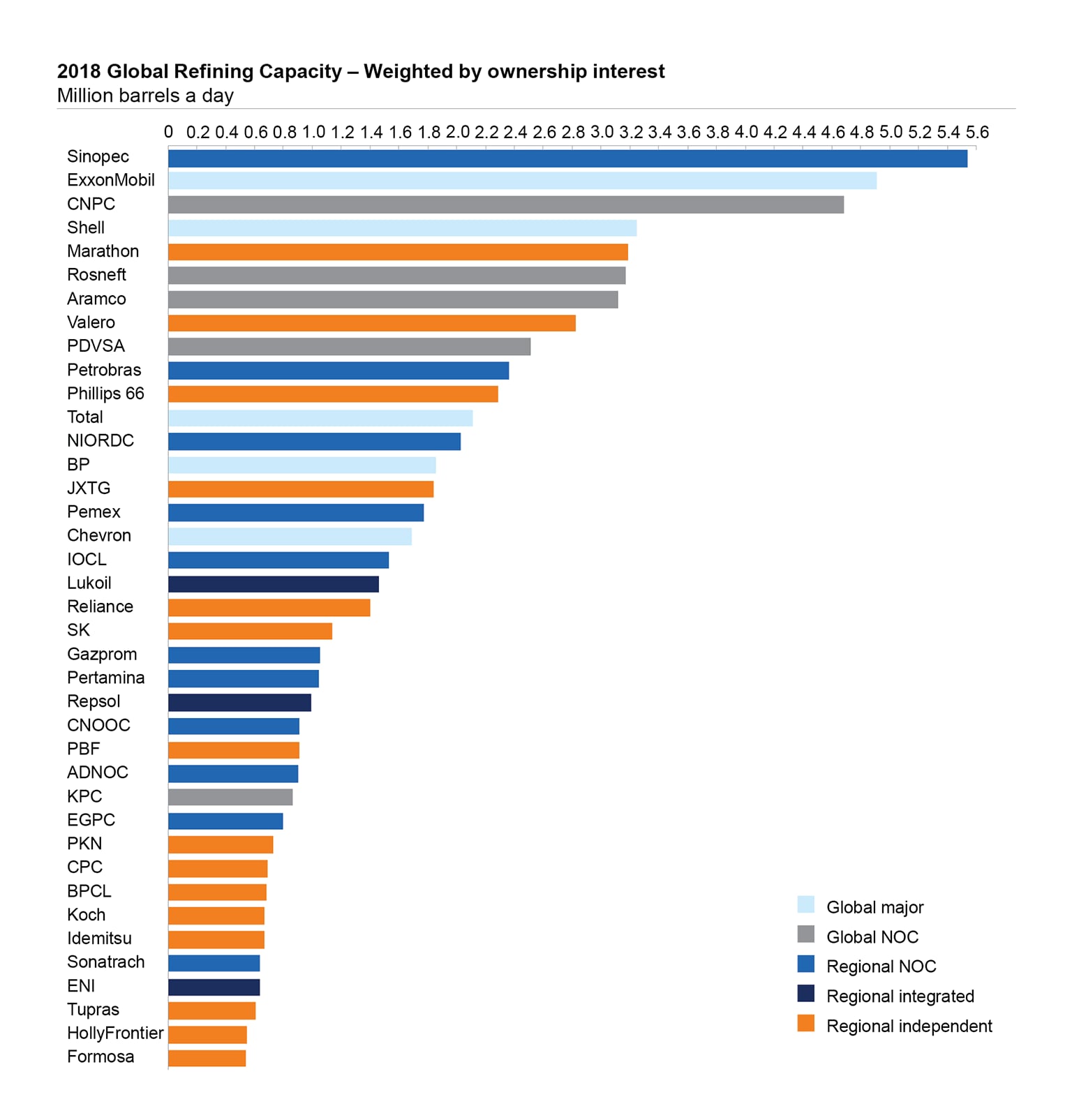

With the completion of the merger of Marathon and Andeavor, we now have a new number one independent refiner in the US. And, with over three million barrels per day of refining capacity, the merged company is the first North American independent in the global top 5.

On October 1st, Marathon Petroleum completed its merger with fellow North American refining independent Andeavor (formerly known as Tesoro). With a combined capacity of slightly over three million barrels a day across a portfolio of 16 refineries in 13 states, this creates a new number-one refinery in the US market. Valero, with 15 refineries totaling about three million barrels a day, is the second-largest refiner by capacity (see exhibit).

For the first time, this also puts a North American independent refiner among the global top 5, which has until now been dominated by the majors and national oil companies (NOCs).

Based on aggregate refinery capacity, the world’s largest refiner is Chinese NOC Sinopec, with about 5.5 million barrels a day of refining capacity across 28 refineries. Fellow Chinese NOC CNPC is not far behind, in third place, with slightly over 4.5 million barrels a day across 35 refineries. Global majors ExxonMobil and Shell hold the number 2 and 4 spots, respectively.

With slightly more than three million barrels a day, the newly enlarged Marathon captured fifth place, displacing Russian NOC Rosneft. It also knocked the previously highest-ranked independent Valero down a spot from number 7 to number 8.

The Marathon-Andeavor combination follows an ongoing trend that is sorting the world’s refiners into these five categories:

- Global majors – The original big boys on the global refining stage continue to see their global portfolios shrink in overall size, number of plants, and share of the market.This has mostly come from the sale of smaller, less-strategic plants and minority interests in joint ventures. For ExxonMobil, Chevron, and Shell, this largely coincided with further investment to expand and enhance remaining core assets in major hub markets such as the US Gulf Coast, Northwest Europe, and Singapore.

- Global NOCs – A number of NOCs have risen in the rankings through a combination of new investments at home and new ventures abroad.This includes the Chinese giants Sinopec and CNPC. Also, in this category is Aramco, which continues to add new plants in Saudi Arabia and build and acquire capacity in Asia and North America; and Rosneft, which has ventured overseas more through acquisition.

- Regional NOCs – NOCs focused on their home markets are more prevalent.These players have seen growth constrained by the limits of their local markets and, in many cases, difficulties in executing major capital projects, such as in Mexico and Brazil.

- Regional independents – The most dramatic growth stories have been independent refiners focused on a single national or regional market. The best example of this is North American independent refiners. Here growth has come largely through acquisition of either smaller independents or picking up the assets spun off by the majors, such as Marathon’s acquisition of the Texas City refinery, which took place in 2013.

- Regional integrated – Smaller, more regionally-focused integrated players have shrunk as several of them have separated their upstream and downstream businesses, which has had the effect of converting their refining business into regional independents.One example of this would be ConocoPhillips, which split off its downstream business to become Phillips66, now one of the largest independents.

Moving forward, we likely will see global NOCs getting bigger and the global majors shrinking the size of their downstream portfolio. The global NOCs seem committed to a strategy of expanding both at home and overseas, through new capacity and acquisition. The global majors meanwhile still have assets in their portfolios that, history would suggest, are candidates for sale when the time is right.

The dramatic growth of the regional independents, at least in North America, may be coming to an end. Most are now approaching a size and level of regional concentration that may limit their room to grow in their home markets. And so far, they have not shown an appetite to grow overseas.

What could this mean for the industry? If past behavior is any indication, a shift in critical mass towards the global NOCs is likely to mean a greater tendency towards investment in new capacity with a bias towards more complex and more chemically integrated capacity. If true this suggests tougher times for the industry with more intense competition to serve shrinking export markets.

For more information, please visit our Energy Insights page.