One of the puzzles of the sluggish global economy today is why companies aren’t investing more. They certainly seem to have good reasons to: corporate coffers are full, interest rates are low, and a slack economy inevitably offers bargains. Yet many companies seem to be holding back.

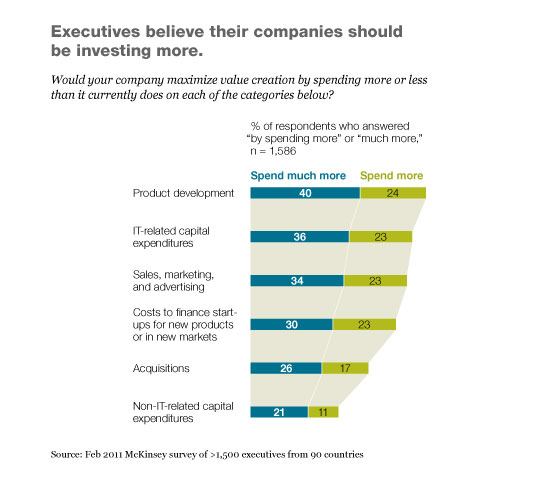

A number of factors are doubtless involved, ranging from market volatility to fears of a double-dip recession to uncertainty about economic policy. One factor that might go unnoticed, however, is the surprisingly strong role of decision biases in the investment decision-making process—a role that revealed itself in a recent McKinsey Global Survey. Most executives, the survey found, believe that their companies are too stingy, especially for investments expensed immediately through the income statement and not capitalized over the longer term. Indeed, about two-thirds of the respondents said that their companies underinvest in product development, and more than half that they underinvest in sales and marketing and in financing start-ups for new products or new markets (Exhibit 1). Bypassed opportunities aren’t just a missed opportunity for individual companies: the investment dearth hurts whole economies and job creation efforts as well.

Such biases, left unchecked, amplify this conservatism, the survey suggests. Executives who believe that their companies are underinvesting are also much more likely to have observed a number of common decision biases in those companies’ investment decision making. These executives also display a remarkable degree of loss aversion—they weight potential losses significantly more than equivalent gains. The clear implication is that even amid market volatility and uncertainty, managers are right now probably foregoing worthy opportunities, many of which are in-house.

The survey respondents1 held a wide range of positions in both public and private companies. All had exposure to investment decision making in their organizations. Nearly two-thirds of them reported that their companies generated annual revenues above $1 billion, and the findings are consistent across industries, geographies, and corporate roles.

More bias means less investment

The survey results were also consistent with earlier findings that biases are common within the investment decision-making process.2 More than four-fifths of respondents reported that their organizations suffer from at least one well-known bias. More than two-fifths reported observing three or more.

Generally, the most common biases that affect decisions could be traced to the past experiences of those who make or support a proposal. The confirmation bias, for example, was the most common one—decision makers focus their analyses of opportunities on reasons to support a proposal, not to reject it. Depending on the proposal, this bias can result in decisions to underinvest or not to invest at all just as easily as in decisions to overinvest. Another common bias was a tendency to use inappropriate analogies based on experiences that aren’t applicable to the decision at hand. A third was the “champion” bias—managers defer more than is warranted to the person making or supporting an investment proposal than to merits of the proposal itself.

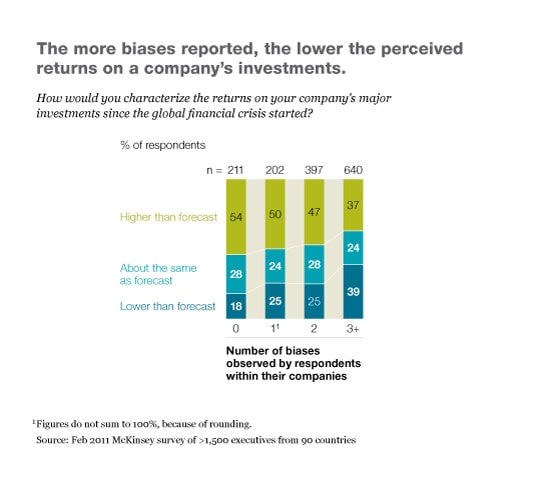

The presence of behavioral bias seems to have a substantial effect on the performance of corporate investments. Respondents who had reported observing the fewest biases were also much more likely to report that their companies’ major investments since the global financial crisis began had performed better than expected. By contrast, those who reported observing the most biases were more likely to report that their companies’ investments had performed worse than expected (Exhibit 2).

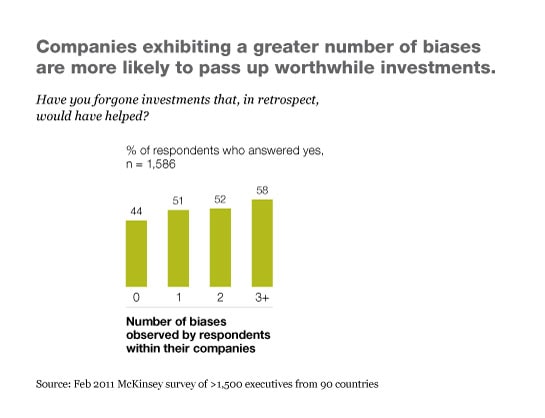

The biases reported by respondents correlate with the performance of investments—and appear to constrain their overall level, as well. Indeed, respondents reporting fewer biases were significantly less likely than those reporting more to state that their companies had forgone beneficial investments (Exhibit 3).

Wary executives

Executives also reported a high degree of loss aversion in the investment decisions they’d observed. They exhibited the same tendency themselves, even when the value they expected from an investment appeared strongly positive. When asked to assess a hypothetical investment scenario with a possible loss of $100 million and a possible gain of $400 million, for example, most respondents were willing to accept a risk of loss only between 1 and 20 percent, although the net present value would be positive up to a 75 percent risk of loss. Such excessive loss aversion probably explains why many companies fail to pursue profitable investment opportunities.3

This degree of loss aversion is all the more surprising because it apparently extends to much smaller deals: respondents were just as averse to loss when the size of an investment was $10 million and the potential gain $40 million. Even if it made sense to be so loss averse for larger deals, it still wouldn’t make sense to be as averse to loss for smaller ones, especially considering how much more frequently smaller opportunities occur.

Executives may be limiting the investments of their companies because of economic fundamentals and policy uncertainties. But their decision making is also tainted by biases and loss aversion that harm performance and cause companies to miss potentially value-creating opportunities.

Related Articles

Why good companies create bad regulatory strategies