The decision in early July to cancel the Atlantic Coast Pipeline (ACP) raises questions about the outlook for natural gas in North America. The ACP, which would have connected natural gas produced in the Appalachian Basin in West Virginia to consumers in Virginia and North Carolina, was cancelled due to project cost escalations after six years of debate and litigation.

In the short term, the effect is likely to be relatively minimal and regionally concentrated. However, in the longer term, the trend of northeast pipeline project delays and cancellations could limit new investment in Appalachian gas infrastructure and subsequently threaten gas production. In this scenario, operators in western Canada are likely to respond by increasing production to meet US demand.

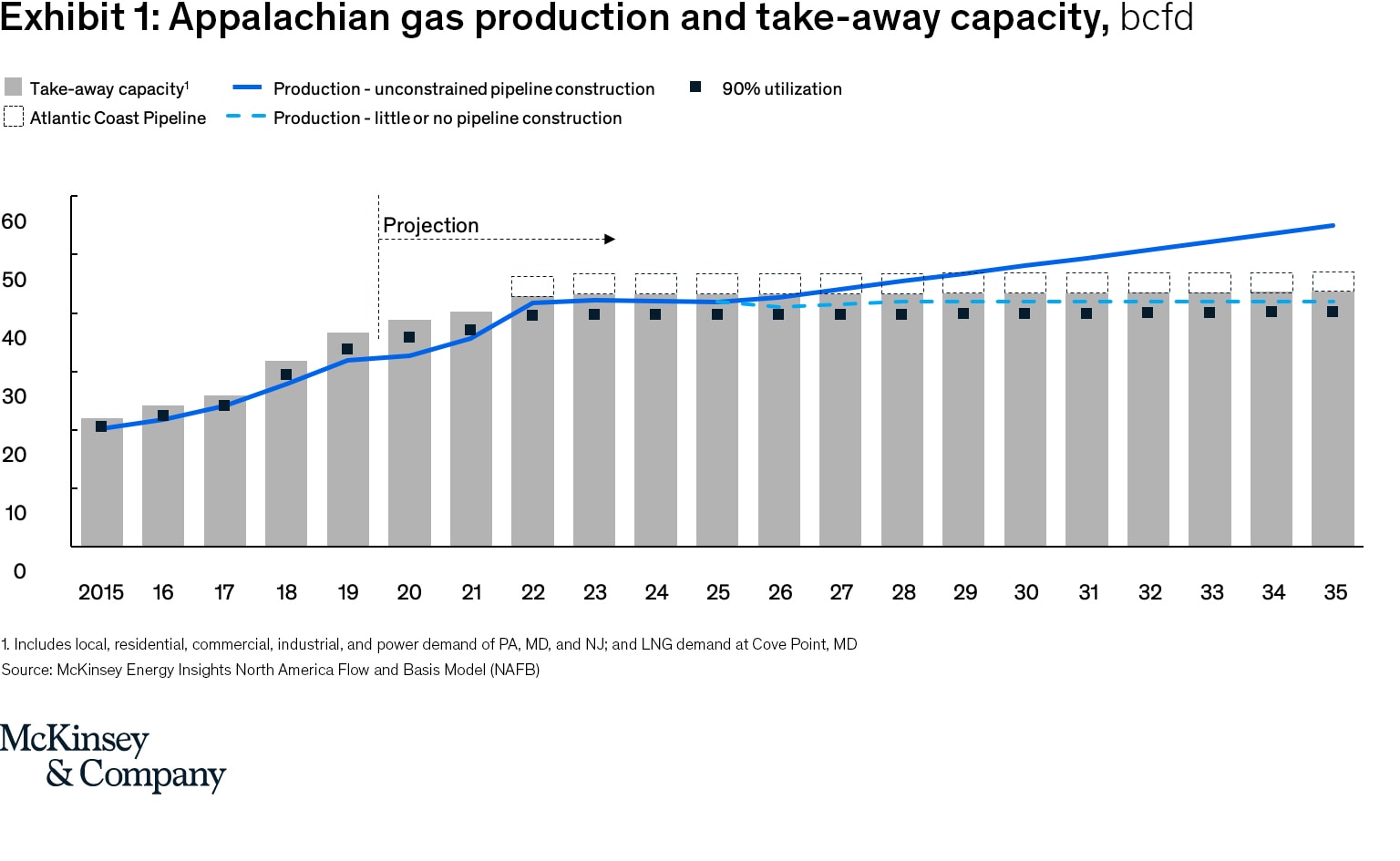

In large part because of the low break-even costs of natural gas produced in the Marcellus and Utica shale plays ($1.6 to $2.3/mmBtu)1, production in the Appalachian Basin grew rapidly—from 3 billion cubic feet per day (bcfd) in 2010 to 31 bcfd in 2019. This growth strained pipeline capacity, creating bottlenecks. New pipelines were built, increasing capacity by about 17 bcfd from 2015-20; this lessened volatility and stabilized prices.

However, pipeline utilization is projected to exceed 90 percent by 2022 as Appalachian gas production continues to grow (Exhibit 1). The 600-mile ACP would have added 1.5 bcfd more capacity. With its rejection, and with the COVID-19 crisis adding a new element of uncertainty, the region may soon become bottlenecked once more.

This article examines the likely consequences of the cancellation of the ACP2. We argue that the cancellation of the ACP can be absorbed without substantial pricing impact, but if the trend of limited pipeline construction continues, the ripple effects could be significant.

Short-term implications of the cancellation of the Atlantic Coast Pipeline

In the next few years, gas production in the Appalachian Basin is likely to be constrained—unable to grow due to lack of pipeline capacity—thus reducing the potential of the basin to meet North American demand.

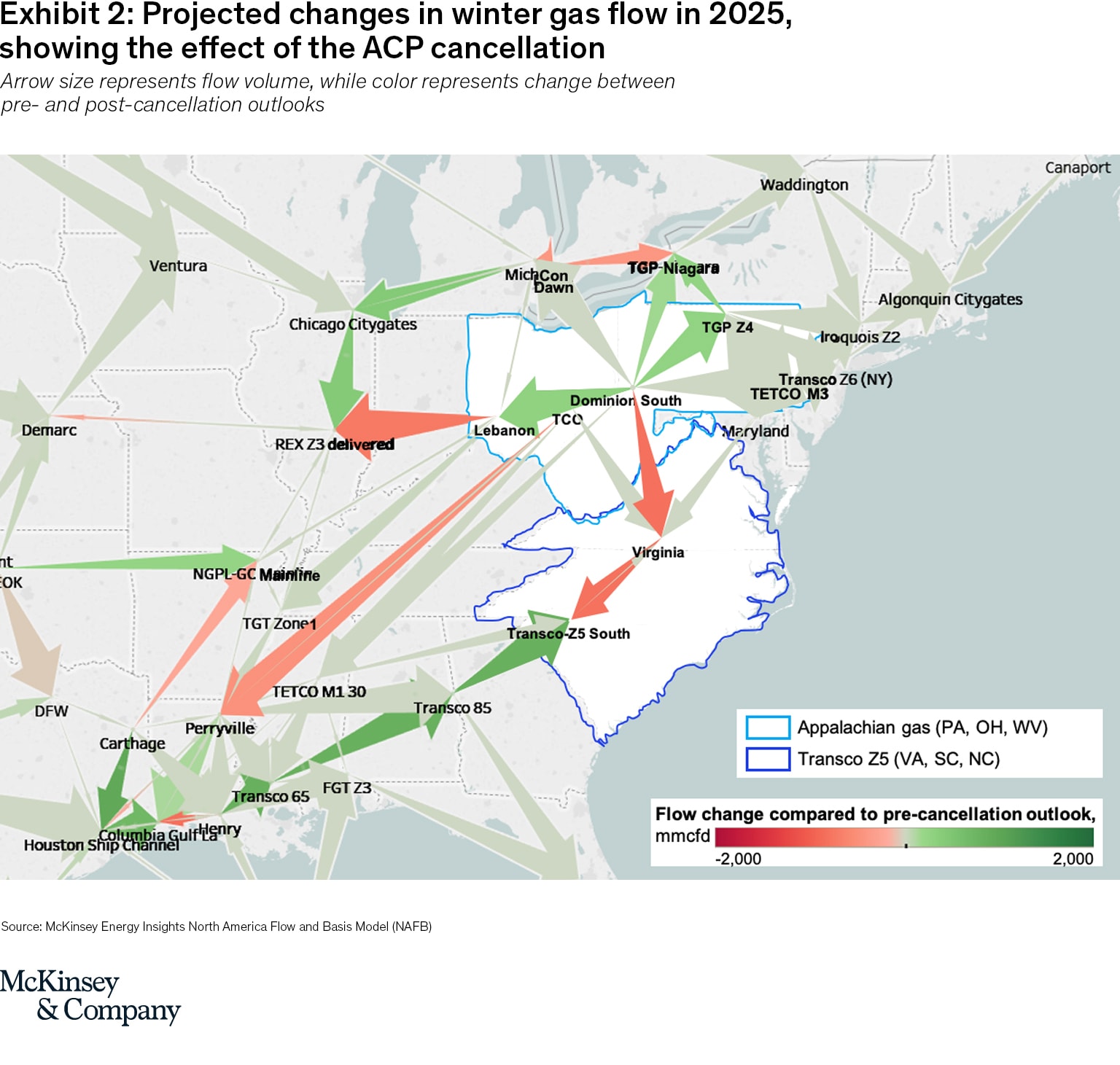

Gas production flowing through the ACP would have brought Appalachian gas to the Transco Zone 5 region—comprised of North Carolina, South Carolina, and Virginia. Without the ACP, there is likely to be insufficient pipeline capacity to meet Transco Z5 market demand from Appalachia; instead gas will have to flow from the Gulf Coast (Exhibit 2). Less gas flow to the Transco Z5 region could create an oversupply within Appalachia, decreasing local gas prices at Dominion South – a common marker for Appalachian gas prices. Lower local gas prices would compress supplier margins, leading to lower-than-expected production growth in Appalachia. Given the drop in supply, gas flows from Appalachia to the Gulf Coast would fall. Flow patterns in the Northeast and upper Midwest would then change as gas supplied from other hubs is displaced by cheaper gas from Dominion South.

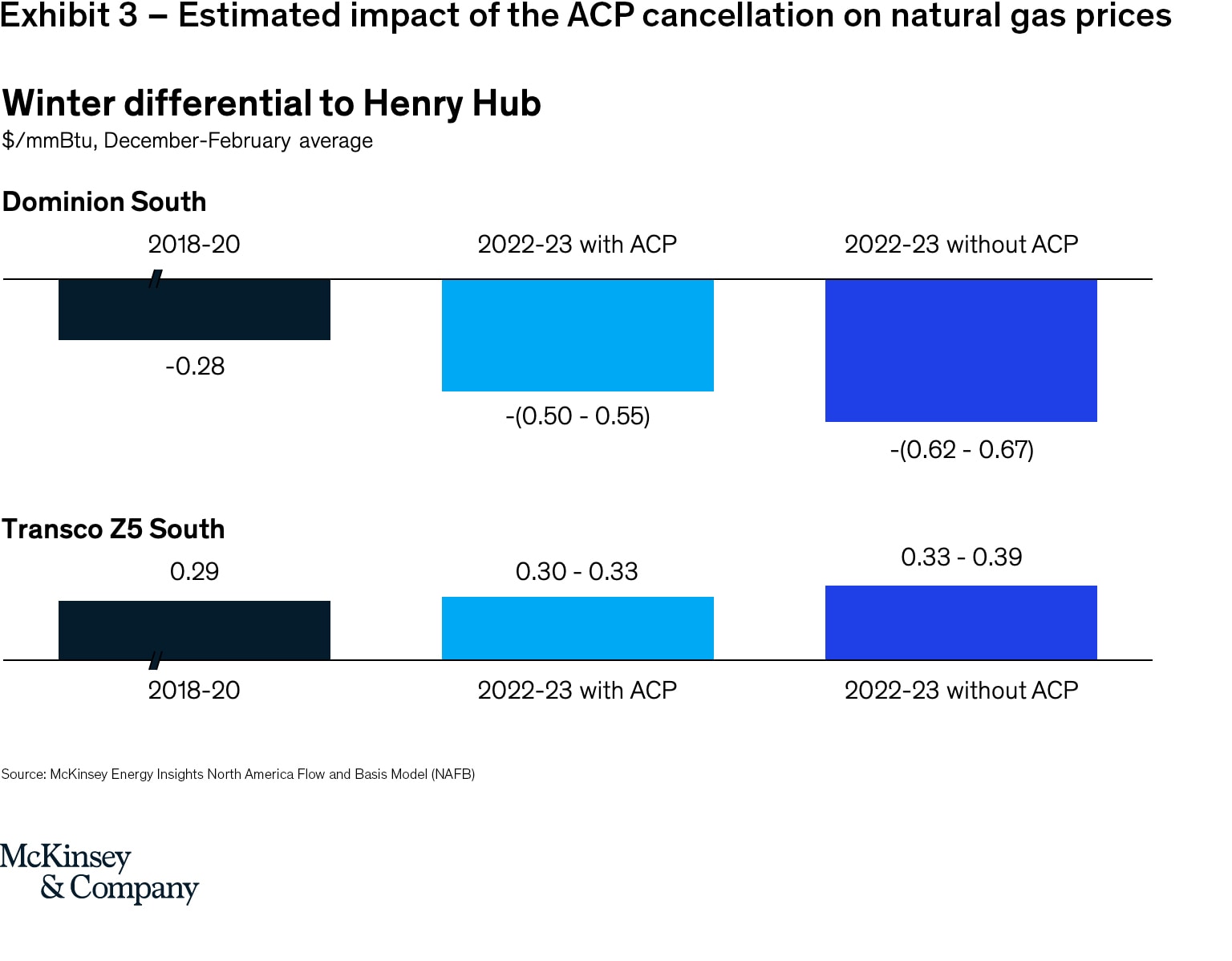

Our analysis estimates that gas prices in winter 2022-23 will likely be four to eight cents per mmBtu higher at Transco Z5 South compared to forecasts made prior to the ACP cancellation (Exhibit 3). The minimal price impact can be explained by several factors. Primarily, the Mountain Valley Pipeline, now under construction, should provide additional capacity from Appalachia to the Transco Z5 region. (The would-be owners of the ACP—Dominion Energy and Duke Energy—are negotiating the purchase of capacity on the Mountain Valley pipeline.) In addition, demand for power generation, comprising almost half of total gas demand in the region, is expected to increase only about 0.2 bcfd by 2025. Finally, Virginia signed an act requiring local utility providers to generate 100 percent of electricity from renewable sources by 2050, which could discourage gas power generation and consumption.

As for Dominion South, we estimate that prices in winter 2022-23 will be on average 12-17 cents per mmBtu lower compared to forecasts made prior to the ACP cancellation (Exhibit 3). In general, price in a producing region is set by the difference between price at the demand location and transport cost. Price at the demand location is held stable by competition from multiple supply paths. As a result, price at an oversupplied producing region decreases as the pipelines become full and transport costs go up.

Long-term implications of the cancellation of the Atlantic Coast Pipeline

If enough new pipelines are built, gas production in the Appalachian Basin could continue to grow to meet demand. However, in recent years, a number of proposed pipelines have faced delays or cancellations; if that trend continues, the lack of midstream infrastructure could constrain production in the region.

Here is how these two scenarios could play out:

Unconstrained pipeline construction: Beginning around 2025, more pipelines are built, and the Appalachian Basin continues to supply growing liquefied natural gas (LNG) demand in the Gulf Coast (an estimated 12 bcfd to 2030). In effect, this would constitute a continuation of recent history: as pipelines get full, bottlenecks occur, so more pipelines are built, prices increase, production grows, and eventually new bottlenecks occur, and so on.

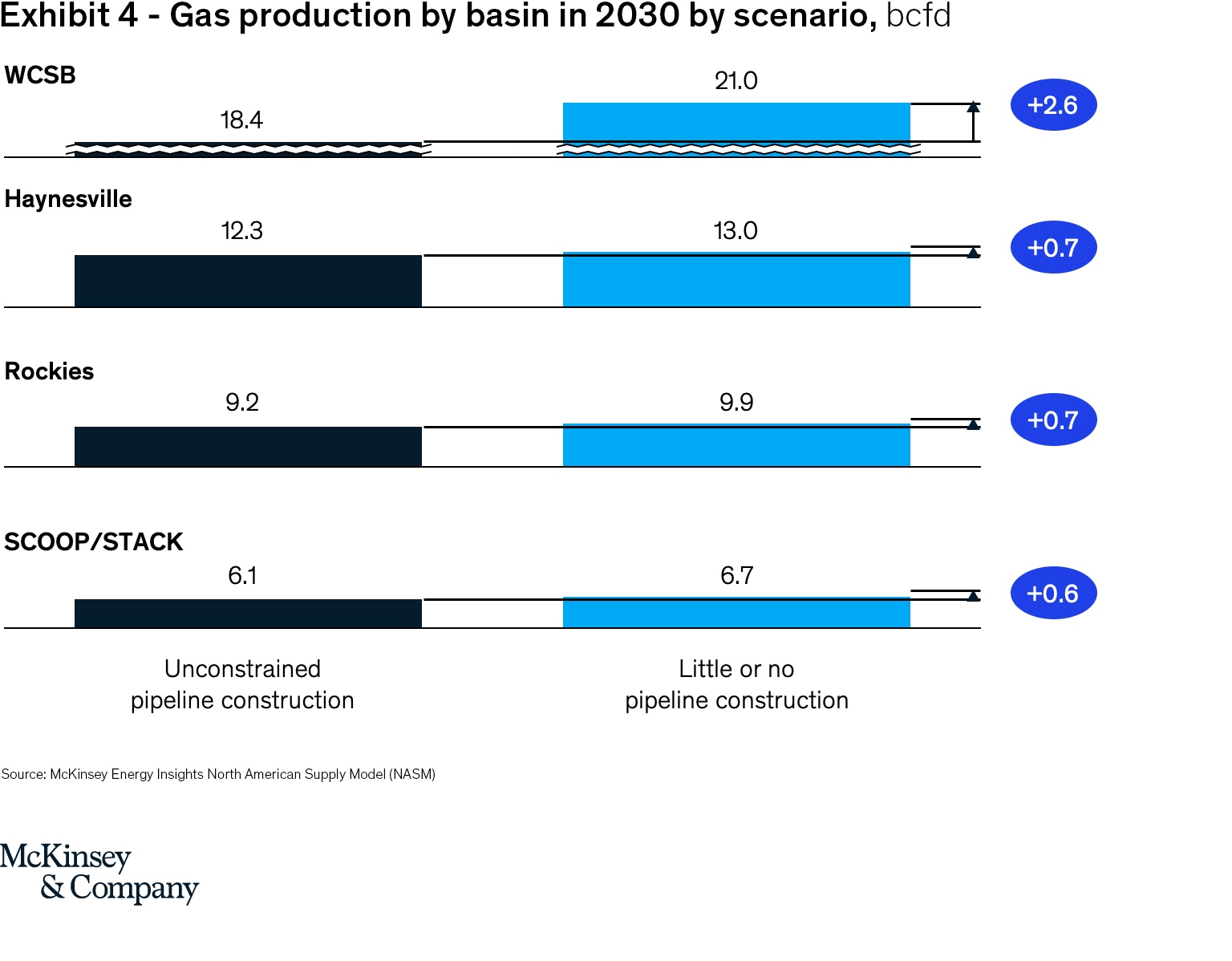

Little or no pipeline construction: In this case, Appalachian gas production would level off at 42 bcfd by 2022, with no new pipelines constructed to relieve bottlenecks. As a result, production patterns would change. Low-cost assets in the Western Canada Sedimentary Basin (WCSB) could see production increase by as much as 2.6 bcfd in 2030 compared to the unconstrained case (Exhibit 4). In addition, other shale basins with access to the Gulf Coast, including Haynesville (Texas/Louisiana), SCOOP/STACK (Oklahoma), and Denver-Julesburg (Rockies), could also help narrow the remaining demand gap.

Pipeline flows across the United States and Canada would also change as a result of these shifts in production (Exhibit 5). The greatest impact would be on gas from Western Canada, which has sufficient pipeline export capacity; flows to the US Midwest and west coast would increase drastically. Incremental production growth in US shale basins would flow toward the Gulf Coast, replacing production from Appalachia.

Understanding what happens next

Growing uncertainties in gas pipeline constructions on top of unprecedented disruptions in supply and demand from COVID-19 pose a number of critical questions to answer in coming months.

One set of questions has to do with regional pipeline constraints.

- Will other pipeline projects face additional delays or challenges, increasing the likelihood and severity of regional pipeline constraints? What would it take to develop additional pipeline capacity out of Appalachia? How many delays will turn into cancellations?

- How will pipeline constraints impact the longevity of operators in the Appalachian Basin, many of whom are already financially distressed? Will lower local prices trigger more bankruptcies?

Another set has to do with how natural gas prices will be affected.

- How will US LNG project development and returns on invested capital be affected? Will projects coming online after 2025 struggle to source low-cost gas?

- How will a challenged natural gas industry impact investment in renewable energy sources in the US?

The answers to these questions will help to shape the future of the North American natural gas market.

About the author(s)

Adam Barth is a partner in the Houston office, where Autumn Hong is an associate partner and Alastair Nojek is an analyst. Dumitru Dediu is a partner in the Boston office.

The authors wish to thank Brandon Stackhouse, Yasmine Zhu, Rupa Ramamurthi, and Kelsey Sawyer for their contributions to this blog post.

1 One million British thermal units, a measure of the energy content in fuel.

2 Projections are made using McKinsey’s “A1 COVID impact scenario”, in which the virus recurs, and there is low long-term growth and muted world recovery.