Financial services for the unbanked are among the most promising opportunities for mobile-telecom operators hoping to counter slowing subscription growth with auxiliary offerings, such as banking, health care, and education services. In emerging markets, formal banking reaches about 37 percent of the population, compared with a 50 percent penetration rate for mobile phones. For every 10,000 people, these countries have one bank branch and one ATM—but 5,100 mobile phones.

A new focus on bringing financial services to the unbanked—those without easy access to traditional banking channels—represents a strategic shift for mobile operators. The very small deposits and loans held by poorer customers make them unprofitable for banks that use traditional delivery models. But mobile devices reduce the cost to serve customers by 50 to 70 percent, making it possible to offer financial services to a vast population once considered unprofitable.

The commercial potential for mobile operators could be significant. Our estimates reflect research, on 147 countries, that we conducted together with the GSMA (mobile industry trade group) and CGAP (independent policy and research center dedicated to advancing financial access for the world's poor). They show that about one billion people in emerging markets have a mobile phone but no access to banking services; by 2012 this population will reach 1.7 billion. Today, only about 45 million people without traditional bank accounts use mobile money, but we expect that this number could rise to 360 million by 2012 if mobile operators were to achieve the adoption rates of some early movers. By that year, the opportunity could generate $5 billion annually in direct revenue, primarily from fees for financial services such as transactions and cash out, and an additional $3 billion annually in indirect revenue, including reduced churn and higher average revenues per user for traditional voice and short message service (SMS).

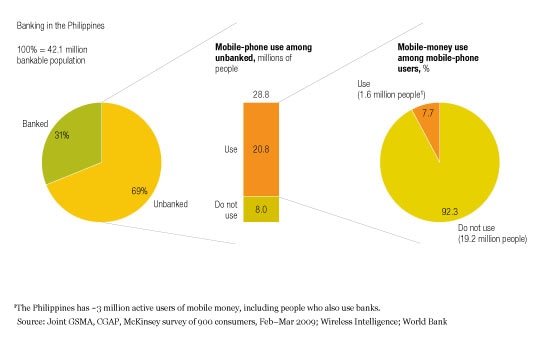

In the Philippines, for example, mobile-subscriber penetration is almost 80 percent, but banking penetration is only around 35 percent, leaving 21 million mobile subscribers with no bank account (Exhibit 1). If operators in the Philippines could bring mobile-money penetration rates among the unbanked into line with those achieved by best-practice operators elsewhere, they could acquire four million to five million new customers and add two to three percentage points of growth to their revenues. And these numbers don’t include earnings on loans and deposits, which we conservatively estimate could be a further $60 million to $80 million. Introductory mobile-money services also set the stage for additional cross-selling and up-selling in the future. In addition, eight million unbanked people in the Philippines don’t have mobile phones, and mobile money could make phone subscriptions more attractive to this segment.

Few mobile-money users

Beyond the commercial potential, mobile money can have social and economic benefits. Access to financial services lowers the cost of sending and receiving remittances, improves the safety and security of cash, and makes payments more convenient. More important, it promotes saving and borrowing, allowing families to pursue economic initiatives, generate income, and accumulate small amounts of net worth. As a result, it may make it easier for lower-income families to meet their periodic expenses, such as school fees and rent, or to buy seeds at planting time and fertilizer over the growing season. Mobile money also offers a savings cushion against expected and unexpected events, such as weddings or health emergencies.

Creating a working mobile-money model will be complicated. It calls for coupling physical assets and capabilities from two distinct domains, telephony and banking, as well as for partnerships with a variety of players—some unfamiliar—to manage cash collections and disbursements and promote adoption. Early movers that crack the code can not only capture the opportunity in their home markets but also have unique know-how that would be valuable in other geographies, either through strategic alliances or direct investment.

A strategic shift toward the unbanked

The technology needed to use mobile devices in financial services has been around for more than a decade, but the focus on using the technology to bring them to the unbanked is a recent development. In the original model, mobile phones acted as a payment and information device for people who already had bank accounts. But a strategic shift now targets the unbanked, who are being offered a broad set of financial services, including savings and credit.

In the basic model for mobile money, customers deposit funds by giving cash to agents, who credit the accounts using a special text-messaging system. Also using text messages, subscribers can make payments from their accounts to retailers in the system or transfer money to others. They can withdraw cash from any agent in the system as well. Loans and other services follow a similar pattern.

SmartMoney and GCash (in the Philippines) and M-Pesa (in Kenya) are at the leading edge of this shift, which is now gaining momentum. In our study with the GSMA and CGAP, we estimated that 120 operators in 70 markets will deploy mobile-money offerings within the next 6 to 12 months. Half of the operators we surveyed said that the unbanked were their principal target. But except for a few notable cases, most of these operators are in the early stages of development; nearly three-fourths have been at it for less than two years.

Understanding the unbanked

Most mobile operators know little about the financial needs and habits of the unbanked. Limited information is available about their saving, borrowing, and payment habits; what they want; whom they trust; and how they buy. Some operators have gained insights through trial and error, but this approach is costly and slow. To help fill the gap, we took a close look at several markets, including the Philippines and India.

In general, the unbanked—even the lowest-income segments—actively use informal financial services. Without access to traditional banks, many turn to their families or communities or to pawn shops when they need credit. Nearly 90 percent store money at home, with a household member, a friend, or a village savings club. Some buy assets, such as cows or chickens, as a store of value. These informal channels tend to be unreliable and expensive.

Nearly 60 percent of unbanked mobile customers in the Philippines keep some form of savings, with a median balance of $40 (about 15 times the average daily income). Our survey also showed that 13 percent of unbanked Filipinos borrow: 55 percent from family or friends, 17 percent from microfinance institutions, and 13 percent from moneylenders. In India, about 20 percent of the unbanked borrow, but in that market moneylenders are the primary source (60 percent of these loans). Family and friends account for about 12 percent.

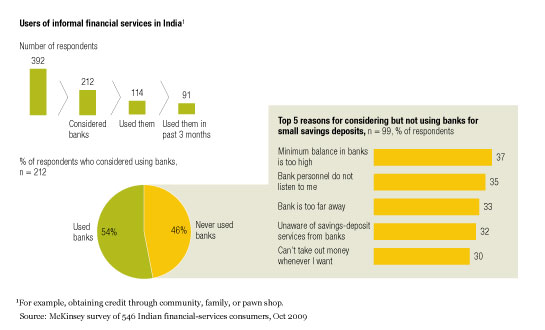

Low-income households in both countries cited many of the same reasons—primarily liquidity—for using informal channels. Such households want quick access to funds, so the proximity of outlets and round-the-clock availability are essential. Few banks can meet these needs, because typically outlets are centered in urban areas and the unbanked mostly live in the countryside. Although more than 50 percent of the unbanked in India have considered using banks, only about half have done so, and our survey showed that distance is one of the top five obstacles (Exhibit 2). These households also need flexible repayment terms, and here again banks fall short. Even when low-income workers do have access to a nearby traditional bank branch, they can find the environment alien and intimidating.

Bank avoidance

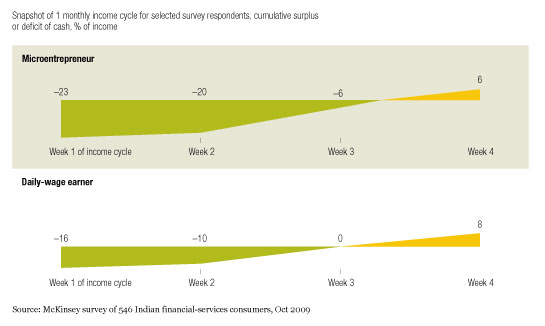

Ethnographic testing and focus groups provide nuanced insights into demand in India. The primary requirements of its low-income households go beyond simple savings vehicles. Many households are looking for a way to help them manage their money or cash flow. But for these consumers, money management is different from pure long-term savings or credit. Its principal focus is balancing times of cash surplus and cash deficits over a typical salary cycle—for example, 30 days.

Rural families, for instance, take in large sums at harvest time. Without a vehicle for savings and cash flow management, they generally store harvest funds at home, and the cash gradually dwindles as it’s tapped for discretionary purchases. When the time comes to plant seeds for the next growing season, there’s not enough money on hand to pay for them. As a result, these families turn to informal lenders, whose rates can be quite high. Many people often run deficits for two to three weeks every month. Small entrepreneurs may be in the red for much longer periods (Exhibit 3). The ensuing debt cycle is hard to break.

Empty pockets

Looking at the requirements of low-income people who already use mobile-money services, we see that products for sending and receiving money are important as well. Many young men and women seek jobs in the larger domestic cities and abroad, and these people need a way to send money home. Money transfers are the most widely used mobile-money service in the Philippines: more than 50 percent of current subscribers use it—40 percent of them more than once a week. The alternatives are perceived as more expensive (money transfer agents) or less reliable (using bus and taxi drivers to deliver cash).

Our research shows an openness to using mobile devices to meet some of these needs. Nearly two-thirds of Philippine unbanked mobile subscribers knew about mobile money, and almost as many—about 60 percent—expressed no misgivings about trying it. Most observers assume that low-income households are cash poor, so it’s surprising that nearly 55 percent of those we surveyed were interested in savings products, compared with 17 percent in insurance and 12 percent in straight credit.

Lowest tiers highly interested

Despite a common assumption that people with little money are relatively indifferent to banking, our work showed that even the lowest-income segment has a strong interest in mobile money. In the Philippines, about 8 percent of the unbanked have subscribed to it. Of these 1.6 million customers, almost one in five—300,000—come from households at the base of the income pyramid: those earning less than $5 a day. While the numbers remain low, several promising tendencies suggest an eagerness to take advantage of mobile money.

Of the lowest-income households we surveyed, about 65 percent said they wanted to use mobile money as a savings vehicle, compared with 50 percent across all income groups. Also, a larger portion of the poorest customers save, and they save nearly as much as the others do. Overall, 6 percent of subscribers to mobile money use it to store value, and their median balance is about $40. But among the poorest segment, about 10 percent have accounts, with an average balance of about $31. Mobile money may even be encouraging the lowest-income groups to save: those who save using informal methods report lower average balances—for example, 44 percent, with an average balance of $19, say that they save at home, and 9 percent, with an average balance of $26, save with a village savings club. It’s not clear whether (or how) mobile-money accounts encourage people to save more than other vehicles do or if they simply attract customers with a higher propensity to save. But this noteworthy correlation provides a promising indication of the demand for and value of a mobile phone–based savings vehicle among the poorest income segments and its impact on their lives.

Overall, the results are encouraging for mobile operators and banks. They show that the unbanked desire to use a range of financial services, particularly savings, and—especially among the lowest-income groups—are comfortable using mobile devices to get them.

Getting to market

To make mobile money for the unbanked commercially viable, operators must sign up 15 to 20 percent of the addressable market. This range is well within the experience of early movers, whose take-up rates have varied from 1 percent to 35 percent. Regionally, the greatest success has been in Eastern Europe (22 percent), the lowest in Asia (around 5 percent).

Mobile operators have distinct advantages. In surveys, nearly two times more respondents recognize mobile brands than bank brands. Respondents also tend to trust mobile brands more than banks. The issue of lost airtime is prominent in the minds of respondents, however, and could be a knockout factor if it isn’t definitively addressed.

Mobile money operates at the intersection of banking and telephony, so skills in both are needed to get products to market. This requirement creates three challenges that any successful model must overcome. Mobile-money operators need a distribution network that can take in and dispense cash from accounts. Operators must work to shape regulations so that they don’t undermine the economics of mobile money. Finally, they need access to financial-services capabilities, most likely from a partner financial institution.

Low-cost distribution, leveraging unique partners

Consumer adoption will turn on the extent of access. Mobile-money operators must create an access network to take cash for deposits and payments and to distribute it for withdrawals and loans (known in the industry as cash-in/cash-out). There must also be a process and location to take applications for other services, such as loans.

Our experience shows that when a cash agent is more than 15 minutes away, mobile money has relatively little appeal, and customers use it once or twice a month. But when the agent is less than 10 minutes away, usage rises to 10 times a month—and for those within 2 minutes of an agent, to 30 times a month. Clearly, proximity of access is vital for getting the unbanked to move from informal financial services to mobile money. Operationally this means creating a low-cost, ubiquitous distribution network.

Mobile operators are experimenting with several ways to create widespread, low-cost distribution. All these approaches involve the use of partners, some of which may not be familiar. One option relies on existing retail networks that sell prepaid cards. Smart Communications in the Philippines, for example, has one million airtime resellers (the whole country has only about 5,000 bank branches). Taking advantage of existing relationships, mobile operators could find tapping into this network, or at least a part of it, relatively easy. Many of these retailers are street-side kiosks, however, and may have difficulty meeting the physical and process requirements associated with security standards and customer enrollment.

A second option is to ally with partners—for example, microfinance institutions, post offices, ubiquitous retailers (including government-owned chains), utility payment centers, or gas stations—that already have the reach needed to access target customers. Operators would provide the basic product design, service requirements, and back-office processing, while the partners would run the cash-in/cash-out facilities. The fundamental idea is that the partner would have an existing distribution network, allowing the mobile operator to avoid footing the bill for the outlets.

Operators may also develop a network from scratch. With the help of airtime retailers, for example, exclusive agents working directly with subscribers to collect and distribute cash could be based in villages and made responsible for specific territories. Although complex to create, a village-based network would have the local knowledge needed to evaluate credit requests and pursue collections. Other industries have used similar models. GlaxoSmithKline has enlisted midwives to distribute specialized vaccines to infants in the Philippines, for example, and rural women in India work for Hindustan Unilever as sales representatives in their communities.

The option (or mix of options) fitting an individual market depends on finding the right balance among three imperatives: customer service skills beyond basic retailing, low costs, and compliance with security and financial regulations.

Shaping regulation

Because the distribution partner is engaging in financial transactions, there will be pressure to put such networks under financial-services regulation, at least to some degree. The broader the product offering—such as money transfers and savings and credit—the greater the pressure to bring these operations under the financial supervisory umbrella. Regulators will naturally require compliance with “know your customer” and anti-money-laundering rules to contain fraud and other criminal activities. Some operational aspects will also be subject to safety and soundness guidelines, including regulatory-capital rules.

Mobile operators will need to help regulators build a framework of rules proportionate to the services on offer. While there are important risks to consider, bringing mobile-money services under the same requirements facing traditional banks would undermine the economics. The objective should be to create a regulatory regime that enables operators to extend formal financial services to the poor and is appropriate for the level of risk created.

In many countries, regulators have already signaled a willingness to work with mobile operators to find this balance. Our global study showed that 60 percent of the mobile operators believed that regulators are indeed open to designing rules that allow mobile money to serve its target customers. Yet 80 percent didn’t think that regulators would grant low-value transactions exemption from anti-money-laundering rules.

In helping to create an appropriate regulatory framework, mobile operators should ally with an industry many might consider their natural rivals: banks and other financial institutions. Both industries are adept at working with governments to craft regulations, however, and since using mobile devices to bring financial services to the unbanked is new territory, there’s little existing turf for either industry to protect and far more common ground. Indeed, successful models will probably require partnerships between companies in both industries. A first step would be to jointly develop a clear view of the full set of regulatory innovations that would support mobile banking while addressing legitimate risks and to articulate the social and commercial benefits of adopting those rules. Few players have gone down this road so far. Bank of the Philippines (BPI) and Globe in the Philippines are notable exceptions.

Acquiring the right skills

Financial-services capabilities are required across the mobile-money value chain, from designing products to managing the flow of funds to handling clearing and settlement. To offer mobile money, mobile operators must acquire these skills quickly.

In the early going, many have opted to build such capabilities internally. While autonomy may bring some advantages, such as not having to share profits, these may be outweighed by the disadvantages. Financial capabilities could take months or years to develop and deploy, allowing speedier competitors to break ahead. What’s more, this approach would limit the range of products a mobile operator can offer. In addition, interest-bearing deposits or credit offerings will inevitably bring a mobile-money service under the oversight of banking regulators, which will either prohibit them or require some sort of banking license.

We believe that successful mobile-money operators are more likely to partner with a financial institution to gain the needed financial-services capabilities and license quickly. Early movers are trying two approaches. In the first, the mobile operator partners with an established financial institution that offers the needed capabilities, providing for a fuller product offering. Keeping costs under control is crucial, since burdening a mobile-money service with fully loaded banking costs will scuttle it. The partners must therefore work out an agreement that bases costs on the specific set of services provided by the mobile-money operation. This model has been deployed by Globe and BPI in the Philippines and is being explored in other markets. The idea is to leverage the financial capabilities of the bank partner and to build up a special-agent network for distribution.

Mobile operators could also consider founding a bank, possibly as a joint venture with an existing one. Its sole purpose would be to provide the core banking capabilities for the mobile-money business and to manage regulatory compliance, back-office operations, product design, and the distribution network. Such a bank could control costs relatively well, since it would avoid legacy costs or, in the case of a joint venture, would be structurally separate from the partner bank. Some models may not require a full banking license.

As subscription growth slows, mobile operators are turning to auxiliary services like mobile money, which allows them to build on their technical expertise, customer base, and, in part, existing distribution networks. A new strategic direction that focuses on using mobile devices to bring financial services to the unbanked has shown significant potential in early markets.

But to succeed, mobile operators must gain distinctive insights into low-income consumers, develop a widespread and inexpensive distribution network (sometimes with unfamiliar partners), and acquire financial-services skills. It’s a tall order, but players getting it right can add two to three percentage points to revenue growth in their home markets—a huge benefit amid declining growth rates for traditional mobile services—and create a platform to move into other geographic markets.