When COVID-19 took hold across Africa, impacting lives and livelihoods, Nigeria’s banking system was swift to respond. The Central Bank of Nigeria (CBN) took immediate steps, rolling out a stimulus package to combat the effects of the pandemic on critical sectors including cutting the interest rate on its intervention facilities from 9 to 5 percent.1 But banking in Nigeria faces a challenging road ahead. Already under pressure coming into the crisis as a result of a sluggish economy, a challenging operating environment, and increased competitive intensity—the ongoing pandemic, currency devaluation, and other macro challenges continue to place roadblocks in the sector’s path.

This article highlights the likely trends and hard choices banks must navigate in the months ahead. As the sector heads into the 2021 planning cycle, we outline strategic options they could consider now and flag key factors that could shape the industry’s next wave of transformation.

COVID-19 fueled the banking industry’s preexisting vulnerabilities

More than a decade after the 2008 financial crisis, and six years since the oil crisis, Nigeria’s banking sector continues to grapple with macroeconomic pressures including declining real gross domestic product (GDP) growth rates, rising inflation and unemployment rates, and fluctuating naira-to-dollar exchange rates caused by unstable oil prices. These factors are combining to dampen consumption and investment and curtail government expenditure, with implications for banking activities.

At the same time, policy measures to stabilize the financial system and increase lending to stimulate the production of goods and services have increased pressures on banks. The CBN’s downward fee revisions to electronic banking charges, which took effect in January 2020 and were designed to ensure the protection of consumer rights as more individuals are financially included, have had a negative effect on banks’ fees and commission income.2

Profitability is also being dampened by the Cash Reserve Requirement (CRR), which, at 27.5 percent, is among the highest in the world.3 The CRR requires banks to park an increasing amount of local-currency deposits with the central bank, and restricts their ability to lend as these reserves are only available for intervention funds. Amidst all this, the CBN’s aspiration to achieve a financial inclusion rate of 80 percent by 2020 has led to increasing competition in payments from nonbank challengers.4 Nigeria’s fintech landscape is recognized as being one of the most vibrant in Africa, with fintech investments growing by 197 percent over the past three years.5 And this shows little sign of slowing down during the crisis, as evidenced by the recent acquisition of Paystack by Silicon Valley group Stripe.6 This, in turn, has created a battleground for digital talent, already a scarce resource, and a critical enabler to help banks respond to the challenges they face.

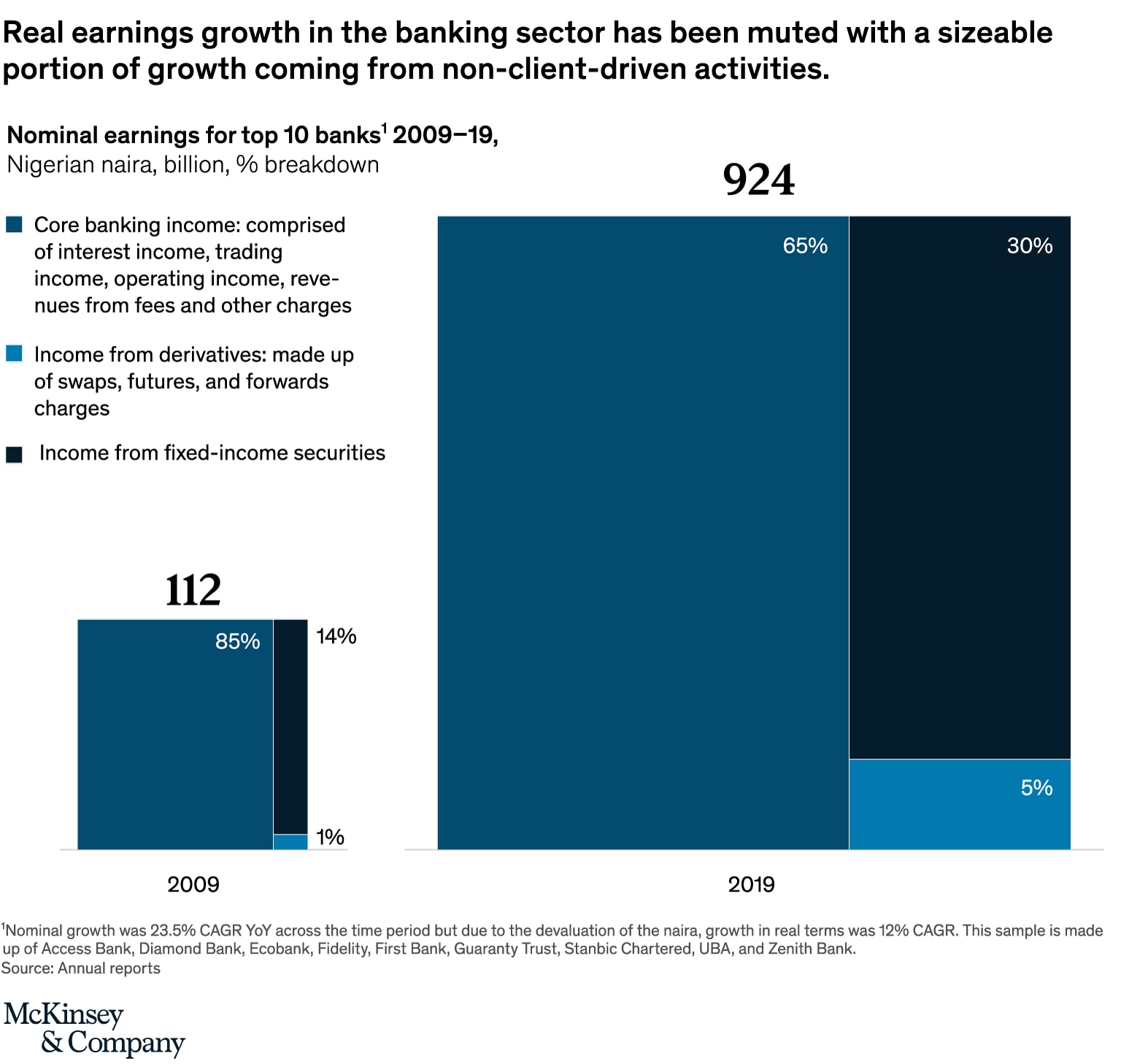

While earnings in the sector have grown by a compound annual growth rate of approximately 23.5 percent in the past ten years, actual growth in real terms has been significantly lower at around 12 percent, with a sizeable portion coming from noncore banking activities such as fixed income and derivative income (swaps, futures, and forwards).7 Derivative income in particular has become increasingly significant; the average Tier 1 bank carries around $1 billion worth of derivatives on its balance sheet and reports around $30 million as profit from trading in derivatives—approximately 12 percent of profitability (Exhibit 1).

COVID-19 is ratcheting up these pressures on banks. Restrictions on movement such as physical distancing and lockdowns have negatively impacted businesses, leading to salary cuts, layoffs, and high levels of uncertainty around business viability, while consumers have cut back on nonessential spending.

The banking sector has felt the impact largely in two ways: slowing revenues and increasing loan loss provisions.8 Revenues, such as fee income from the first half of the year, have declined by 6 percent compared with the third quarter of 2019. McKinsey analysis suggests that recovery from the COVID-19 pandemic could follow an “A1” scenario based on the most likely effect of the public-health response and stimulus implemented, where there is a dampened short-term recovery and slow long-term growth.9 In this scenario, the impact on banking performance could extend even further as banks continue to make provision for loan losses, which have gone up by 200 percent relative to 2019. Short-term and medium-term impacts on revenue pools will primarily be due to margins, where a decline in fee income will likely offset the increase in interest revenues (Exhibit 2).10 Client-driven banking revenues could fall by as much as 18 percent by 2021 before regaining a slow recovery path.11

Bold thought and action are required beyond the crisis

Banks responded swiftly to the immediate pressures of the pandemic by, for example, adjusting to a remote operating model and revisiting portfolio priorities, and have learned some valuable lessons along the way about what is possible in the “next normal.” Now, bold thought and action across four dimensions, with digital as a key enabler, could allow banks to translate the learnings of the past few months to drive sustainability beyond the crisis.

1. Scale: Define a segment or geography in which you can excel

As competitive intensity rises and margins come under increasing pressure, gaining a cost advantage becomes imperative. Scale can help bring down marginal costs as a bank gains operating leverage with a consistent increase in size. However, our analysis shows that it is not total size across the diverse markets a bank serves that enables superior performance, but optimal scale within a given geography or segment. In Nigeria, significant opportunities remain for banks to develop scale across segments—for example by targeting small and medium-size enterprises (SMEs), which have significant unmet needs in the banking sector—or by targeting geographies such as the north of the country, which has been historically underserved. Whichever geography or segment they choose to play in, banks can look for new ways to leverage digital to serve customers at scale.

2. Efficiency and productivity: Transform operating models to serve customers as they want to be served

The unprecedented scale of the COVID-19 crisis has forced banks—and indeed all members of society—to reexamine and reimagine the way they do things. The McKinsey Financial Insight Pulse survey conducted in October 2020 found that most consumers expect to increase their use of digital and mobile banking services even after the crisis, with 53 percent of consumers wanting their banks to make it easy to get a line of credit and 36 percent desiring improved bank websites to facilitate online transactions.12 In Nigeria, we’ve also seen a surge in agent-banking transactions during the crisis, opening up new possibilities for delivering services to more people at lower costs.13 However, these shifts may reverse unless steps are taken to hardwire new behaviors and attitudes.

Now is an opportune moment for banks to revisit and interrogate matters of efficiency and productivity in a disciplined manner. Actions taken out of necessity during the lockdown such as online training, virtual performance management sessions, remote working for certain jobs, and adjusted operating hours for branches could be refined for implementation on a permanent basis. Our analysis shows there is a 25 to 40 percent cost-reduction opportunity for Nigerian Banks—primarily to be found in revisiting the branch network and coverage model, increasing efficiency of spend, and increasing productivity through end-to-end digitization.14

Spend-control towers could be set up to review every spend request above a certain threshold, with the aim of not just addressing immediate efficiencies but bringing to light opportunities that need to be addressed given new models of working. This could include, for example, reviewing vendor agreements for cash management based on adjusted operating times and hours for branches or adjusting expansion plans in light of physical-distancing requirements and remote-working options. Beyond spend control, banks could accelerate end-to-end digitization to capitalize on consumer’s newfound willingness to use electronic channels. While most banks have digital options in place and have made progress in driving channel migration during the past few months, the high footfall into branches post-lockdown suggests there are still gaps. Rethinking end-to-end digital options for card subscription and renewal, PIN reset, and electronic channel issue resolution, to name a few, could unlock new growth. In addition, sales and lending processes, which have been heavily reliant on physical interaction, could be reviewed to identify automation potential, especially for SMEs. Ultimately, reimagining these processes in line with consumer requirements will lead to a redefinition of the role (and size) of the branch network and required coverage model.

3. Data and analytics: Leverage technology for commercial, risk, and operational effectiveness

Rapid shifts in consumer behavior driven primarily by physical distancing have led consumers to embrace digital options at a scale and pace not seen before. This, in turn, is clearing the way for banks to ramp up their use of data and analytics to enhance services and reduce costs. Previous McKinsey research has demonstrated that data and analytics can potentially increase a bank’s cost advantage by 10 percent and improve cost-to-income ratios by up to 15 percent, even in a recession.15 Two immediate areas to explore are risk and sales, particularly digital marketing. Nigerian banks could develop new risk models powered by artificial intelligence and machine learning that improve accuracy and efficiency and leverage real-time transaction data to understand market and customer dynamics. This could help them to explore opportunities in new segments and ramp up effective and personalized customer service, as well as to meet regulatory requirements.

On the sales front, data and analytics can drive digital customer acquisition through a combination of factors. First, by increasing qualified leads and conversions through funnel optimization and personalization and second, by streamlining roles and processes within the organization and leveraging data to improve and monitor marketing campaigns. The latter could be achieved through performance tracking and reporting and advanced return-on-investment approaches such as attribution modeling. Having an end-to-end value proposition that adequately and holistically addresses customers’ needs, maximizing the potential of data and analytics for sales is important here, or hard-won new customers will not stick.

4. Talent: Find the best people to support your shift to digital

The crisis has prompted dramatic shifts in working behavior—notably working from home models—that are opening up new avenues for banks to attract and retain the skills they need to support their shift to digital. To benefit from this trend, banks could take steps to enhance their employee value proposition, which is often perceived to be less attractive than those of technology companies that are competing for the same talent. By revisiting the development opportunities that they offer and the workplace experiences they create—including embracing flexible working—banks could position themselves as attractive employers. A commitment to inclusivity and gender parity will be critical here. McKinsey research has repeatedly demonstrated that diverse companies are more likely to outperform those that lack diversity and that more inclusive work environments produce better results and enhance the employee value proposition.16

While the four dimensions described above are valuable for all banks, specific actions taken by each bank will vary depending on its starting point, including the size of its financial “war chest” and level of maturity vis-à-vis digital trends, technology infrastructure, and its execution ability (Exhibit 3).

For financially strong Tier 1 banks with scale (resilient and market leaders), now is the time to consider investing in technology infrastructure and talent to expand beyond current customers and products. Equipping employees with the right skills and digital tools, doubling down on digital marketing, and establishing robust digital infrastructure are likely to be key enablers for success in the next normal. Furthermore, given the current environment, banks with stable balance sheets could selectively explore mergers and acquisitions, partnerships, and joint ventures across the financial services landscape that could help achieve scale and acquire new talent and customers.17

Tier 2 banks, faced with smaller balance sheets and less room to maneuver (follower and challenged), could focus on differentiation. Our research has shown that banks serving a niche segment with a specialized product suite and superior customer service have managed to sustain high-return premiums irrespective of size.18 Driving productivity by, for example, expanding shared utilities and infrastructure is also important. However, for banks that are subscale with significant challenges with their loan books and capital structure, the urgency is acute, and some may wish to consider selling to a stronger buyer with a complementary footprint or portfolio of services.

Five key factors to watch to usher in the next wave of transformation

Big moves in Nigeria’s financial-services sector have traditionally been driven by a combination of a strategic thrust (such as banking consolidation or the drive towards financial inclusion) or in response to crisis (for example, consolidation after the 2008 financial crisis)—and the regulator has had a central role to play. The COVID-19 pandemic and other ongoing pressures present the sector with a new vantage point from which to address structural vulnerabilities and position itself for sustainable long-term growth. As stakeholders respond to the crisis, we think five key factors, and the interplay among them, will be pivotal in determining how the sector evolves.

1. Cash reserve ratio (CRR) policy: Balancing stability with economic stimulus

Nigeria’s CRR ratio increased by 5 percent to 27.5 percent in January 2020 but the actual effective rate is estimated to be above 50 percent.19 Under current regulations, Nigerian banks can request to access deposit monies at specified rates to provide credit financing for development projects in the real sector (agriculture and manufacturing), but it remains to be seen if they can utilize this effectively. This perceived “fiscalization’’ of banking has led Fitch Ratings to downgrade Nigeria’s banking sector from stable to negative.20 While the regulator’s recent introduction of special bills is expected to improve liquidity in the system, banks will need to be proactive in this environment by taking steps within their immediate control including: 1) developing capabilities to identify and fund viable businesses within the intervention fund category; 2) restructuring their funding base to reflect the realities of the current CRR impact; and 3) using this opportunity to educate the frontline (and harmonize targets across the organization) on the implications of CRR and the effective cost of every deposit.

2. Banks’ capital base: Planning for another round of consolidation

To thrive beyond the crisis, Nigerian banks will need to bolster their capital levels and grow capital faster than the rates of inflation and devaluation. This will be no small feat in the current environment. Given the need to meet Basel III requirements, the possible deterioration of asset quality, and some foreign-exchange-based commitments to service, it is likely that another round of consolidation and capital raising is approaching. Three lessons from previous consolidations emerge for consideration in the next round. First, strong Tier 1 banks benefited most—big banks got bigger, benefiting from scale, flight to safety, and possibly limited distraction from acquisitions. Second, only bold, at-scale combinations were rewarded, with only one combination resulting in a Tier 1 contender. And third, banks that did nothing or too little got pressurized in an increasingly concentrated market.21

3. Portfolio restructuring: Staving off another portfolio crisis

With around $15 billion of bad loans still owed by the Asset Management Corporation of Nigeria (AMCON) to the CBN from the last financial crisis, the Nigerian economy can ill afford another portfolio crisis.22 However, there is a very real risk that in the current economic environment—with the 65 percent loan-to-deposit ratio requirement, low-interest rate intervention fund loans, and challenges with risk management practices in many banks—that this may occur. The CBN has granted regulatory forbearance to enable banks to restructure their loans at this time, and as of June, almost one-third of all industry loans had been submitted for loan restructuring.23 There are risks to consider with this strategy, notably, how many of these restructured loans are really viable? How many nonperforming loans will be created in this environment through interventions funds? And what portion of the industry trade book is at risk due to devaluation? These are indicators that will need to be monitored on an ongoing basis.

4. Regulatory collaboration: Streamlining regulation to support innovation and diversification

As banks seek to mitigate the negative impact of the crisis on their revenue streams by diversifying into new and adjacent financial-services businesses, the synchronized perspective of key industry regulators, including the CBN, the National Pension Commission, the National Insurance Commission, and the Ministry of Finance, will become increasingly critical to unlock broad-based financial services growth and true financial inclusion. A number of banks have already announced plans to expand their financial services portfolios. Seeing how well these banks fare in delivering diversified financial services will be a key factor to watch going forward.

5. Shared services: Paving the way for the next growth area

The Nigeria Interbank Settlement System (NIBSS), which is jointly owned by the CBN and all licensed banks, has played a critical role in the Nigerian banking industry over the past three decades—putting in place effective shared infrastructure to facilitate interbank payments. Today, NIBSS and privately-owned Interswitch power Nigeria’s payment ecosystem. Given the essential nature of electronic services, this infrastructure requires continuous improvement and expansion. In addition, there is scope for the industry to come together to build on this foundation, enabling the next wave of shared services. Specifically, the sector can leverage payments data—including a Bank Verification Number (BVN) database of 43 million—and other nontraditional sources of data to build new credit algorithms that can unlock lending for SMEs and other underserved segments. Together with the recent Global Standing Instruction policy, this could be the critical enabler for credit growth in Nigeria’s deposit-rich and asset-poor banking industry.24

Banks play a critical role in keeping economies vibrant and societies stable. While the situation now facing the sector is undeniably severe, the pandemic also offers stakeholders an opening to reshape and reimagine their offerings. Instead of reverting to old habits, the sector could choose to build on the learnings from these difficult times and position itself for long-term growth and sustainability. With banking revenues projected to return to precrisis levels only between 2022 and 2024, depending on whether a rapid or slow recovery scenario prevails, Nigeria’s banking sector faces a prolonged period of uncertainty. This is yet another wake-up call. The shape and the resilience of the industry postpandemic will depend on how stakeholders respond now. It’s time for bold choices and decisive execution—the faster the better.