This past year was significant for the global LNG market, with plenty of twists and turns, winners and losers. With 2019 underway, let’s reflect on the previous year to see what went right and what didn’t.

Over the course of 2018, we used LNGFlow, our LNG fleet utilization and movement tracker to pinpoint the most major developments in the global LNG market. We compared market dynamics from 2018 with dynamics from the same period a year ago to identify the biggest importers and exporters and emerging trends to keep an eye on. From this analysis, we’ve ranked 15 key insights from the past year and explain what they reveal for the upcoming year.

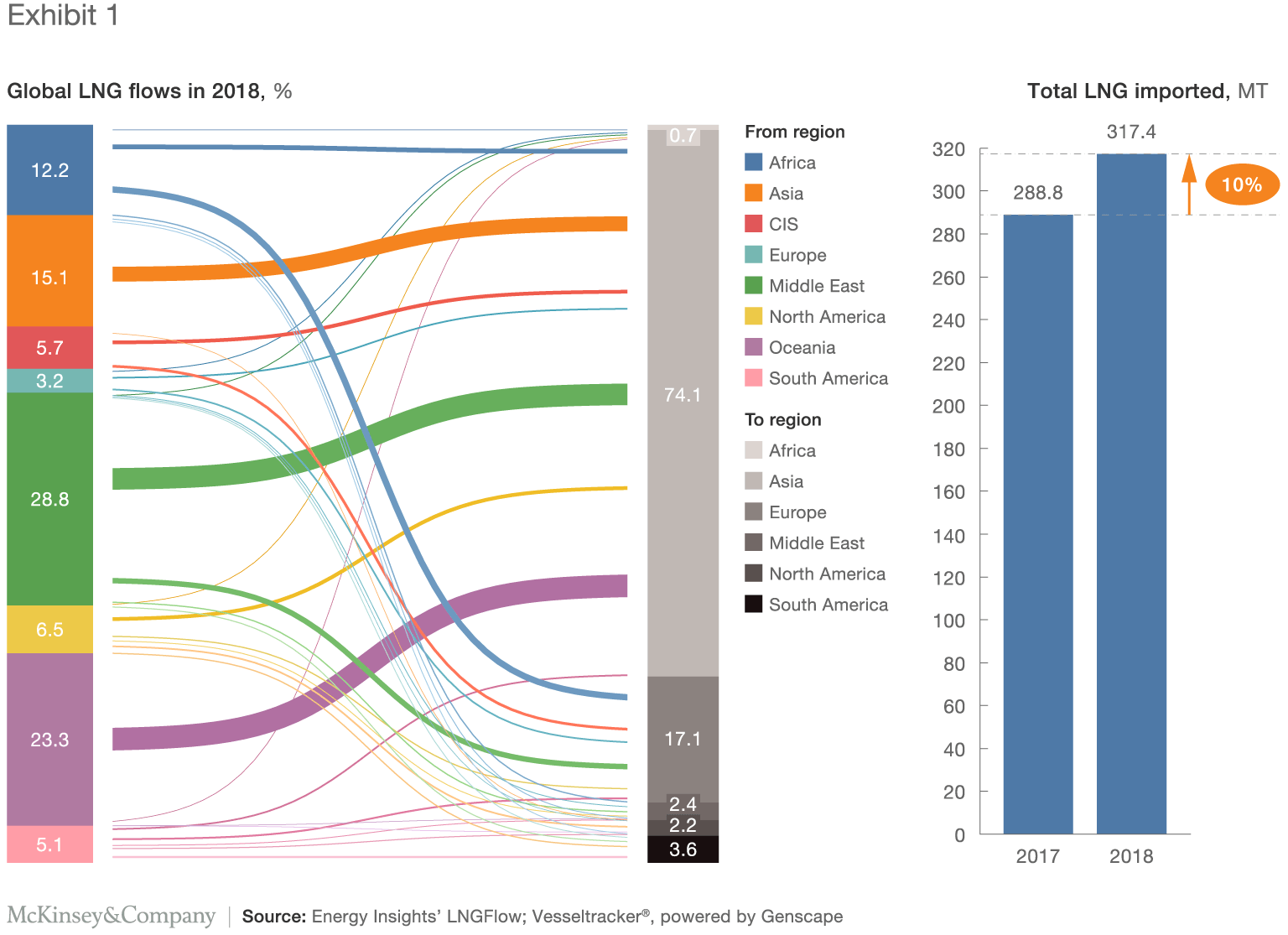

1. The global LNG market is still on the up and up, growing 10% year-over-year in volumes delivered. This represents an increase in the 9.5% growth achieved in 2017. In total, imported LNG volumes reached 317 MT in 2018, compared to 289 MT in 2017.

2. All eyes are still on Asia, the main importer—to the tune of ~75% (239 MT)—of LNG volumes shipped globally.

3. Within Asia, 143 MT (45% of global imports) of those volumes went to Japan, South Korea, and Taiwan, while 54 MT (17%) was sent to China.

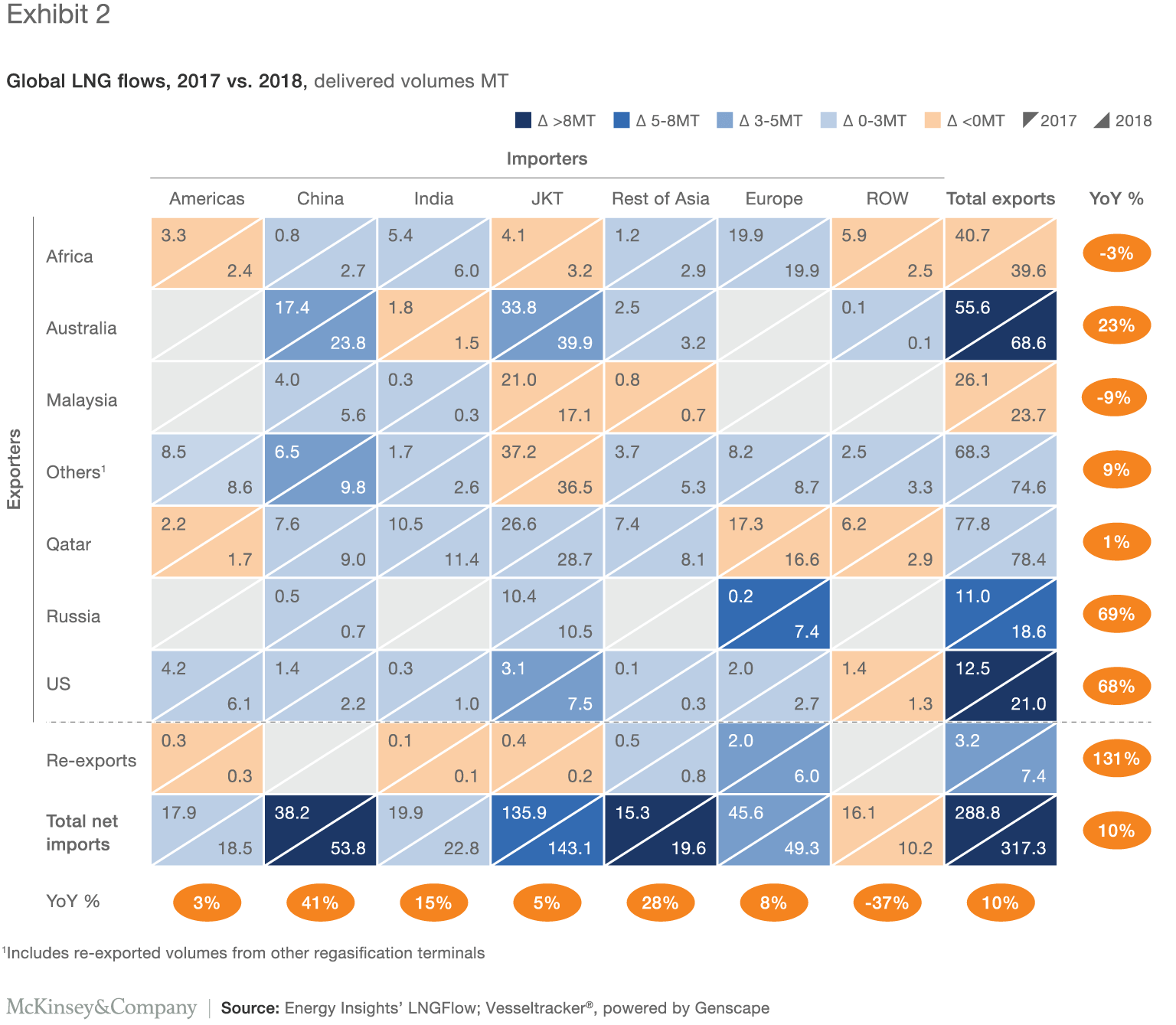

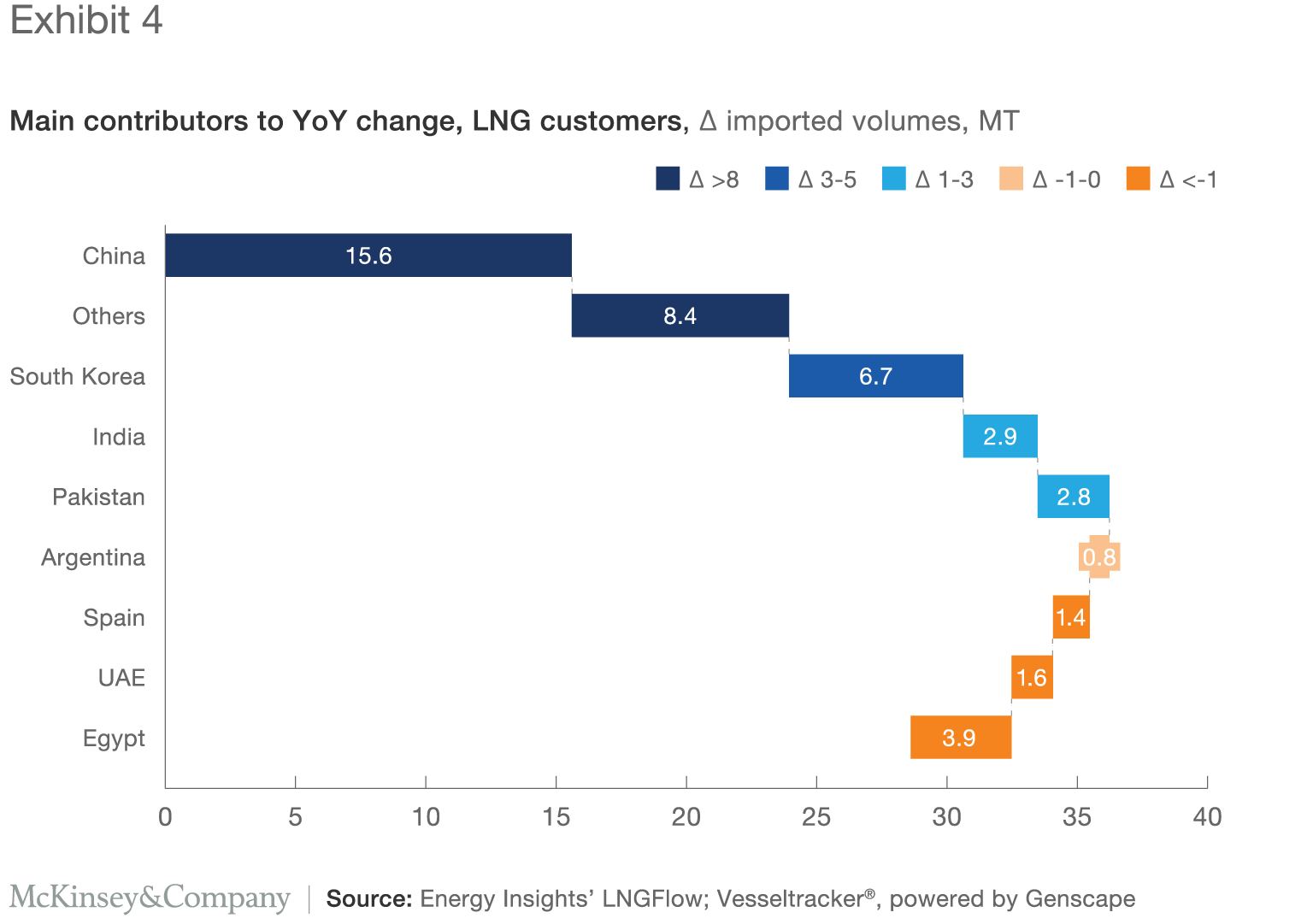

4. In 2018, gas consumption and in particular LNG imports continued to grow at pace in China. 2017 saw the country become the 2nd largest importer of LNG volumes after Japan. In 2018, China cemented its position as a critical importer with a 16-MT (41%) increase in LNG imports—reaching a total of 54 MT imported in 2018. Increases in LNG imports represented 50% of the additional volumes consumed in China and were complemented with additional domestic production (11 bcm) and additional piped imports (10 bcm).

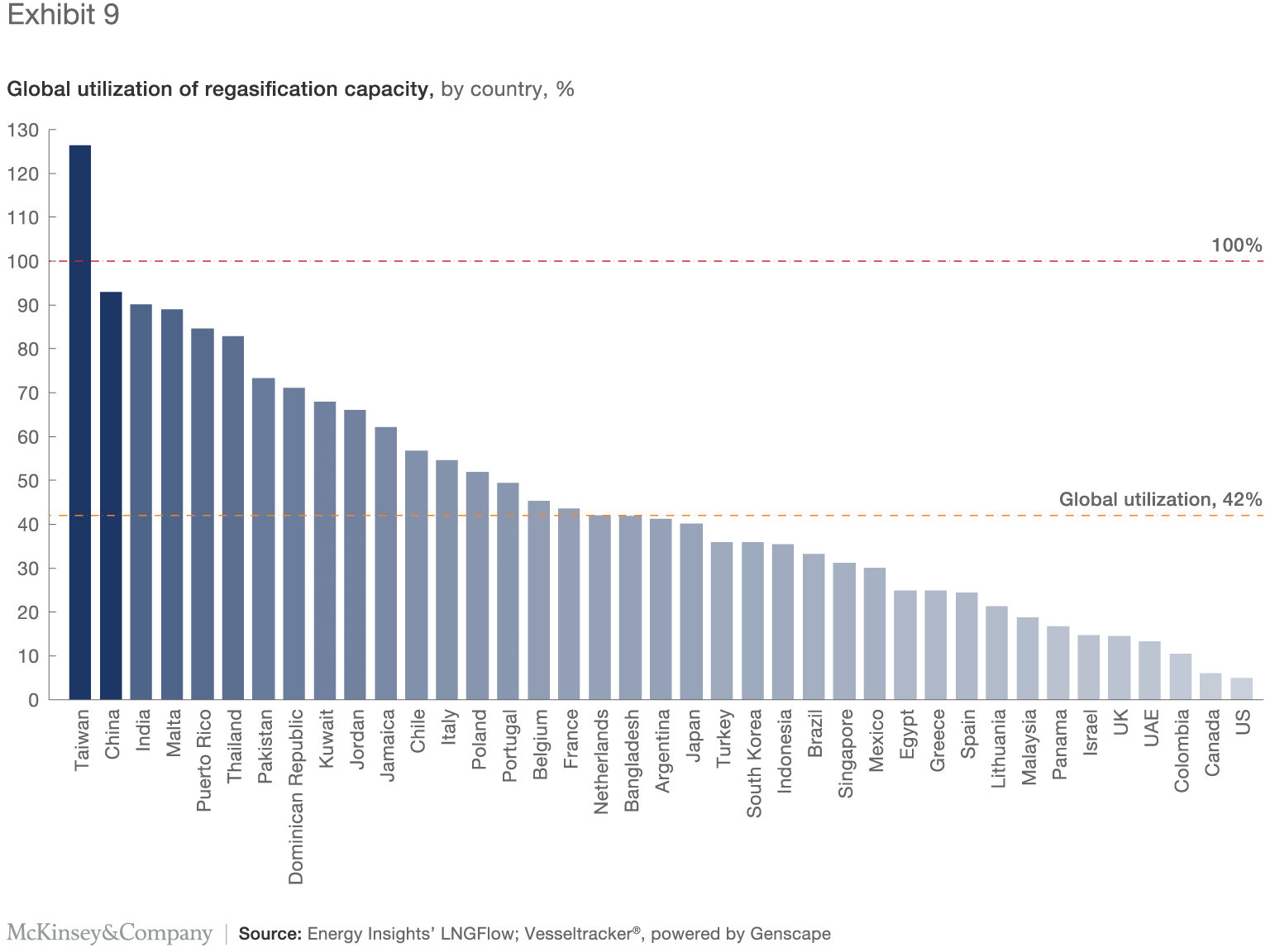

5. Due to the 41% growth in LNG import volumes, China’s regasification utilization increased to ~90%.

6. The South Asian peninsula—covering India, Pakistan, and Bangladesh—imported an additional 6.3 MT of LNG in 2018, with a growth of 2.9 MT (15%) in India, 2.7 MT (56%) in Pakistan, and first volumes being imported to Bangladesh (0.7 MT).

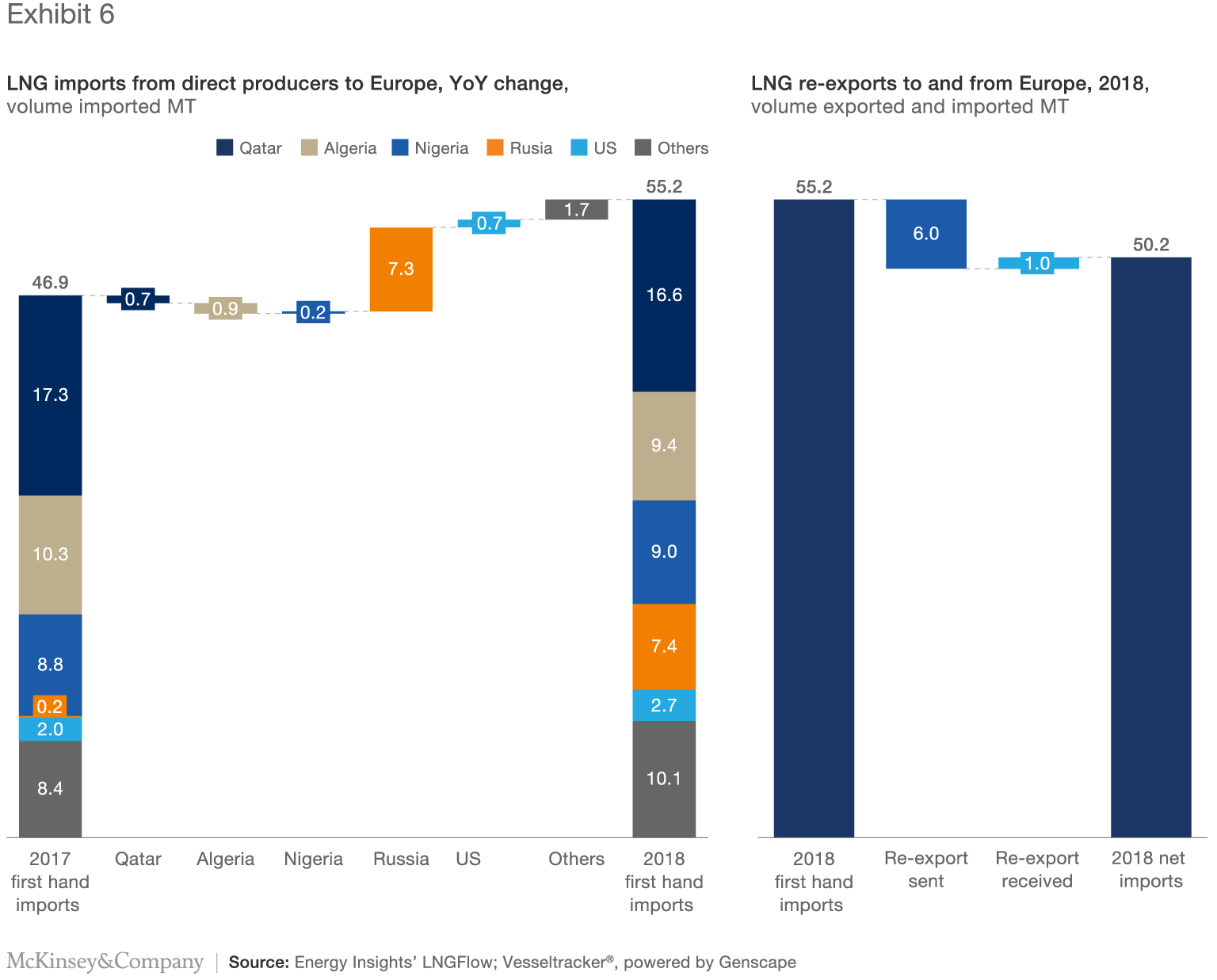

7. Russia’s Yamal LNG supplied the bulk of Europe’s additional 9 MT year-over-year imports. However, Europe also re-exported 6 MT, resulting in 4% net growth year-over-year. Of those re-exports, 57% were delivered to Asia, with China receiving nearly 1 MT. An additional 11% was redistributed within Europe itself.

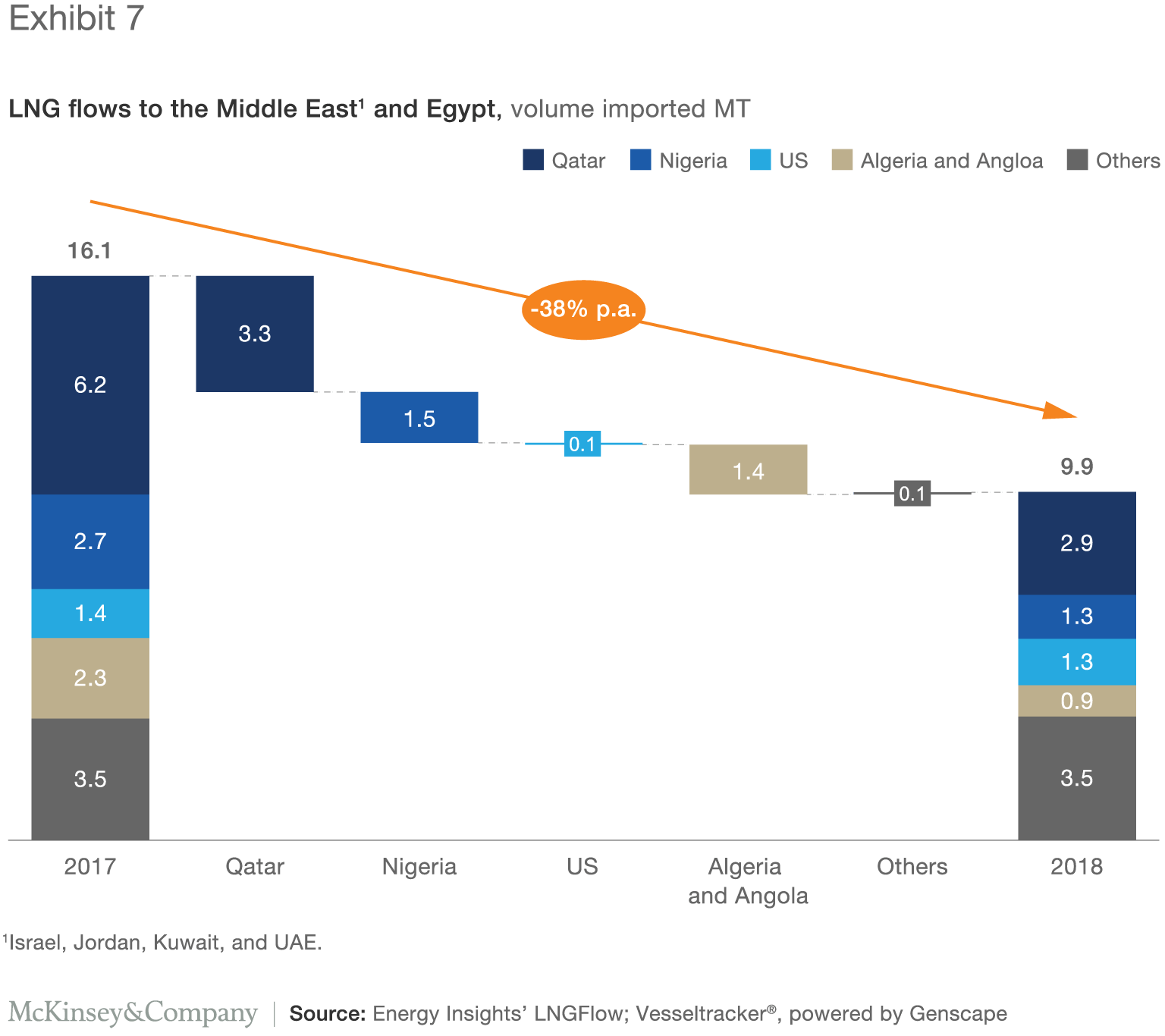

8. In sharp contrast, the Middle East and Egypt actually decreased their LNG imports by 6 MT between 2017 and 2018, with Qatari exports to the region reducing by 50% from 2017.

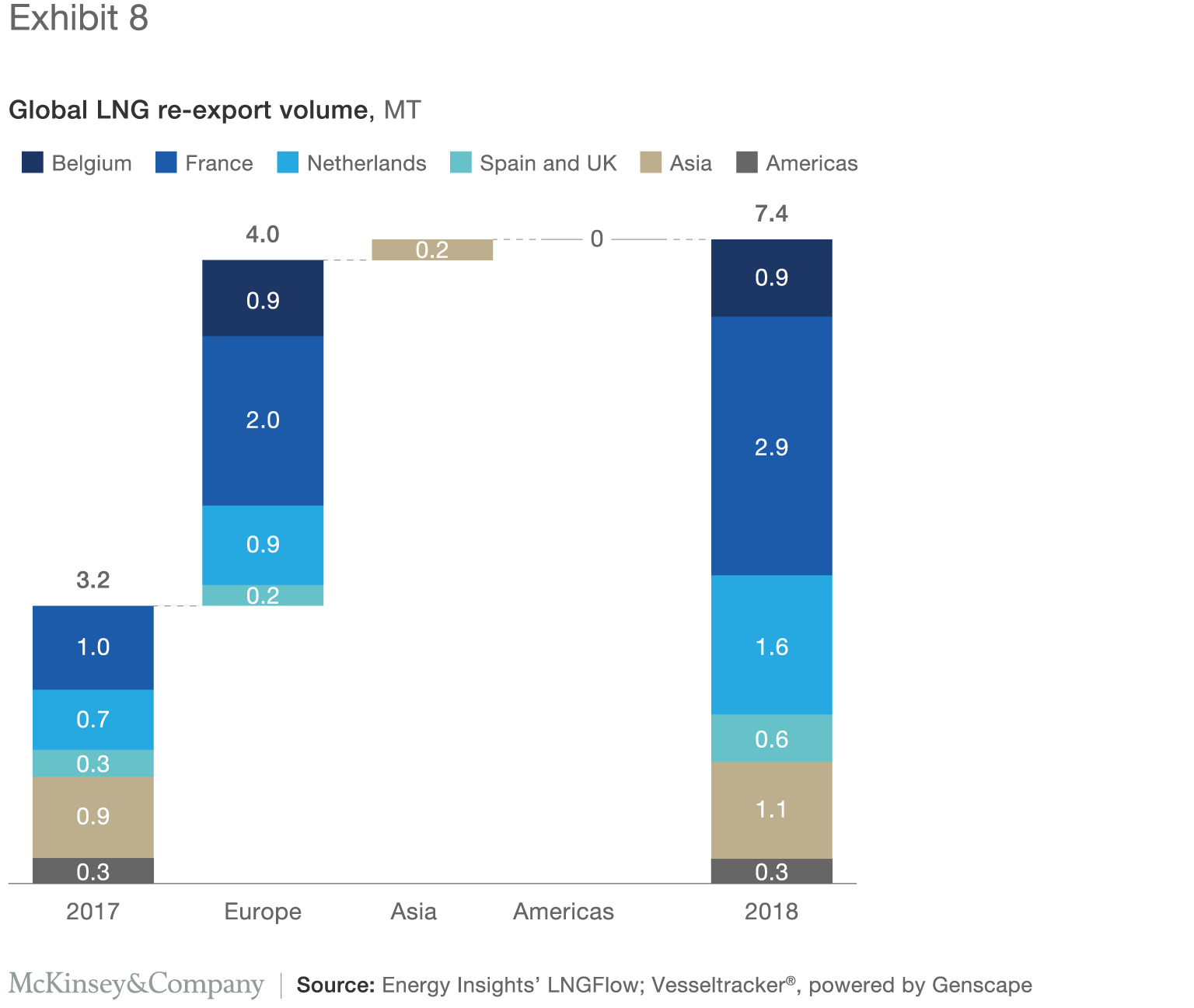

9. LNG re-exports were the domain of European players: France (2.9 MT), the Netherlands (1.6 MT), Belgium (0.9 MT), Spain (0.4 MT), and the UK (0.2 MT). In 2018, these countries contributed to 81% of the total re-exported volume.

10. Overall, regasification levels remained low in 2018 at ~42%, up from 40% in 2017.1 Aside from Bangladesh, Panama also started importing LNG volumes with its first cargoes received in June.

1 Only nameplate capacities of terminals which have received at least one cargo in 2018 have been considered

11. On the supply side, the situation is more mixed. While Qatar continues to be the top LNG exporter with 81.4 MT exported in 2018, the rapid expansion of liquefaction activities from other exporters is driving the gap in exported volumes between Qatar and others to shrink. Australia (70.9 MT), Malaysia (24.3 MT), and the US (22.1 MT) take up, respectively, the 2nd to 4th places in terms of volumes exported.

12. Furthermore, the ramp up in operations of liquefaction facilities contributed to the 20-MT year-over-year growth in the market, with the biggest increases observed in Russia (8.4 MT/74%), Australia (7.9 MT/14%), and the US (7.8 MT/55%).

13. Yamal played a big role in Europe’s LNG story, and its sent volumes almost doubled since August, when its second train started operating. Russia’s Yamal exports have primarily reached European terminals, although significant volumes were re-exported to other markets.

14. Australia’s capacity was extended with the Ichthys liquefaction plant (first cargo sent in October) and Prelude FLNG. The latter, despite receiving a commissioning cargo, still hasn’t started sending LNG. Another new FLNG capacity was Cameroon, which has been operating continuously since May.

15. The US has dramatically increased its sent volumes, jumping from the 6th biggest exporter in 2017 to 4th in 2018 (outpacing Indonesia and Nigeria). This was possible thanks to continuous upgrades made to Sabine Pass capacity, such as the opening of trains 3 and 4, as well as Cove Point’s production since March. The newly completed Corpus Christi, with its first cargo sent in December, is expected to add to the country’s overall LNG production capacity in 2019.

With these kind of shakeups in 2018, what can we expect to see in 2019? For starters, Yamal is one to watch, with its third LNG train recently made operational. Outside of that, liquefaction facilities in Australia and the US are continuing to expand, which may further close the gap between top exporter Qatar and other exporters.

By Gillian Boccara, Monika Stadnicka and Ewa Janiszewska-Kiewra

For more information, please visit our Energy Insights page.