Natural gas prices in North America (NA) hit record highs this year, quadrupling from pre-pandemic levels.1 These high prices have reverberations across the economy, impacting everything from home-heating bills to power prices and affordability. As NA heads into winter—the period of peak natural gas demand—it raises the question: What could impact natural gas prices over the next year?2

The natural gas market is complex and dynamic with ongoing changes and unpredictable elements in the mix. From mid-September to mid-October this year, the United States (US) has seen five consecutive injections of natural gas into storage of more than 100 billion cubic feet (bcf) per week. This is the longest streak of weekly injections of more than 100 bcf in the autumn for at least 12 years. As a result, US inventories are only 5 percent below the five-year average, resulting in downward pressure on natural gas prices.3

While there are several factors that could impact natural gas prices in the near term (such as the availability of coal for generation, economic growth, market sentiment, associated gas supply, and policy), few things may have a bigger, more sustained impact on prices than winter temperatures, producer investment and, to a lesser extent, liquified natural gas (LNG) exports.

Winter temperatures

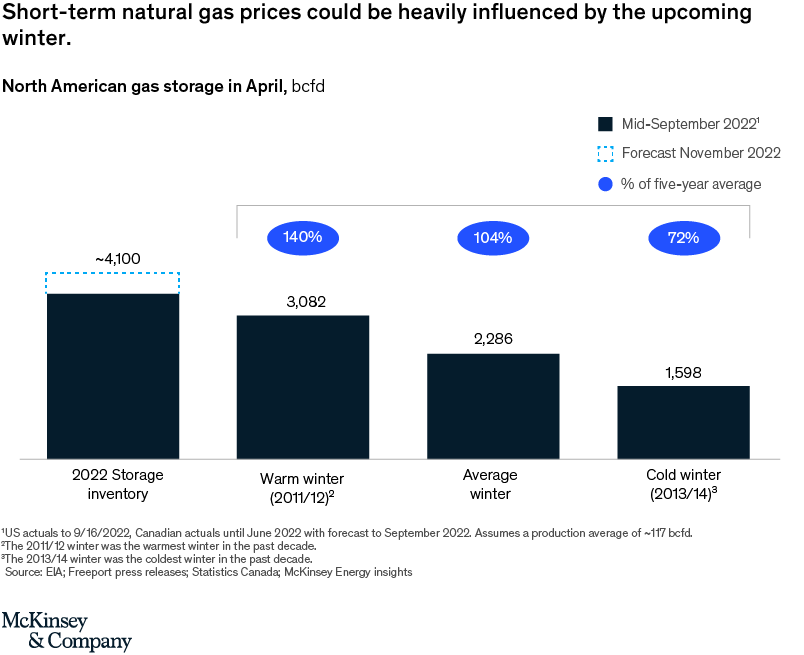

The severity of winter temperatures is key to determining near-term natural gas prices. Residential and commercial demand for natural gas can decrease by up to five bcf per day (bcfd) with a warm winter. Meanwhile, a cold winter can increase demand by up to five bcfd, in large part due to the natural gas required for space heating. In turn, prices are swayed (Exhibit 1).

According to the National Oceanic and Atmospheric Administration (NOAA), the upcoming winter in NA is generally expected to be milder than usual—potentially leading to lower natural gas demand than historical averages. This lower demand could put downward pressure on natural gas prices.

Producer behavior

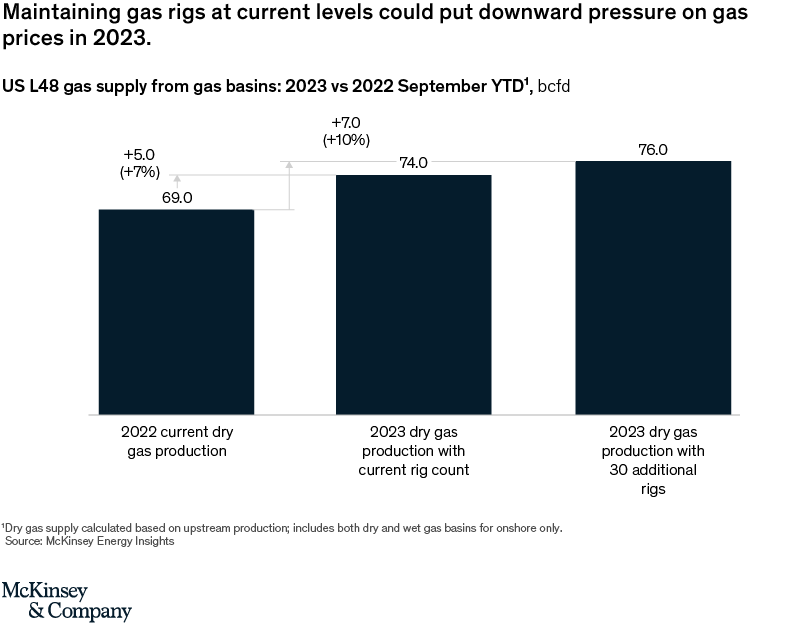

Producers are being more disciplined about deploying additional dry gas rigs to increase gas supply than they have been before. If current dry gas drilling is maintained, around five billion bcfd of additional production is expected in 2023. If 30 new dry gas rigs are introduced, it could result in an extra seven bcfd from current levels (Exhibit 2).

The addition of five to seven bcfd could put strong downward pressure on gas prices in the short term if demand stays stable. Given the currently high gas prices, it is unlikely that producers will reduce rig levels.4

LNG exports

LNG exports can affect the price of natural gas, to a lesser extent. Although there is an anticipated increase in demand for natural gas in Europe from sources other than Russia, the shift will likely not impact the NA natural gas market in 2023 more than current expectations. The infrastructure to export more LNG from NA to Europe does not exist and would take years to build.

Already, LNG exports from NA are largely operating at full capacity. However, the halt of operations at the Freeport LNG natural gas export facility in Texas this past June led to an export demand loss of around two bcfd—placing downward pressure on natural gas prices.5 While Freeport LNG is expected to resume operations in November 2022, there have already been delays, which could put additional downward pressure on NA natural gas prices.

***

The NA natural gas market is volatile with unpredictable elements, and the longer-term demand for LNG exports is expected to grow. But a warmer-than-usual winter, more disciplined producers, and a decrease in LNG export demand, could bring down natural gas prices in the short term.

About the author

Jamie Brick is a consultant in the Houston office.

Acknowledgements

The author would like to thank Sehrish Saud for her contribution to this article.

1 Henry Hub Natural Gas Spot Price, U.S. Energy Information Administration, October 19, 2022.

2 In this article, Henry Hub prices are considered as a proxy for overall North American natural gas prices. There are regional price hubs that may exhibit different pricing dynamics.

3 Weekly Natural Gas Storage Report, U.S. Energy Information Administration, October 20, 2022.

4 Higher oil prices could shift rigs from dry gas to tight oil basins. However, there are likely enough rigs in reserve to prevent this from happening. Additional oil drilling would also increase associated gas supply.

5 “Freeport LNG provides update on restart timeline for its liquefaction facility,” Freeport LNG, August 23, 2022.