Merger-and-acquisition activity may have slowed during the third quarter of the year, but it’s unlikely to stay slow, the results of a new McKinsey survey suggest.1 In this survey, we asked finance and other senior executives to weigh in on how M&A will change in the coming months and years: the expected size of deals, the capabilities in place, and the amount of attention devoted to differences in organizational cultures.

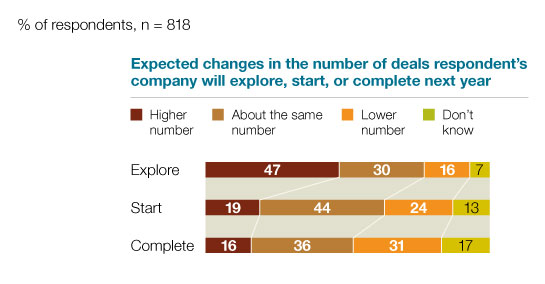

The results show that in spite of the difficult economy, most executives still think M&A is an important strategy for growth. In fact, nearly half of the respondents expect their companies to explore more deals in the next 12 months than in the past 12, and small majorities expect them to start or complete at least as many, if not more.2 In addition, nearly half of the respondents report that their companies are looking outside the core business for new ways to grow. There’s no consensus on whether deal size will increase, but executives do indicate that they expect to focus more on deals that bring specific strategic advantages, such as new geographies, products, or intellectual property. The results also indicate that many companies still need to build critical capabilities, including integration planning, responding to cultural issues, and establishing standardized deal teams. That effort may well be complicated by a striking number of areas in which CFOs’ opinions differ from those of other C-level executives on topics as basic as which deals to do and what capabilities a company has.

Defining deals

A majority of respondents agree that M&A remains a necessity for growth. The most common rationale cited for deals is to acquire products, intellectual property, and capabilities. Executives at private companies are likelier than those at public ones to say that their companies have done deals to acquire products or intellectual property, to incubate new businesses or enter new geographies, or to acquire scale.

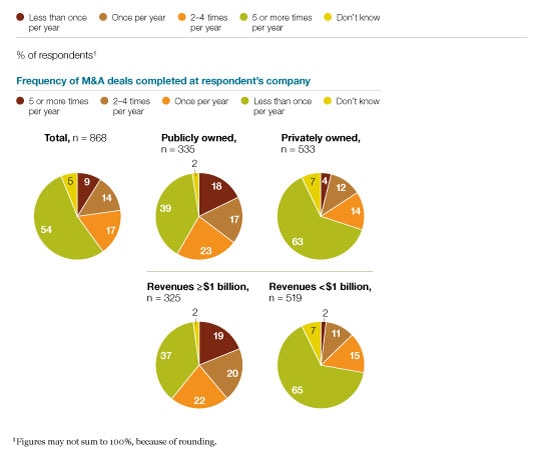

Seventy-seven percent agree that M&A is an important factor driving consolidation in their industries. Respondents at publicly owned companies and at larger ones (with annual revenues of at least $1 billion) say their companies complete more deals than others. Among all respondents, a majority report that their companies complete deals less often than once a year (Exhibit 1).

Given that finding, it’s no surprise that more than half of the respondents report that their companies invested 10 percent or less of either their market capitalization (at publicly owned companies) or their annual revenues (at privately owned companies) in M&A over the past 12 months. Moreover, although nearly half of the respondents expect their companies to explore more deals over the next 12 months than they did over the past 12, few expect that they will start or complete more (Exhibit 2).

More deals made at larger, public companies

Better prospects for exploration

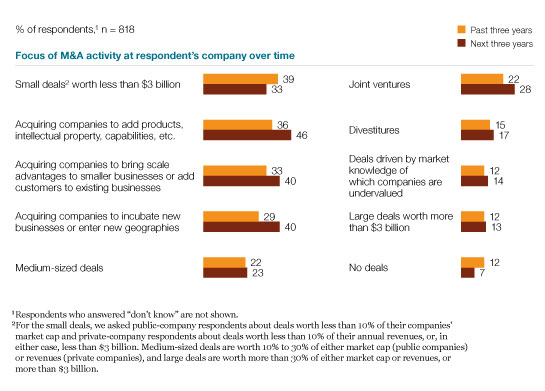

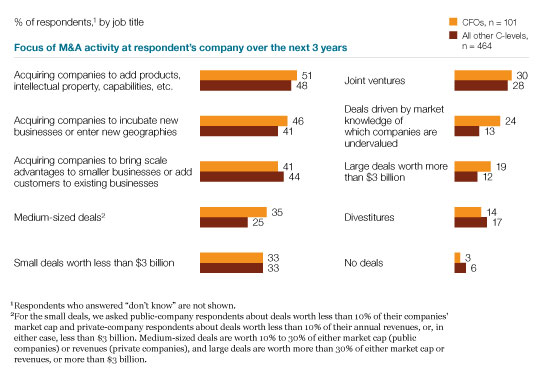

As for the size of deals in the next 12 months, the respondents are divided. Just over a third expect deals to remain about the same size, while a quarter expect the value to decrease— the same share expecting it to increase. Most common over the past three years, respondents say, were deals worth less than 10 percent of their companies’ market cap or annual revenues.3 Smaller shares of respondents expect such small deals to be a focus of their companies’ activity in the next three years. These respondents expect other strategic goals to become more important—especially acquiring companies to add products, intellectual property, and capabilities (Exhibit 3).

Future focus on strategic acquisitions

Putting the pieces together

In our experience, it’s critical for companies to take a systematic and fact-based approach to understanding corporate culture if they hope to retain critical people and capabilities after a transaction. Responses to this survey show that many don’t. Nearly a third of the respondents report that their companies put off integration planning until after negotiations have begun. And while nearly three-quarters of the respondents say the companies they work for understand their own cultural strengths and weaknesses, far fewer conduct internal organizational due diligence to confirm that understanding: less than half say their companies do so to diagnose strengths and weaknesses in the context of specific deals, and just over a third say they do so when they’re not doing a deal. Furthermore, 29 percent say their companies are not willing to make changes or launch targeted interventions to address cultural gaps.

One reason so many companies fall behind at managing integration and cultural differences may be a lack of resources and formalization. Only a slim majority of respondents believe their companies have the right number of people and organizational resources to meet M&A aspirations, and only 49 percent report that their companies have standardized deal teams (Exhibit 4). Moreover, only a bit more than a third of the respondents report that their companies have standardized integration teams, and just over half report that their companies’ M&A capabilities rest in specific individuals rather than the institutions.

Lack of resources and standardization

This lack of structure may also underlie other merger-management weaknesses: around a third of the respondents report that their companies have failed to capture synergies because of factors such as slow decision making (chosen by 35 percent), unclear decision-making criteria (31 percent), and implementation plans lacking sufficient detail (31 percent). More active companies seem to lean toward standardization: the companies where respondents are significantly more likely to report that they have standardized deal teams are those where respondents also say that they do more deals by value, do deals more frequently, or generate higher revenues. In addition, standardized deal teams are more common at companies whose respondents also expect them to explore, start, or complete a high number of deals in the next 12 months than at companies planning fewer deals. These teams also are more likely to exist at companies where respondents agree that M&A is important for consolidation in their industries.

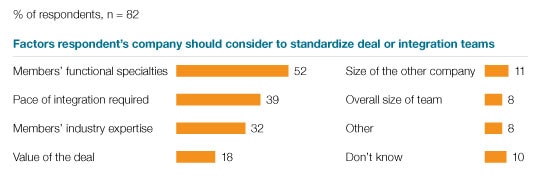

Looking at integration, executives of companies with standardized teams in place are significantly likelier to report that they have the right number and quality of people in place to meet their aspirations—more than 80 percent say so. This finding is consistent with our experience: we’ve seen that standardized deal teams tend to be both more experienced and more capable of realizing value that cuts across functions. Respondents who say that their companies don’t have standardized deal or integration teams most often cite functional skills as the factor to consider in standardizing team setups (Exhibit 5).

Considering skills in teams

Different functions, different perceptions

CFOs’ views differ from those of other C-level executives on a number of topics we asked about in this survey. CFOs are much likelier to agree that M&A is important for their companies’ growth, that it’s important in consolidating their industries, and that their companies have a clear understanding of cultural strengths and weaknesses.4 CFOs are markedly less likely to agree that their companies are looking outside the core business for new ways to grow (40 percent of CFOs say that, compared with 51 percent of other C-level executives), that they have the right number of people and organizational resources to realize M&A aspirations (42 percent to 52 percent), or that they have the right quality of people and organizational resources (52 percent to 57 percent).

Furthermore, CFOs expect their companies to do deals different from those cited by other senior executives: for example, they are more likely to expect their companies to focus on medium-sized deals and deals driven by market knowledge of which companies are undervalued (Exhibit 6). These differences may arise because CFOs are more connected to the financial rationale of any given deal than to the business rationale or because CFOs are more frequently brought in on larger deals.

CFOs diverge on future deals

Looking ahead

The results and our experience suggest that many companies have an opportunity to boost their chances of making successful deals if they formalize their approaches to M&A planning and integration and ensure that know-how is broadly disseminated. Besides standardizing teams and dedicating expertise, the helpful actions we’ve seen include building M&A playbooks and tool kits, as well as conducting a postmortem after each deal.

It is critical for companies to retain talent and manage cultural differences. The results suggest that most companies would benefit from examining whether they have established the culture and structures to make the most of the different skills, values, and insights available in acquired organizations.

Given the increasingly common role of many CFOs as operators and strategists, it’s important to acknowledge and explore any differences between their expectations and those of other C-level executives. Clear senior guidance is crucial to successful transactions, so executive teams should spend more time building a shared understanding about the role of M&A in executing strategies and the types of M&A that organizations should pursue.

Related Articles