With the completion of the US government’s banking “stress tests,” the rebound in first-quarter 2009 bank earnings, and the recent rise in the US stock market, it is fair to ask if we can now see a clear path out of the credit crisis. How close are we to the restoration of a strong and profitable banking and securities industry that is capable of providing the US economy with the credit it needs to grow?

The good news is that we have probably turned a corner in the credit securities crisis that last fall forced big financial institutions into collapse, nationalization, or extreme survival tactics. But the contours of a broader resolution of the crisis will remain fuzzy for some time to come. That’s because what many have been regarding as a single credit crisis is in reality the tale of two closely related but different crises, each with its own pace, duration, and demands on banks to rediscover operational discipline in a harsh economic and regulatory environment.

Twin crises

The first credit crisis was centered in the securities markets and initially manifested itself in the subprime and mortgage-backed securities markets. Because of the fair-value accounting that broker–dealers and investment companies use to mark assets to current market expectations, these firms began to suffer deep losses on mortgage-backed securities long before large volumes of loans started to default. This credit crisis started in mid-2007 and peaked in 2008, resulting in the demise of Bear Stearns, Lehman Brothers, and Merrill Lynch, and forcing Morgan Stanley and Goldman Sachs to become bank holding companies in order to survive. It also heaped huge losses on the securities arms of major US banks and forced government takeovers or mergers on AIG, Fannie Mae, Freddie Mac, National City, Wachovia, Washington Mutual, and others.

The good news is that we appear to be seeing the end of this credit securities crisis. That is in part due to the clarity provided by the stress test exercise and the ongoing commitment on the part of government not to allow a large-scale bank failure. The other credit crisis is a commercial-bank lending crisis. While this crisis also stemmed from bad residential mortgages, it involves a broader array of lending, including commercial real-estate loans, credit card loans, auto loans, and leveraged/high-yield loans, all of which are now going bad because of the economic downturn. The bulk of these loans are subject to hold-to-maturity accounting, which, in contrast to fair-market accounting, typically does not recognize losses until the loans default. The bad news is that this crisis is still in its early stages and may take two years or more to work through the credit losses from these loans.

Of course, all large financial institutions hold both kinds of credit assets on their books. Some of the largest broker–dealers hold 70 percent of their assets at fair value, while some regional banks hold up to 90 percent of their assets in hold-to-maturity accounts. For the banking and securities industry as a whole, about two-thirds of assets are subject to hold-to-maturity accounting.

It might seem odd that accounting methodologies can make such a big difference. At the end of the day, what counts is the net present value of the cash flows from each asset, but those are unknowable until after a debt is repaid. Fair-value accounting, based on mark-to-market principles, immediately discounts assets when the expectation of a default arises and ability to trade the assets declines. Fair-value therefore makes the holder of the assets look worse, sooner. Hold-to-maturity accounting works in reverse and makes the holder look better for a longer time.

First-quarter 2009 earnings

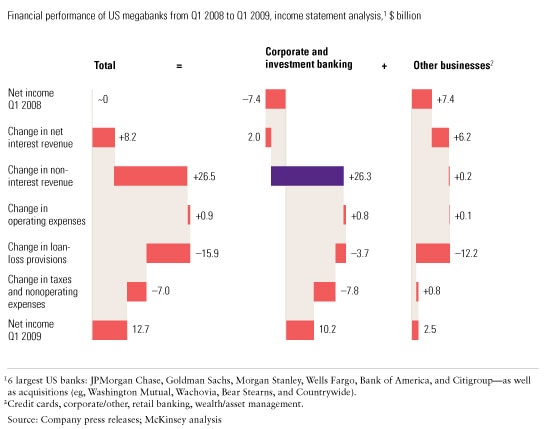

Many of the largest banks reported a return to profitability in the first quarter of 2009. The comfort this provided to markets is not necessarily misplaced. Without the “corporate/other” category (which includes many one-time accounting adjustments), first-quarter 2009 operating earnings for the six largest banks were $12.7 billion, compared with breakeven in the first quarter of 2008.

An analysis of these results shows that quarterly noninterest revenue for corporate- and investment-banking activities (that is, largely broker–dealer operations) increased by a surprisingly large $26.3 billion from the prior year (Exhibit 1). Fair-value accounting losses depressed 2008 results but in 2009 were replaced by fair-value gains. Large additional trading profits were made possible by arbitrage and other trading opportunities that became available as market conditions improved.

A return to profitability

While the worst may be over for the broker–dealer sector, first-quarter 2009 results tell a different story for commercial-banking activities at the same major banks. These banks took $38 billion in loan-loss provisions in the first quarter, $16 billion more than in the 2008 period. Most of this increase—$12 billion—was from retail-banking and credit card credits. In other words, the pace of defaults on these credits is rising.

This merits concern because loan provisioning under hold-to-maturity accounting is a lagging indicator of future loan losses. Under hold-to-maturity accounting, loan losses are delayed even when they are highly probable, because loan-loss provisioning doesn’t take place until the loans actually default. And since many of these loans have terms and conditions that allow the borrower to pay interest out of a line of credit, such loans won’t default until the line of credit is exhausted. Hence, eventual losses may grow as the lines are drawn down, but the timing of the losses is delayed. When loan-loss provisions start rising rapidly, it is likely that more losses lie ahead.

Loan losses to come

While 2008 was the year for taking losses on broker–dealers, this year and next will be the years for taking losses on assets subject to hold-to-maturity accounting. These are the losses that show up in stress tests, in which regulators make assumptions about how the economy will perform and calculate the resulting loan losses under various economic outcomes. For example, credit card losses are highly correlated with unemployment. By projecting unemployment rising to a certain level, stress testing can then project the attendant credit losses.

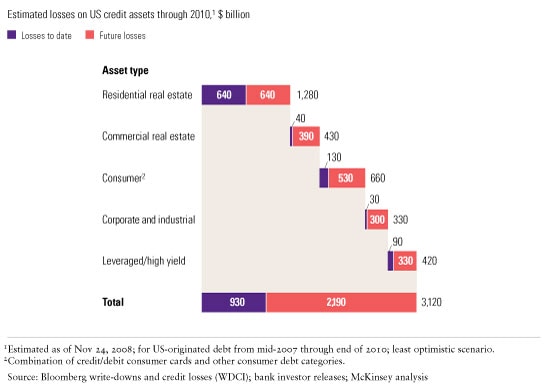

McKinsey research estimates that total credit losses on US-originated debt from mid-2007 through the end of 2010 will probably be in the range of $2.5 trillion to $3 trillion, given the severity of the current recession (Exhibit 2). Some $1 trillion of these losses has already been realized. Since US banks hold about half of US-originated debt, the US banking and securities industry will incur about $750 billion to $1 trillion of the remaining $1.5 trillion to $2 trillion of projected losses on this debt, which includes residential mortgages, commercial mortgages, credit card losses, and high-yield/leveraged debt. These numbers are in the same range as those of the US government, which calculated a $600 billion high-end estimate of credit losses for the 19 largest institutions.

A breakout of credit losses

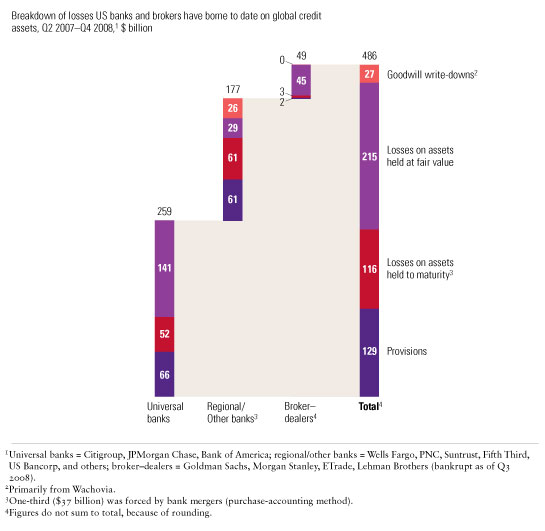

Since the middle of 2007, the US banking and securities industry has absorbed some $490 billion of losses, or $80 billion per quarter (Exhibit 3). If the industry incurs additional losses of $1 trillion in 2009 and 2010, the losses will be about $125 billion a quarter. As noted, however, these losses will be concentrated in commercial-banking loans. Importantly, many of these losses will be concentrated in the banks that the stress tests revealed to be undercapitalized.

Already gone

The relative capital strength of any given institution, using generally accepted accounting principles (GAAP), is highly related to its mix of assets and in particular to the mix of assets subject to fair-value or hold-to-maturity accounting. Therefore, it is not surprising that most of the well-capitalized institutions, as determined by the stress tests, are either firms with large broker–dealers (that is, Goldman Sachs, Morgan Stanley, and JPMorgan Chase) or large custodians/asset managers (that is, Bank of New York Mellon and State Street) that took major losses in 2008. Nor is it surprising that most of the “undercapitalized” banks are institutions whose portfolios are largely composed of hold-to-maturity assets with losses still to come.

Grading the stress tests

Stress testing may have set the stage for restoring the health of individual institutions because it has provided the financial markets with information on the quality of each individual institution’s loan portfolio. The more transparent the information on the composition of loan portfolios is, the better analysts will be able to make their own estimates of losses on hold-to-maturity loans. Moving in this direction is essential to restoring confidence in the quality of bank balance sheets and to providing discipline against unwise risk taking going forward.

The tests also marked a turning point because they provided much greater clarity regarding how the US government will handle troubled institutions in the future. The US government has demonstrated to the financial markets’ satisfaction that it has both the resources and the will necessary to ensure that there will be no more large bank failures. The government is clearly prepared to use whatever combination of funding support, guarantees, and capital injections are required to ensure that any future resolution of troubled financial institutions will be orderly.

Restoring earnings strength

While the stress tests have focused on capital adequacy, the only real way for an institution to become strong enough to stand on its own feet is through its ability to earn profits. Banks and securities firms with real earnings power will be able to raise capital both from retained earnings and by issuing new securities.

The challenge for many adequately capitalized banks is that they will find it difficult to generate enough income to cover loan-loss provisions over the next two years. Moreover, it is unclear how long net interest margins will hold up. Since 2006, net interest margins have actually increased for the stress-tested banks, despite rising nonaccruals (that is, when a loan defaults and a loan provision is made, it no longer accrues interest). For these banks, net interest margin has actually increased from 2.1 percent to 3.0 percent, which represents $70 billion of income annually (Exhibit 4). Much of this increase is due to rapid declines in funding costs thanks to the US Federal Reserve, which has lowered the rates banks pay faster than the interest on their loan and securities books. As more loans go on nonaccrual and as loans roll over, net interest margin may come under pressure, even if the Federal Reserve keeps rates low.

Increasing net interest margins

To meet this earnings challenge, well-capitalized and adequately capitalized banks must play both defense and offense. In terms of defense, investing in building collection and workout skills is essential. Based on our experience, the difference between common and best-practice performance can easily be 5 percent to 15 percent of losses, depending on an institution’s starting point.

It is also essential for banks and securities firms to begin reducing operating expenses more programmatically. Although one might assume that banks and securities firms have been reducing costs in response to hard times, the 19 stress-tested institutions have actually increased annual operating expenses by 32 percent since 2006 ($90 billion annually, from 2.8 percent of assets to 3.3 percent). Many banks need to target reductions in noninterest expenses of 20 percent or more from 2008 levels.

Banks with broker–dealers should have an abundance of opportunities as the markets continue to thaw. The pent-up demand for credit securities issuance, acquisitions, and spin-offs is considerable. Moreover, trading opportunities should be numerous for strong counterparties.

Challenges ahead

Even the strongest of the major US banks face a challenging environment for the foreseeable future. Not only has the economic shock thrown financial markets and industry structures into flux, but the process of saving the banking and securities industry has transformed the nation’s social contract with the industry. The entire industry is now dependent on government support of all kinds, ranging from low-cost funding (courtesy of the Federal Reserve), to debt guarantees, asset guarantees, and capital injections.

There is no clear path to restoring the industry to independence from the US government. Major changes in regulation are coming, and the industry is going to be subject to more government involvement and oversight than it would like for a long, long time. Against that backdrop, stress testing has removed much of the generalized fear that painted all institutions with the same brush. It has also removed the uncertainty related to how the US government is going to treat individual institutions. But it will remain for the industry’s leaders to put in place the operational efficiencies and discipline that may determine when—and how—the credit crisis is finally resolved.