Following an announcement by the White House several weeks earlier, the US Environmental Protection Agency (EPA) released a waiver on April 29 to allow the sale of E15 gasoline this summer.

In previous years, the sale of gasoline with 15% ethanol content (E15) was banned between June 1 and September 15 out of consideration of its contribution to smog accumulation during warmer summer months.

What effect would this have on US ethanol demand, and what does it mean for corn markets, from which ethanol is produced?

The E15 shift

Ethanol is one of the renewable fuels mandated under the US Renewable Fuel Standard (RFS) to be blended into transportation fuels to reduce greenhouse gas emissions. Typically seen in the E10 formulation (10% ethanol, 90% gasoline), the price of ethanol blended fuels is usually lower than gasoline, reflecting its lower fuel economy (especially at higher blends). Domestically, this biofuel is created primarily from corn, accounting for approximately 40% of annual US corn production.

Recent sharp increases in gasoline prices have spurred policy measures to reduce the cost burden on consumers—and on April 29, the US EPA announced a waiver to allow E15 gasoline to be sold in the summer. This is intended to combat high prices by increasing supply through the greater use of ethanol.

Impact on US ethanol

The availability of E15 sold at the pump is limited—approximately 2,300 out of 153,000 retail stations nationwide sold E15 in 2021. The limitation in availability is partly driven by compatibility requirements of certain equipment. Consumer awareness and concern over engine compatibility has also played a part in limiting the growth in market adoption.

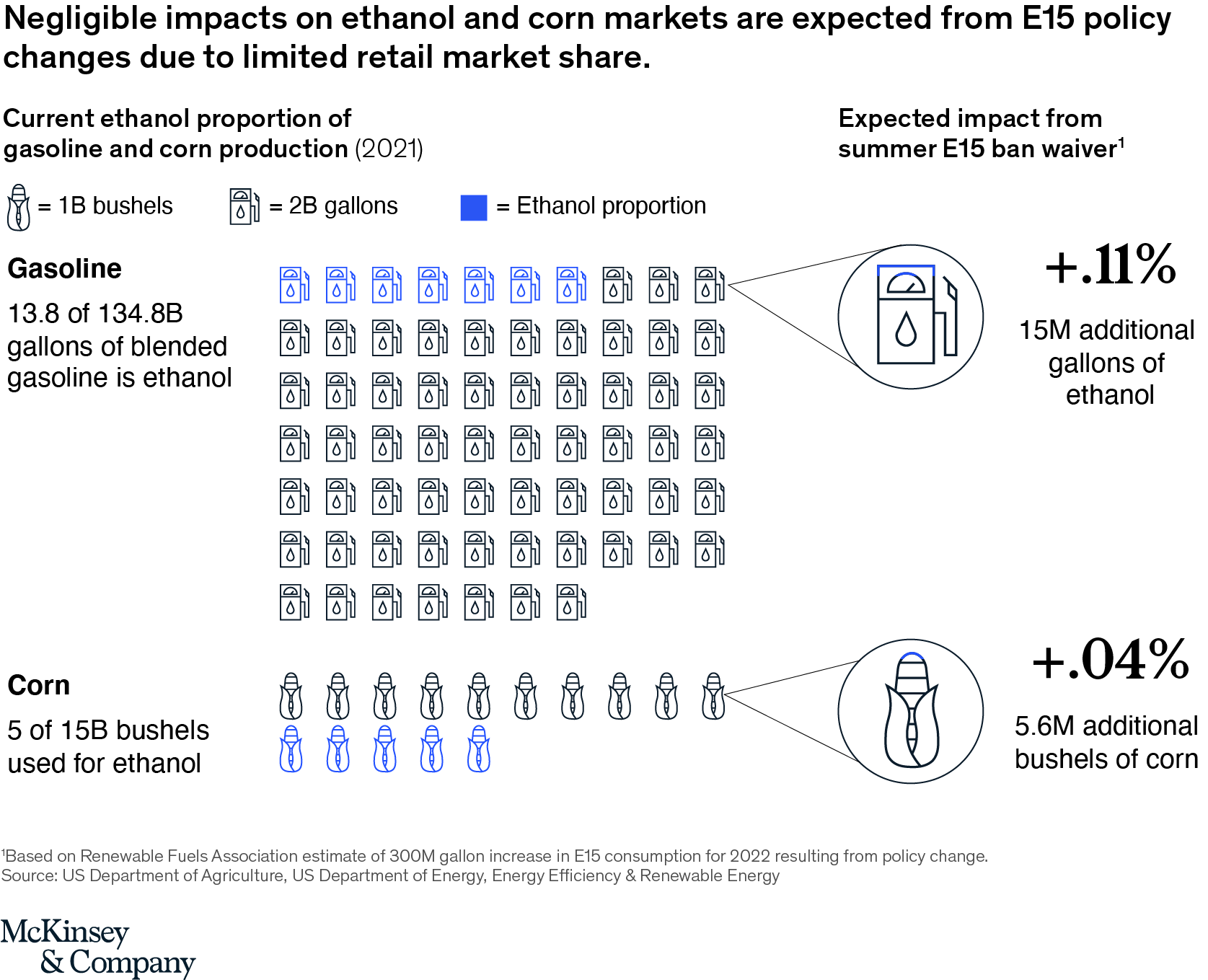

In 2021, E15 represented only 0.6% of all blended gasoline consumed—equating to 0.8 billion out of 134.8 billion gallons of blended gasoline sold. Assuming the barriers to higher adoption of E15 remain, the E15 ban waiver is expected to lead to a demand increase of 15 million additional gallons of ethanol. While this may sound significant, it is only 0.11% of the 13.8 billion gallons of ethanol used annually for gasoline.

Do we have enough corn?

In 2021, the US produced a total of 15 billion bushels of corn. The additional 15 million gallons of ethanol that will likely be consumed by E15 this summer equates to 5.6 million corn bushels, only a 0.04% increase.

Annual US corn production typically fluctuates by ~500 million bushels from year to year, ranging from 13.6 billion to 15.1 billion bushels since 2016. As a result, the additional demand created by E15 is unlikely to have a noticeable effect on supply.

More important are impacts driven by tightening of staple food crops from production and export disruptions in Ukraine as well as expected lower wheat yields in India, both of which may create material impacts on grain availability and food security in select countries.

What about E85?

The recent rise in gas prices has also led to a shift in demand for E85 gasoline, which sells at a discount to both E10 and E15 gas blends. E85, also called Flex Fuel, consists of 51% to 83% ethanol blended with gasoline. This percentage changes throughout the year to adjust to seasonal temperatures.

Since early March, demand for E85 has risen to 8,000 barrels per day, compared to the 2021 average of 6,000 barrels per day. If this shift were to persist for an entire year, the impact would be 25.7 million gallons of ethanol (0.17% of annual ethanol production) or 9.5 million bushels of corn (0.07% of annual corn production).

While there has been a shift in purchasing behavior, the impact is again negligible due to limited availability. Like E15, E85 has a small distribution network and is only available at 2.4% of gas stations (3,700 locations).

Synthesis

The summer waiver for E15 is not expected to have a significant impact on ethanol and corn markets, due to limitations on greater market adoption of E15. While we do not expect material impacts on supply in these markets, production disruptions of key staple crops in other regions should be closely monitored.