Stormy waters are nothing new for offshore drilling. Boom and bust cycles figure regularly in its long and volatile history. But the convergence of the global pandemic with the acceleration of the energy transition presents a unique challenge to an industry with unwieldy economics. Many drillers are considering restructuring their organizations or redeploying capital elsewhere, but another, more radical, option is worth considering: transforming offshore drilling into a more attractive business.

The industry has evolved to meet customers’ technical and operational demands while navigating the highs and lows of the oil price. However, its inherent volatility, together with its cyclicality, has led investors to question its potential for long-term value creation. While offshore drillers have delivered value for brief periods, they have destroyed value in excess of $85 billion since the 2007 peak, through speculative rig investments and a lack of commercial discipline (Exhibit 1).

This unattractive industry structure has been materially worsened by the events of 2020 and is likely to remain very challenged in the business-as usual-scenario. Today’s industry is plagued with chronic oversupply and poor economics in all categories. Leaders in offshore drilling have responded to the downturn by incrementally reducing costs, delaying capital expenditures, and canceling orders for new rigs. The resulting savings have allowed them to sustain positive operating cash flows for a while longer, but significant challenges remain (Exhibit 2).

As part of their cost-reduction efforts, many drillers are retiring non-competitive older assets (Exhibit 3). However, yet rig supply continues to exceed demand, pushing down rig rates. Further action is needed: many offshore drillers are approaching bankruptcy, their operating cash flows unable to support debt-ridden balance sheets or the traditional industry business model. New shareholders need to realize this is a zero-sum game: extinguishing debt allows companies to continue without addressing the structural oversupply of active rigs.

This time, recovery calls for a different approach

Some observers may claim that the downturn is merely part of the oil cycle, and will be resolved by underinvesting in new projects. But this view ignores the new forces that are transforming the dynamics of supply and demand for offshore oil.

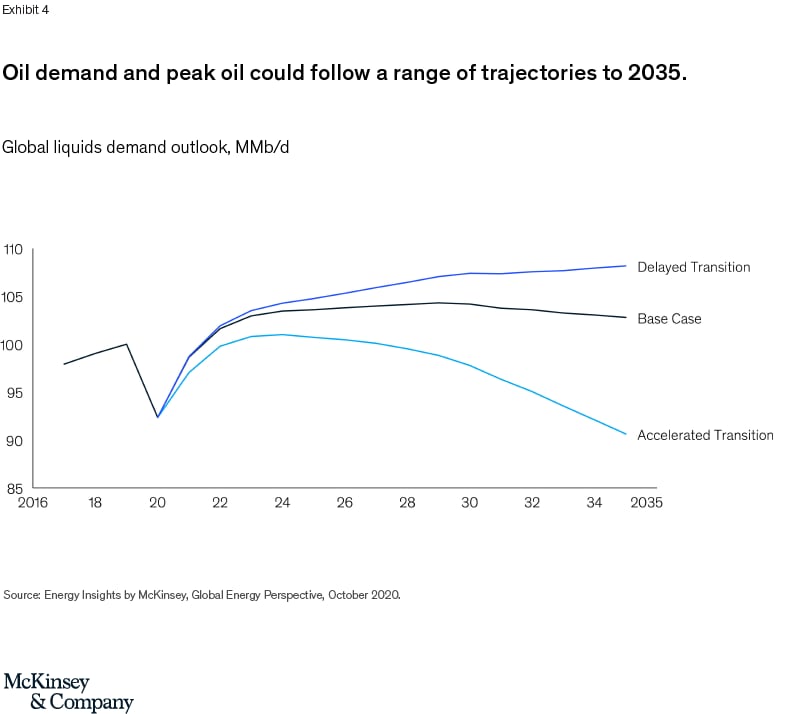

On the demand side, the transition to renewable energy sources and the impact of the COVID-19 pandemic have brought about a structural shift in oil demand (Exhibit 4). These shifts could potentially eliminate almost $130 billion in near-term capital spending. In addition, an estimated 6 to 7 MMb/d of yet to be sanctioned offshore projects between now and 2035 will be at risk if the energy transition accelerates.

On the supply side, offshore oil faces strong competition from other oil resources, particularly shale oil. As investors push for short-term cash generation, exploration and production (E&P) companies have seen opportunities to deploy capital into these shorter-cycle investments.

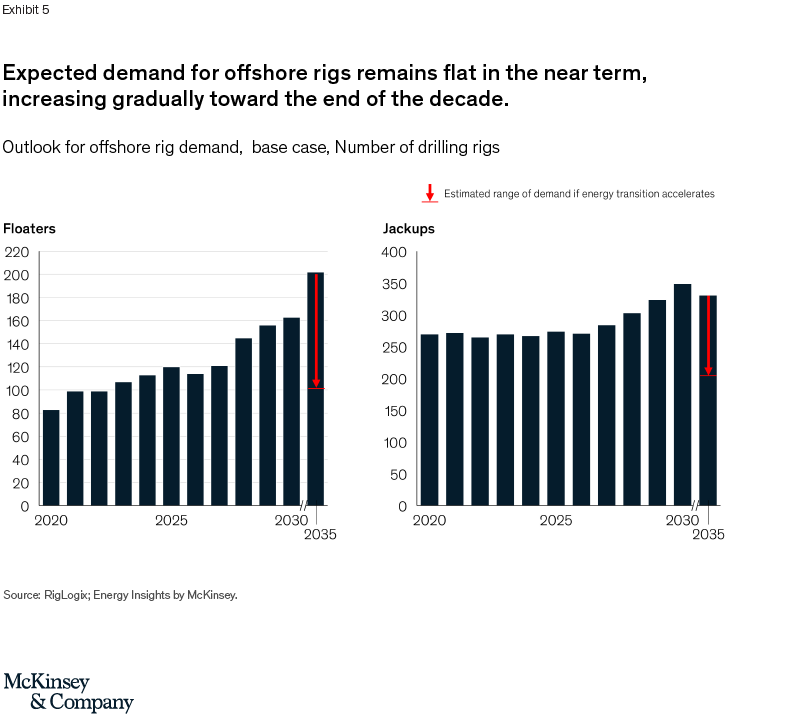

The outlook for oil demand and the resilience of shale oil shed light on the scale of the problem for offshore drillers. Under McKinsey’s base case scenario,1 floater demand remains flat for the next five years at around 100 rigs, before gradually rising through the middle of the decade to about 120 rigs. In the second half of the decade, demand grows to between 145 and 165 rigs.

For jackup rigs, on the other hand, flat demand continues at between 260 and 280 rigs to 2027, followed by an increase to about 340 rigs by 2030. However, in an accelerated energy transition, demand for both jackups and floaters could drop by about 30 to 50 percent by 2035 (Exhibit 5).

Historically, pricing stability has returned to the industry as marketed utilization passes 75 to 80 percent for floaters and 80 to 85 percent for jackups. If offshore drillers took no further action to reduce their active fleets and no more new builds entered the market, the utilization threshold required to achieve pricing stability would not materialize until 2028–29 for floaters, and probably not at all for jackups in the period to 2035 (Exhibit 6).

In short, offshore drilling has a structural oversupply of rigs for the foreseeable future. To recover from the downturn, it will need to change. This challenge stretches beyond drillers through to their upstream customers: in an Oil & Gas industry that has to fundamentally lower its cost structure to prosper, a damaged and weakened supply chain is not a long-term winning strategy.

A path to profitability

Neither restructuring nor incremental cost cutting will deliver the lasting strategic improvements required for a healthy industry. Re-establishing long-term profitability will require a radically different approach based on five imperatives: a step-change improvement in drillers’ cost position - much of this through technical innovation a transformation of their commercial model, a rationalization of their worldwide rig fleet, a diversification of their revenues, and a reframing of their portfolio.

1. Step-change improvement in cost position

Through several rounds of cost reductions, the offshore industry has cut onshore headcount, controlled offshore opex, shut down bases, and trimmed staff benefits. The only way to secure further savings is through a fundamental improvement in drillers’ operating model that reduces offshore and onshore operating expenditure and optimizes capital expenditure.

To reduce offshore operating costs, drillers could look at reducing the number of offshore staff, streamlining maintenance, and pursuing sourcing efficiencies:

Reducing offshore staff. Over the past 20 years, offshore crews have grown by 20–30 percent for comparable assets, and even more for technically complex assets. With customers’ cooperation, crew numbers could be reduced through cross-training, the sharing of specialist teams across rigs, and greater technology deployment. During the COVID travel restrictions, the industry showed it can operate for extended periods with fewer personnel offshore. It may be possible to reduce customer personnel and third parties on rigs by 50 percent or more. Winners will need to deploy value accretive technology and digitally enabled advanced operations aggressively.

Streamlining maintenance. Layers of maintenance requirements have been added over the years, particularly as the industry experimented with an asset-management mindset and worked to keep uptime at close to 100 percent. McKinsey analysis suggests that even for non-critical equipment, redundant maintenance tasks have inflated annual costs by 20 to 30 percent, at no obvious benefit to drillers. Meanwhile, maintenance systems still make considerable use of time-based tasks. Drillers could improve both performance and cost by redesigning maintenance activities around predictive data analytics and reliability approaches.

Pursuing sourcing efficiencies. Over the past few years, the emphasis on capturing sourcing synergies has begun to jeopardize the health of supply chains. However, drillers still have scope to address parts and servicing costs by reducing their reliance on OEMs for recurring maintenance and even critical equipment.

To reduce onshore operating costs, drillers could outsource transactional support functions to lower-cost countries. Some companies still use staff at high-cost locations to perform activities such as accounting month-end close, payroll, and accounts payable. They could cut costs by moving support activities to low-cost countries or delegating them to professional business-processing outsourcing companies. Complex engineering tasks could also be outsourced to specialist providers. By taking a clean-sheet approach to designing their organization, global footprint, and support centers, drillers could use technology to drastically reduce their overhead costs.

To optimize capital expenditure, drillers could push for quick payback and require that all capital expenditure pay back in the short to medium term. With a rig, that means within the current contract or prior to the next special survey stopping point. Drillers could also share the cost of enhancements with operators, accepting as-is drilling packages unless improving them is economically justified. They could also ask operators to fund upgrades in the spirit of partnership, since it is they who reap the benefits.

2. Commercial transformation

Offshore drillers and operators both suffer from a lack of positive operating cash flow. Their investment decisions typically take four to eight years to mature and generate positive cash flow, so they need partners that bring creative solutions to bear on long cash cycles. Drillers could consider developing new contracting models that align their need for cash with operators’ offshore investments. Operators will need to consider picking ‘basin winners’ and partnering long-term to increase utilization stability and create the environment for technology led improvements. The possibilities include:

Adopting a development-lifecycle mindset. Drillers could partner with operators to bring development wells online more quickly through parallel operations rather than sequential programs. Multiple rigs could conduct batch drilling and completions simultaneously to maximize the learning curve and minimize time to production.

Blending plug and abandonment (P&A) work into drilling programs. This work is often planned and executed by an entirely different department at the operator. To maximize utilization, drillers and operators could agree to conduct P&A work during scheduled idle rig times, capturing synergies by taking advantage of available rig days at adjusted terms.

Aligning compensation with operators’ cash flows. During well development, drillers could partner with operators to take a share of contract-drilling fees over time after production comes online. This would enable the cost of development projects to be spread and the operator’s peak invested capital to be reduced, potentially unlocking development opportunities that cannot be fully funded at present.

Other opportunities include applying an incentive model based on exploration outcomes, seeking partnership scale, and pushing for services such as transportation, boat logistics, cementing services, mud services, and casing running to be integrated into longer-term partnership arrangements.

3. Rationalization of rig supply

In an oversupplied market, drillers need to retire rigs that no longer serve a purpose in market rebalancing. They have two options: a business-as-usual path and a coordinated rationalization path.

The business-as-usual path. Here, the industry persists with its fragmented market and “wait and see” mindset. In line with historical rates of rig retirement, about 80 jackups and 30 floaters are retired in the next four to five years. Even if no new builds enter the market, utilization remains below 75 percent for floaters and 70 percent for jackups to 2028. Since companies operating older fleets have little to lose by keeping rigs in the market, they continue to compete on price. Meanwhile, established drillers with newer stacked assets burn cash for several more years by holding on to their rigs in hope the market will return and allow reactivation. This is not a path that gives the industry much chance of making a return on invested capital or attracting new capital.

A coordinated supply rationalization path. Under this scenario, industry leaders work to rationalize the offshore fleet, restore balance in the market, and drive economic performance. They retire or stack about 50 working or idle floaters and at least 130 jackups over the next four to five years—more than 60 percent more rigs than in the business-as-usual path, with many of them less than 10 years old. Provided no new builds come online, marketed utilization could return to 75 percent for floaters and 80 percent for jackups by 2024–25. Major established drillers and financial owners of speculatively built rigs would need a catalyst to make hard choices to retire assets as part of an overarching strategy of consolidation and market stability.

When assessing potential retirements, drilling contractors would need to prioritize rigs according to a set of objective criteria. First, they would rank each rig against competitors to assess its likely utilization in the medium and long term. Second, they would make a realistic assessment of the costs of reactivation, repair, and upgrading to determine how much total investment a stacked rig needs to return it to competitive work. Underestimating these costs destroys value.

Finally, to maintain disciplined decision criteria, drillers would set prudent economic and payback requirements, such as a cash return on reactivation at the end of the first contract or profitable returns by the next special survey project. If, having assessed these factors, drillers find conditions don’t support reactivation in the next five years, the cost of holding the rig in stack mode is likely to outweigh the opportunity to reactivate at a later date.

4. Revenue diversification

As the energy transition progresses, drillers need to weigh up options for, and the viability of, establishing alternative revenue streams to balance the risk of their drilling revenues. This could involve:

Repurposing idle fleets. Offshore drillers need to act now to determine where they could compete effectively in offshore wind or deep-sea mining, and whether they could modify idle rigs to participate in these sectors.

Establishing a position in an adjacent service business. Taking advantage of the skills associated with an asset-intensive service business, drillers could look for opportunities in adjacent or new areas such as logistics, supply chain, onshore engineering, procurement, and construction (EPC) projects, geothermal energy, and mining.

5. Re-framing the strategic portfolio

In this challenging environment, boards and executive teams will need to double down on strategy: business-as-usual and incremental improvements will not suffice. Whilst consolidation will not be a cure-all remedy, we are likely to see accelerating M&A activity and portfolio reconfigurations. As with their upstream customers, large complex fleet drilling companies will need to re-examine the value of integration and re-configure their organization, governance and operating models to ensure that they can win and lead on both cost and performance at the micro-segment level (rig class & region).

* * *

For the past five years, offshore drillers have ignored the fact that their business is broken. Now they urgently need to transform their operating and commercial models and reduce their global rig fleets. Restoring balance in the market calls for bold actions from industry leaders and a fundamental change in the industry structure. With the transition to renewable energy accelerating, this is a decisive moment for change. Operators can also play a part in ensuring the viability of the supply chain by working with drillers to establish win/win commercial models in offshore oil.

1 The base case scenario is based on the Global Liquids Supply Demand Model and Global Gas Intelligence Model developed by Energy Insights by McKinsey. It assumes that oil and gas demand recovers to 2019 levels by 2021–22 and that prices track the long-term average equilibrium Brent oil price of $50–60/bbl through to 2035.