The CFOs of any company that uses or produces energy were naturally interested in the outcome of the recent Copenhagen round of global climate negotiations, for both the potential new costs and new opportunities. Although the conference did not lead to the legally binding global carbon reduction treaty that a lot of climate watchers had hoped for, many are still watching closely as regional (rather than global) carbon markets continue to evolve. For despite the uncertainty in Copenhagen, current global carbon market arrangements will probably survive. The pricing that these markets set for carbon emission allowances will continue to be increasingly important for businesses—in particular, those facing the cost of buying allowances (so-called carbon credits) or developing projects for which carbon credits are anticipated sources of revenue.

Emission caps and related carbon trading in developed nations are a very effective way to reduce carbon emissions if supported by other forms of regulation, such as energy-efficiency standards. Moreover, developed nations will continue to be bound by domestically defined emission caps and can trade their carbon allocations among each other and through the offset market for developing nations.

However, the role of carbon markets in developing nations (through offset financing) is still unclear and might be relatively limited compared with their role in developed nations. The difference is a result of both the large potential of and requirements for emission reduction in developing countries and the limited demand for offsets from developed nations, given the current proposals on the table. This imbalance may limit the ability of companies in developed markets to benefit from offset credits for investments in developing nations. Indeed, if carbon markets do not take off in developed nations in a major way, companies could be left holding credits for which there is no demand.

The economics of offset markets

Even though a global deal remains elusive, domestic and regional carbon markets will continue to grow—from slightly less than €100 billion in 2008 to around €800 billion in 2020, according to recent McKinsey estimates. The European Union, for example, already has a domestic carbon market—currently the only one of its size, with trading volumes expected to increase as the market matures and liquidity increases. The United States is poised to establish one, with climate change legislation awaiting action this year. And a number of other countries, including Australia, Canada, Japan, and New Zealand, are considering the introduction of domestic carbon markets. At the same time, multiple regional markets exist (within the United States, for example) or are being considered (as in China), mostly voluntary in nature.

Companies in these markets have a choice of reducing their own emissions to stay within their caps, buying credits from other companies, or buying international offsets. Abatement achieved through domestic carbon markets counts toward the economy-wide targets, as do purchased international offset credits. Without a mechanism linking the various domestic carbon markets, prices, driven by local market conditions, will probably vary significantly.

The offset market plays a key role, as it is the de facto international carbon price mechanism, in the absence of direct market linkage. In theory, an originator of offset credits—say, an offset project developer—can sell its credits to a government in an Annex I country1 (which will use these credits to offset its carbon reduction commitments) or to a company in a domestic carbon market. These activities can create price arbitrage between various domestic carbon markets and the international carbon market.

Two factors hamper price equalization among the offset market, domestic carbon markets, and the global market as envisioned by the assigned amount units (AAU) established in the 1997 Kyoto Protocol on climate change.

On the one hand, countries have limited the amount of offsets that can be imported into domestic carbon markets. For instance, the European Union will allow only 1.6 metric gigatons2 (GT) of offset credits to be imported into its market from 2008 to 2020, or on average 0.1–0.2 GT per annum. As this quota will probably be exhausted by 2015, prices on the European carbon market might start to deviate from offset market prices.

On the other hand, the demand for offsets from Annex I countries is less certain, as the global market is oversupplied with “hot air,”3 which limits the need to buy offset credits. Therefore, national demand for offset credits is typically seen as “soft.”

Offset market supply also plays a key role in offset market prices. Initially, offsets were based on relatively cheap sources; for instance, many reductions in levels of greenhouse gases other than carbon dioxide require little upfront investment. As the market matures, more expensive sources of abatement, often requiring an upfront investment, will be pursued. Supply will also be determined by the offset market’s future structure. Currently, carbon offsets are project based, which requires independent verification of projects—a slow and bureaucratic process. There are also concerns about the so-called additionality of project-based offsets.4

Multiple proposals have been put on the table to scale up offset markets. Key options include a reformed project-based mechanism, a programmatic mechanism that would award policies with credits, a sector no-lose mechanism that would reward abatements but not punish their absence, outright sector caps, or any combination of the above. The eventual supply of credits and their relative cost will be determined by the choice of mechanism, as well as the type of offset credits allowed (for example, whether they include carbon capture and storage, nuclear power, or efforts to cut emissions by reducing deforestation and the degradation of forests).

McKinsey has developed a carbon market model based on the firm’s most recent greenhouse-gas-abatement cost curve.5 This tool models all domestic and international carbon markets over time and estimates emission reductions and long-term fundamental carbon price levels by markets, as well as the flows among them. The model is not a price-forecasting tool but does help users understand relative price differences between markets and the fundamental factors that explain those differences. The “hard” demand for offsets is expected to be around 1.4 GT by 2020—adding up demand from domestic carbon markets, including the European carbon market and the expected US one. Additional soft demand from Annex I countries, arising from their reduction commitments, could add a further 0.5 GT of demand but depends critically on the resolution of the hot-air overhang from the 2008–12 Kyoto period and the absence of hot air after 2012.

The model calculates that 2020 carbon prices in the EU emission-trading system (around €29 a ton) will be well above the price in the offset market (around €13 a ton, which reflects the exhaustion of the system’s offset quota). The US carbon market price (€16 a ton) is much closer to the offset market price. The difference results from the offset discount factor proposed in the American Clean Energy and Security Act of 2009.6

Abatement: A modest role in developing countries

The Intergovernmental Panel on Climate Change (IPCC) suggests that the global community needs to limit emissions to 44 GT in 2020 in order to limit global warming to two degrees.7 That goal would require global cuts of up to 17 GT of emissions by 2020. A large share of this decline will have to take place in developed nations, but their potential is limited to 5 GT by 2020. Faster-growing developing nations have more room to make low-carbon choices in energy efficiency and power (6 GT by 2020), as well as most of the emission reduction potential of preserved forests (roughly another 6 GT by 2020).

McKinsey’s carbon market model offers a view on the likely outcomes of the global regulatory debate, and in particular the role played by carbon markets. To do so, the model assesses the effectiveness of existing and proposed climate change regulations, including those outside the emissions directly capped by carbon markets. Emission reductions of all kinds influence carbon market outcomes. As an example, energy efficiency in European buildings (not covered by the EU Emission Trading System) will reduce demand for power and thereby the power sector’s emissions (which are covered). In a similar fashion, climate change regulation in developing nations can influence the availability of offset supply, particularly in sectorwide offset programs.

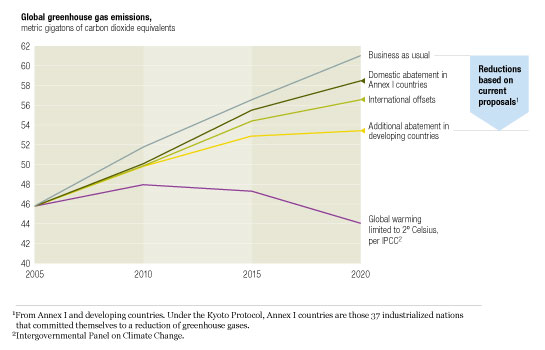

A detailed assessment of all proposals from Annex I and non–Annex I countries currently on the table8 shows that the world will be able to realize only about half of the emission reduction potential required to limit global warming to two degrees (exhibit). Of this emission potential, three GT of reductions will be achieved as domestic abatements in Annex I countries, up to two GT will be international offsets (which count toward the domestic abatement of Annex I countries), and a further three GT will be achieved by autonomous action from developing nations, potentially with financial support from Annex II nations.9

Only halfway

Actions currently envisioned by developing countries include a 70 percent reduction of deforestation in the Amazon rainforest by 2017 (which Brazil has proposed) and the increase of renewable power in China to 15 percent of its energy mix in 2020. In reality, most developing nations are unwilling to make stringent commitments before that year, while some have proposed quantified caps thereafter. South Africa, for instance, proposes to let its emissions peak in 2025 before reducing them after 2035.

Offset demand of up to 2 GT represents significant growth compared with 2008, when 140 megatons of offset credits were issued. Yet 2 GT is a relatively modest amount in light of the up to 17 GT of abatement required to limit global warming to two degrees.

We need to be critical of this assessment, however, as the scenario modeled is only one possible outcome of ongoing discussions. In coming years, countries could markedly improve their proposals for domestic emission caps. The European Union has offered to reduce emissions to 30 percent below 1990 levels if other countries make similar commitments. Japan has already announced a target of reducing emissions 25 percent below 1990 levels by 2020. Although that goal is conditioned on the willingness of other countries to take similarly bold action, it is much more ambitious than the country’s previous goal.

Furthermore, developed nations proposed substantial financial support for developing ones in the nonbinding political Copenhagen Accord: $30 billion in the period from 2010 to 2012 and up to $100 billion a year by 2020. This money might make developing nations more willing to reduce emissions and could therefore raise global performance. However, it might not be possible to achieve the recommended environmental outcome even given a more ambitious scenario with stricter national targets.

As a result of this uncertainty, companies are likely to move away from projects—such as the capture of gases other than carbon dioxide and the reduction of emissions from cooking stoves,10 which are responsible for up to 18 percent of global warming—that rely completely on offsets as their income stream. Instead, they will look for projects that also have other income streams, such as power market revenues and government subsidies, even if these projects require significantly more investment.11