrastructure and high extraction costs. Producers know that over the long term, demand for copper can only grow. At the same time, they’re wary of investing in infrastructure ahead of the demand cycle—a strategy that practically guarantees future pricing volatility.

In uncertain times, the need to plan for widely different outcomes is the one clear certainty

Regulation will prove another wild card. Virtually every major economy in the world is contemplating stricter rules, but there’s little consensus over which regulatory schemes will be adopted, much less how they will be enforced. Some could dramatically transform business models. How, and if, carbon is priced, for example, could fundamentally alter many industries. The same is true with water.

Large regulatory changes are sure to disrupt entire value chains. Agriculture, for example, is one of the world’s leading carbon emitters. If it becomes regulated under a carbon regime, that will affect not just farmers but also their suppliers—for example, equipment manufacturers, seed producers, and fertilizer providers—as farmers scramble to adopt emission-reducing agronomic techniques, such as no-till planting.

Consumer behavior may prove the great unknown. Although consumers are becoming much more environmentally aware, to date they have not shown much proclivity either to reduce their resource consumption or to pay for environmentally friendly products—and certainly not if such products cost more. (There are some notable exceptions, such as the Toyota Prius, which captured more than 2 percent of the US market, despite being 20 percent more expensive than a similar vehicle powered only by gasoline.) That resistance could change dramatically as we have seen before: recall the backlash against chemical companies in the 1960s, following the publication of Rachel Carson’s Silent Spring.

The implication: companies can no longer rely on business-as-usual scenarios when it comes to resources; they must factor in higher base-level prices and increased volatility. They also need to weigh any number of factors that are not yet—but may become—priced in the future, such as carbon and water. And they need to understand how customers might respond. Since these are huge uncertainties, companies will have to consider their options and outcomes under multiple scenarios.

Business models that drive resource productivity will be just as important as those that drive labor productivity

Despite the hype over clean energy, the biggest impact from rising pressure to price the planet may well come from something much more mundane: conservation. Boosting resource productivity—like labor productivity—will become an increasingly important way for businesses to reduce both their costs and their pricing exposure. Many of these gains require low capital investments and are comparatively easy to adopt.

Advances in fields such as environmental product design and “green software” (which helps optimize resource usage) will become important ways for companies to reduce resource consumption. UPS, for example, has saved 2 percent on fuel costs by using software that helps plan delivery routes with fewer left turns (which use more fuel than right turns). Similarly, Apple has created approaches to reduce waste in its products: since it launched the iMac, it has reduced raw-material content by 50 percent and energy consumption by 40 percent. Boeing designed its new Dreamliner with both the environment and costs in mind: by using lightweight composite materials, the company improved fuel efficiency by more than 20 percent, reducing both a customer’s lifetime ownership costs and potential future environmental exposures.

Regulatory decisions will foster clean-energy innovation as well. Long-term Spanish subsidies of wind power are major reasons for the rise of two Spanish companies, Iberdrola Renewables and Gamesa, as global leaders in wind energy.

Customers, too, are pushing companies to become more environmentally friendly—and helping to spawn some great new businesses. Clorox, for example, captured 40 percent of the US natural-cleaning-products market within the first quarter of launching its GreenWorks line, increasing the size of the overall category substantially. Moreover, it did so by offering a suite of products that were up to 25 percent cheaper than other natural products. That made customers happy, and GreenWorks pleased shareholders as well by generating margins 20 to 25 percent higher than the company’s average.

Of course, not every green investment is a good investment, so companies need to assess the puts and takes on their options carefully. The future of some green businesses, such as carbon trading, depends hugely on still-murky regulatory environments. Other opportunities, particularly in clean energy, will take years to scale. Still others, such as “smart” building technologies, may have an immediate payoff today, both for customers adopting them and businesses selling them.

Plan for regulatory change—but don’t count on global consensus

Governments everywhere hear the clamor for sustainability, but most also know they will retain power only if they keep delivering economic growth. Couple that imperative with the high coordination costs and fundamental resource usage inequities that persist across countries—China, for example, emits less than a fifth of the carbon dioxide per capita that the United States does—and it’s hard not to conclude that while broad agreements may be possible, they will more likely prove elusive, as first Kyoto and now Copenhagen have demonstrated.

Future natural disasters seem inevitable, and so does the rise of “adaptation” businesses and offerings—for instance, new insurance and building products that respond to environmental challenges.

Nonetheless, we should fully expect a flurry of environmental regulations at the regional and local level. Local environmental problems, especially those (such as water safety) with immediate health consequences, will be solved more easily than global ones. Companies should identify where regulation is most likely to occur and get ahead of potential challenges—not always by taking action but, at least as a first step, by having a plan for what to do if laws change.

Without coordination, this likely future patchwork of varied global regulatory standards may create unexpected opportunities. The model example is hybrid-electric-motor technology. First commercialized in Japan in response to stricter emission guidelines there, it later proved a commercial hit with US consumers, even though US regulations did not require the same standards. Expect more such arbitrage plays in the years ahead.

Finally—and sadly for regions especially exposed to climate change and other forms of environmental degradation—we should prepare for the strong likelihood that an effective global regulatory regime will not appear in time. Look for the emergence of “adaptation” businesses, which develop in response to environmental disasters or challenges. New kinds of insurance products, building products, commercial fisheries, and other businesses designed to respond to tomorrow’s environmental realities may well grow and thrive.

The impact of global forces on business

Related Articles

Global forces: An introduction

The great rebalancing