The classic approach to corporate strategy starts with a presumption: that with sufficient analytical rigor and an adequate assessment of the probabilities, strategists can pave a predictable path to the future from the matter of the past. In this world, they make reasonable assumptions about the evolution of product markets, capital markets, technology, and government regulation and, in effect, "assume away" most risk. Chief executive officers articulate strategy every few years, often in the context of a change in top management.

Such traditional strategy formulation often pays lip service to the perspectives of the capital markets, to changing industry structures, and to the forces at work in the environment. But in reality, a "visionary" corporate strategy is often an internally driven reflection of what the company wants the world to look like.

But suppose we no longer believe that the future is foreseeable. What if defining and achieving an enduring competitive advantage is really just a conceit that must be abandoned? What if the outstanding fact of business, as John Maynard Keynes once described it, is the "extreme precariousness of the basis of knowledge"? What if it is no longer possible to block out the "noise" of the world's messy reality in order to rationalize a plan to achieve predetermined outcomes?

In fact, this is the confusing, complex, and uncertain environment that corporate leaders now face. Globalization and technology are sweeping away the market and industry structures that have historically defined the nature of competition. Although the pace of change continues to accelerate, the fundamental transformations under way in the global economy have only just started.1 The variables that can profoundly influence success and failure are too numerous to count. That makes it impossible to predict, with any confidence, which markets a company will be serving or how its industry will be structured—even a few years hence.

The result is an economic environment that is rich in opportunity but also marked by a substantial increase in awareness of risk and aversion to it— a phenomenon reflected in the rise of risk premiums throughout the world even while the risk-free cost of capital remains low.

A new approach

Strategy today has to align itself to the fluid nature of this external environment. It must be flexible enough to change constantly and to adapt to outside and internal conditions even as the aspiration to deliver favorable outcomes for shareholders remains constant.

An analogy may help. Consider the management problem of moving supplies and ships across the Pacific Ocean during World War II. The starting point for the strategist was to recognize that controlling the environment—the weather in the Pacific—was beyond anyone's power but that risks could be minimized and schedules roughly set through the study of weather patterns and the use of navigational aids. But the real challenge was to consider factors beyond natural forces—factors such as enemy submarines, other enemy ships, and air attacks, analogous to corporate competitors with unknown capabilities and plans.

The strategist's answer was to deploy whole convoys with a mix of aircraft carriers, battleships, destroyers, escort ships, troop ships, and supply ships. Convoys improved the ability of each ship to cross the ocean and, crucially, helped to ensure, through "portfolio effects," that sufficient supplies made it across the ocean even when some ships didn't. The strategist couldn't know where battles might occur or which ships would be lost to enemy action. Yet the probability of success for individual vessels and the mission as a whole could be increased.

Likewise, a CEO can think about corporate strategy not as a "portfolio of businesses" but as a "portfolio of initiatives" aimed at achieving favorable outcomes for the entire enterprise. Usually, these initiatives will be organized around themes—"convoys" if you please—focused on achieving particular aspirations, such as increasing the global reach of the enterprise, entering a new but related industry, or achieving the industry's lowest marginal cost of production. Portfolio effects increase the likelihood that some of these aspirations will be achieved even if many others fail.

Like a more traditional strategy, such an effort is best led by the corporate center and an activist CEO, making use of his or her command over talent and resources. Beyond that, however, most executives will find this approach more deductive, adaptive, and fluid than any they have used before.

Familiarity breeds opportunity

An approach that enables a corporation to mobilize convoys of initiatives now offers extraordinary payoffs. In the post-September 11 business environment, risk premiums have risen for all manner of investments. Consider the rise of risk premiums in the bond markets: in early 2002, for example, US Treasury bonds commanded nothing less than an 8 to 9 percent premium over B-rated corporate debt, compared with a spread of only 4 percent just ten years ago.

Risk premiums rise not only because the absolute level of risk increases but also because lenders require higher rates of return when they are unsure about how companies will perform—that is, when they lack deep famili-arity with the specific risks individual companies face. An investor who can acquire distinctive knowledge about particular B-rated credits and discern where the risk premiums are "too high" can create a bond portfolio with superior returns relative to the risks taken. Strategy thus becomes increasingly about gaining competitive advantage through deep familiarity (in other words, distinctive knowledge), which can transform the rise in risk premiums into increased rewards.

Consider another analogy. Of two runners, one is faster than the other and can be expected to win on a level track no matter how many times the race is run. But what if the race were held at night on a path strewn with rocks and fallen trees? Suppose that the slower runner practiced both in daylight and at night, while the faster one didn't bother to see the course in advance. The runner with the superior knowledge—the greater familiarity—would probably win even if the other were intrinsically faster. If the prize money were to rise, the value of familiarity would rise as well.

In today's increasingly global economic environment, confusion about risk is like the obstacles in this analogy. Familiarity makes them less dangerous. As the global economy evolves, and as geographic markets and industry structures aggregate, par-ticipants will enjoy a variety of advantages from familiarity and a variety of disadvantages from unfamiliarity. The strategic idea is constantly to adapt the corporation to this fluid environment and to take risks primarily where it enjoys the former, while shedding the latter.

Statisticians call this approach a search for "asymmetric" risk. Oddsmakers might call it "loading the dice," and it is the opportunity to capture this effect that makes a portfolio-of-initiatives approach so appealing today. If companies scanning the range of new opportunities choose to compete only where they have significant advantages of familiarity, and if they can build a portfolio of such initiatives, they make it highly probable that they can prosper even amid a high level of complexity and uncertainty.

A portfolio in action

Consider the hypothetical case of a financial company. Bank Multistate, a multiregional institution with $250 billion in assets and $2 billion in profits, was formed from a series of regional bank mergers. Its strengths lie in lending to small and midsize businesses, branch-based retail banking, credit cards, and mortgage banking. It also has special strengths in commercial finance and leasing.

Bank Multistate enjoys a number of familiarity advantages in many of its core businesses and geographic locations. It is particularly familiar with the use of technology to improve the productivity and underwriting results of lending to small businesses. The bank wants to explore whether it could use this skill to become an "outsourcing" intermediary for other banks. To load the dice in this initiative, Bank Multistate might begin by making a small bet ($1 million to $2 million) to assess the opportunity and design a value proposition. Its objective would be, first, to acquire distinctive knowledge by exploring market acceptance of its proposed offering and by "reverse-engineering" possible competing offerings. It would also work to acquire skills such as hiring experienced talent. During this exploratory phase, a full-time team of one senior manager and three or four junior managers and analysts would probably be deployed for four to six months.

Diagnosis and design can take a company only so far, however. Much of the needed familiarity can come only through experimentation, which in this case might include testing the new value proposition. At this point, Bank Multistate might need to make a medium-bet investment of $20 million to $30 million to undertake a pilot with two or three customers.

If the customer pilots proved successful, Bank Multistate might then be willing to make a large bet of $200 million or more so that the company could leapfrog potential competition. In any case, the decision on whether or not to scale up the business would be made "just in time," when further information had been gained from the pilots. By staging the investments, Bank Multistate would be using the passage of time to acquire deep familiarity and the option to expand, while still limiting its downside risk until the value proposition became clearer.

The hallmark of this approach is a willingness to change direction contin-ually as more and more distinctive knowledge is acquired. The approach implies an expectation that major midcourse corrections will be required, not that everything will go according to plan. It calls for a willingness to shut down initiatives if it becomes clear that they are headed nowhere.

Certain companies already use this approach in at least some of their strategic decision-making processes. The pharmaceutical industry has long used such disciplined processes to develop new drugs and medical devices, and so have venture capital firms, with their portfolios of companies. But most businesses are much less disciplined: far too often, large-scale decisions to build new businesses, to acquire or divest others, and even to adapt core businesses to changing conditions are made under extreme time pressure. In turn, these big, spur-of-the-moment decisions often come about because the company squandered its available lead time.

In particular, most companies put too little energy into adapting core businesses to changing markets. Indeed, they often unintentionally harvest their core businesses by pushing for short-term performance while neglecting the investments needed to stay ahead of the game. Often, companies move only when competitors start investing aggressively. When these companies do act, they usually make insufficient small-bet investments in diagnosis and design and skip the medium-bet prototyping and piloting steps entirely because they are trying to play catch-up. As a result, these initiatives are often exposed to entirely avoidable risks in execution, or, even worse, sometimes businesses panic and make bet-the-company investments based upon leaps of faith.

In a portfolio-of-initiatives approach, every major strategic action is subject to a disciplined process. Bank Multistate might, for example, have 10 to 20 such initiatives, at various stages of exploration, in order to build new businesses, to adapt its core businesses, and to acquire or divest businesses. The bank might have pursued some of these initiatives in the ordinary course of events. What makes a portfolio-of-initiatives approach different is the quantity of initiatives explored, the rigor of the analysis behind them, the discipline of the process, the willingness to make midcourse corrections, the staging of investments, the high degree of hands-on involvement by executives, the open discussion of issues, and the care taken before deciding whether to forge ahead.

Rigorous monitoring is crucial. The group for reviewing initiatives could consist of a strategy oversight team of the company's 20 or so top managers, chaired by the CEO, which would review initiatives perhaps monthly. Each initiative might well be reviewed several times before the final large-scale decision is made.

Increasing the visibility and transparency of these processes helps ensure that the best decisions are made and raises the stakes so that managers don't approach the group's work in a halfhearted way. The intent, of course, is to improve performance. In Bank Multistate's case, a favorable outcome for the shareholders might be financing five or six big-bet initiatives annually. In all, these might provide an extra 5 percent a year of growth in earnings and an extra 3 percent increase in the bank's return on equity—without involving big risks.

Three distinct elements are central to a portfolio-of-initiatives approach. First, it entails a disciplined search, based on familiarity, to discover and create initiatives that provide disproportionately high rewards for the risks taken. Second, it involves a dynamic, continuous effort to manage the portfolio of initiatives resulting from this search process and the use of time-management and portfolio theory to overcome unavoidable risks due to complexity and uncertainty. Finally, it calls for a flexible and evolutionary approach that lets "natural selection" rather than vision determine where, how, and when to compete. It may be useful to examine each of these elements in greater detail.

A disciplined search

CEOs might find it difficult to believe that there can be an abundance of "no-regrets" and "low-regrets" opportunities in these uncertain times. Yet the same global forces that create confusion, complexity, and uncertainty also create opportunities for companies to innovate in their core businesses. The world's markets and industry structures are in flux because the global forces at work are lowering the barriers to interaction.2 As interaction costs fall around the world, new economies of specialization, scale, and scope are being created—economies that can provide innovative companies with an abundance of opportunities to earn high rewards for the risks taken. Some companies, for example, are discovering that they can save up to a third of their labor costs in overhead or customer service functions by moving them to, say, Scotland or India.

Most large incumbents have dozens of high-potential opportunities to use their familiarity advantages to adapt their core businesses or to build closely related ones that could capture the new economies of scale, scope, or specialization. Many of these seemingly mundane opportunities will prove upon close examination to have higher returns, relative to the risks taken, than some other activities on which the company may already be investing its focus, talent, and discretionary spending. A daylong brainstorming session can usually generate dozens of ideas about potential opportunities.

The challenge is to convert these raw ideas into real investment opportunities. A company must organize a disciplined search to identify, enhance, and nurture its best ideas—and deploy some of its most talented people to pursue them—if it wants to create real opportunities to earn high returns relative to the risks taken. One of the hallmarks of a portfolio-of-initiatives approach is the overinvestment of scarce resources, such as discretionary spending, talent, and focus, on acquiring advantages of familiarity. No less important, senior management must "just say no" to making big bets in situations in which it lacks familiarity or is exposed to uncertain outcomes, even when competitors are making big strategic moves. As a rule of thumb, a company is familiar with opportunities when it doesn't have to take any large leaps of faith to understand where it expects to make returns from its investments.

Managing a portfolio of initiatives

Corporate-level involvement is essential because hard decisions must be made about allocating scarce resources to nurture the initiatives. Only the company's top-management team can balance the risks, rewards, and timing of each of the initiatives and make decisions about which to start, scale up, or terminate.

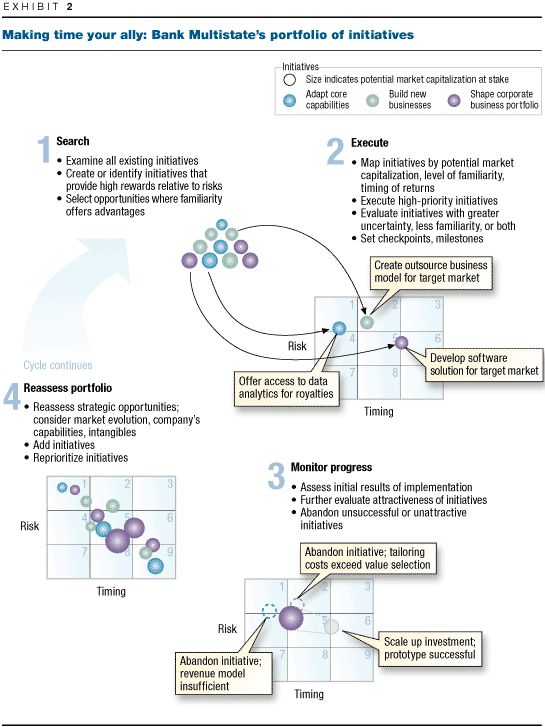

The challenge for a chief executive and the top-management team is to create enough initiatives to be reasonably sure that the company will be able to outperform the market's expectations. While it is essential always to have opportunities with large current returns, numerous small-bet initiatives can hold out the promise of large potential future returns once familiarity has been achieved. Much of the challenge of undertaking a portfolio-of-initiatives approach to strategy is the need to keep many balls in the air at the same time. To make it easier to do so, we have found it helpful to use a simple matrix to array on a single page all of the initiatives being undertaken (Exhibit 1). This matrix allows the strategist to see, at a glance, the economics at stake, the risk level of the investments, and the time horizon until each initiative matures.

Executives employing a portfolio-of-initiatives approach should make the passage of time an ally. Checkpoint reviews, milestones, and staged investments enable managers to make maximum progress while minimizing risk. Pilot programs build familiarity before investments are scaled up. Risks arising from complexity and uncertainty fade as time passes, because the range of outcomes is reduced (Exhibit 2). Competitive advantage comes in the form of the progress a company makes while its competitors, paralyzed by confusion, complexity, and uncertainty, sit on the sidelines. The key is to be ready to act as soon as it becomes possible to estimate, in a reasonable way, the risks and rewards of an investment. The advantage lies not with the first mover but with the first mover that can scale up activities once the way forward has become clear and it is possible to see returns from larger bets.

A flexible and evolutionary approach

A successful portfolio-of-initiatives strategy involves creating enough initiatives offering high returns relative to the risks taken to enable a company to meet its aspirations and outperform the expectations of the capital markets. The process requires the CEO and the management team to keep an open mind about where the company might be headed. Inherent in this approach is the understanding that future decisions and future outcomes are likely to vary enormously from initial hypotheses. The whole process resembles art more than science. Most of the critical decisions involve subjective judgments that, unlike those generated by more deterministic strategies, will be informed by not just the highest-quality staff work but also the knowledge gained as time passes.

There is, of course, no substitute for the talent of a top-management team. But the advantage of the portfolio-of-initiatives approach is that it is far better at getting the most out of a company's top talent than are traditional approaches to strategy.

Although the world is increasingly complex, confusing, and uncertain, serendipity doesn't have to be more important than skill in the crafting and implementing of corporate strategy. Traditional deterministic approaches to strategy aren't likely to be up to the task of helping companies negotiate these dangerous waters, but executives need not put the fate of their businesses entirely in the hands of chance. As the global environment continually changes and risk levels rise, a portfolio-of-initiatives approach holds out the opportunity for corporations to be as flexible and adaptive as the markets themselves.

Related Articles