China's banking sector has made phenomenal strides. More than 100 banks act as go-betweens for savers and borrowers in every corner of this huge country, up from just a handful when economic liberalization began, in 1978. Last year foreign banks took stakes worth $18 billion in China's biggest banks—moves reflecting the extent of the sector's maturation as well as optimism about its prospects. Rapid growth hasn't been painless, however. Since the end of 2001 the government has been digging banks out of a mountain of nonperforming loans, which will ultimately cost Chinese taxpayers an estimated $215 billion, and possibly far more.

Research by the McKinsey Global Institute comparing the performance of China's banking system with international benchmarks shows that although the country's banks have come a long way, they are not yet out of the woods.1 Chinese banks still lend too much of their money to underproductive state-owned enterprises (SOEs)—a problem that leaves them particularly vulnerable to changes in the economic climate and hinders the country from achieving its stated regulatory goals. China's government can certainly afford to bail out the banking sector again should the need arise. But it would be far better for the economy, and especially for the taxpayers (who foot the bill for bank bailouts), if regulators could accelerate the pace of reforms that encourage banks to lend more productively.

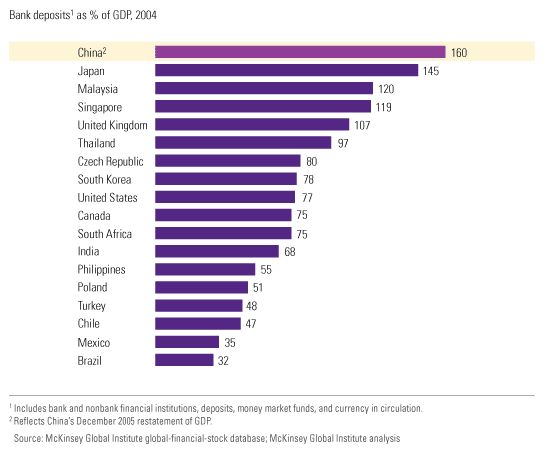

Bigger . . .

A strong banking sector is vital to China's economy because banks dominate the financial system as a whole: at the end of 2004, they accounted for 72 percent of the country's financial stock, far higher than the 43 percent in India, 33 percent in South Korea, and just 19 percent in the United States. Last year, more than 95 percent of new corporate funding for Chinese companies came from banks—a proportion much higher than that in other major Asian economies. China's banking sector is huge in absolute terms as well: in March 2006 bank deposits stood at more than $3.5 trillion, roughly half from households and half from corporations. At the end of 2004, deposits equaled 160 percent of GDP.

. . . but not better

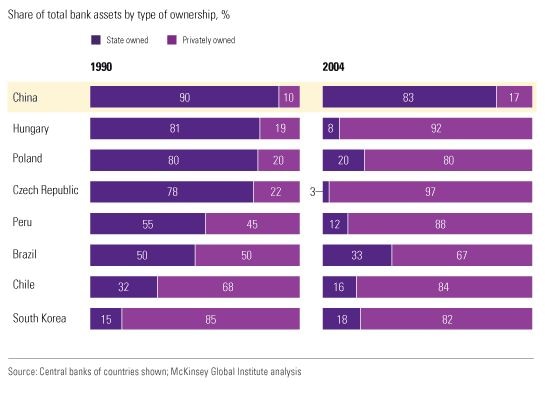

Many Chinese banks, despite their size and high levels of lending, struggle to price loans according to the risks individual borrowers pose. Banks still lack this basic commercial skill largely because they have little incentive to develop it. In contrast to other countries where market liberalization has taken hold, in China banks remain firmly in the government's hands, and precious few have a strong commercial mind-set. Although private investors take part in the management of a handful of major banks in China, none are fully privately owned. Regulators hope to change this state of affairs, and today many banks—including the Bank of China, the Bank of Communications, the China Construction Bank, and the Industrial and Commercial Bank of China—have foreign strategic investors. Such partnerships bring not only capital but also, and more important, valuable skills in everything from risk management and IT to general management. Nevertheless, rolling out the profound changes that are necessary across thousands of far-flung bank branches will take time. Without majority control, it is unclear how much influence foreign partners can have.

The big four

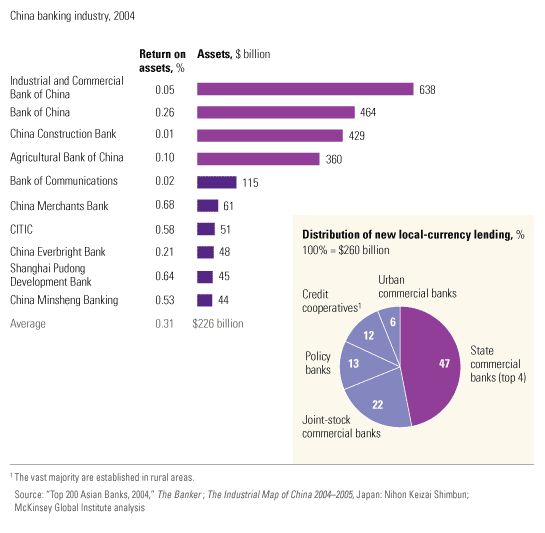

Four large banks dominate China's banking sector, and it is these that regulators are trying most strenuously to raise to world-class standards through broader ownership (via strategic foreign investments and IPOs) and improved governance. In addition, the country has roughly 120 smaller city and regional banks, and the best of them also have foreign investors. Some of the smaller banks are rapidly gaining market share—indeed, in 2004, for the first time, the proportion of new loans made by the big four dipped below 50 percent. While this may sound like the stirrings of healthy competition at work, some smaller banks appear to have worse lending skills than the big four do and are even harder for regulators to monitor and control. These small institutions often lend at rock-bottom rates to increase their market share. Should economic growth falter and loan defaults rise, this strategy could land them in trouble. To make competition effective, higher-performing banks should be allowed to purchase them in the years to come, and the industry should consolidate. The recent and forthcoming IPOs of the largest banks could facilitate this process.

Misguided lending

Unlike institutions elsewhere, China's banks lend primarily to companies rather than consumers. Although growing rapidly, consumer lending remains underdeveloped: mortgages, for example, equal just 11 percent of the country's GDP, and total consumer credit in China equals just 13 percent of GDP, compared with 38 percent in South Korea and 88 percent in Singapore. Within the corporate sector, banks lend mostly to large SOEs, even though they are, on average, less productive than private small and midsize enterprises, which, together with foreign companies, now account for over half of China's GDP but only 27 percent of all outstanding loans.

From a banker's perspective, this lending bias is rational. Banks have difficulty judging the health and performance of private-sector and smaller companies because financial reporting is generally poor and credit bureaus and independent rating agencies are scarce. Moreover, bankers assume that the loans they make to SOEs are backed by Beijing. That perception is hard to shake given the $105 billion it has spent so far to recapitalize banks and the $300 billion worth of nonperforming loans that have been transferred to state-owned asset-management companies.

Poor risk assessment

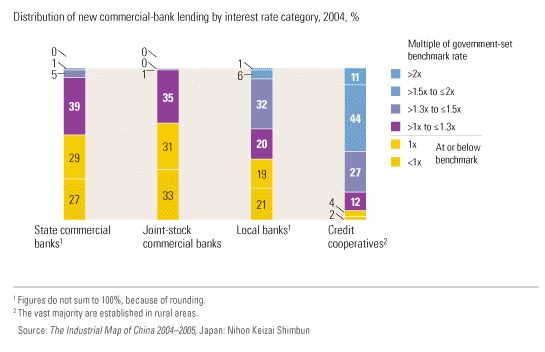

The good news is that the government has now partially deregulated Chinese interest rates by removing the interest rate ceiling on loans and the floor on deposits. But the largest banks still price most of their loans at, or slightly below, the government-set benchmark rate because they lack loan-pricing skills. With better information on borrowers, banks might appraise the real risks of their customers more proficiently and make more loans, at varying rates, to the private sector. These moves would be good for the banks' profits and much better for the economy as a whole, since investment could be targeted to more productive uses. But to align the banks' incentives with China's economic interests, regulators must make it clear that bailouts for bad loans are a thing of the past.

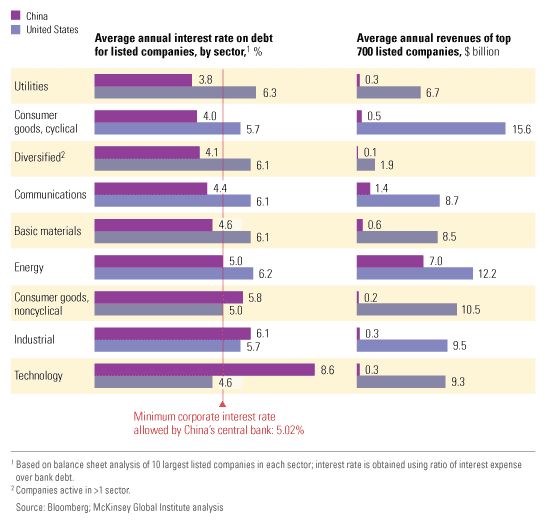

Cheap money

Meanwhile, the banks' current approach to pricing loans makes the cost of debt for Chinese companies abnormally low. They not only pay less for loans than do US companies—despite being much smaller and operating in a far riskier environment—but also, in some sectors, pay average financing costs even lower than the minimum levels prescribed by China's central bank. Cheap loans encourage overborrowing, which leads to excess capacity and inefficient investments in many sectors. China's regulators are trying to discourage excessive lending by raising the benchmark interest rate and, in certain cases, telling banks to reduce the level of loans to overheated industries. But this approach may actually have the opposite effect, since regulated deposit rates haven't been raised. Banks thus have higher margins, which may tempt them to lend even more.

Loans gone wrong

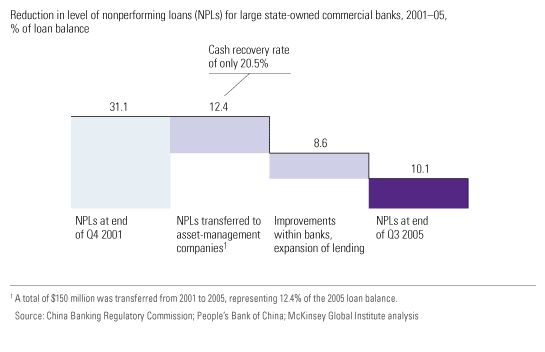

Despite significant progress in recent years, the problem of China's nonperforming loans probably hasn't run its course. From 2001 to 2005 the state bought, at face value, most of those held by the largest banks and transferred them to state-owned asset-management companies, which are working them out slowly. Such transfers, which accounted for 60 percent of the reduction in the level of nonperforming loans as a percentage of the large commercial banks' total assets, successfully eliminated the risk of a systemic banking failure by moving existing nonperforming loans off the banks' books. In most cases, however, Chinese banks still don't have enough information on borrowers, or strong enough lending skills, to prevent more bad loans from accruing. Few banks even reward their loan officers for avoiding nonperforming loans. Although many banks are trying hard to improve in these areas, the task is huge, and the ratio of bad loans to good ones could rise again, particularly if economic growth slows.

Deposits high, returns low

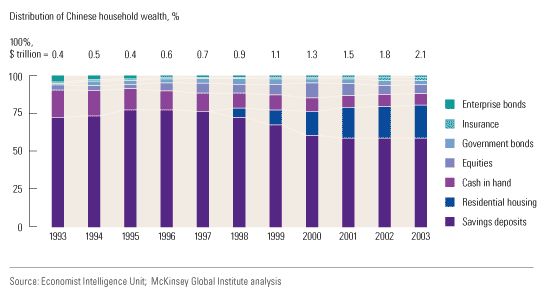

At first blush, China's banks look more secure on the deposit side. Bank liquidity is high because households keep a large portion of their assets in savings accounts, and the yields on bank deposits have to date been unusually low because the government regulates deposit rates. Other financial assets available to households have also offered very low returns (with higher volatility), which helps to explain why the Chinese park so much money in low-yielding deposit accounts. Over the past ten years, returns on household financial assets after inflation have come to only 0.5 percent a year in China, compared with 1.8 percent in South Korea and 3.1 percent in the United States. Things could change as other financial assets and investment options (such as real estate and equities) become more attractive, which would make bank deposits vulnerable. In recent years, for instance, more people have begun to invest in real estate, and this trend has reduced the share of household assets kept in savings accounts. Bank deposits represented 59 percent of household wealth in 2003, down from 76 percent in 1997—though the absolute value of deposits continued to grow over that period.

Concentrated wealth

Chinese banks are particularly vulnerable to the possibility that affluent customers might switch out of deposits. China's wealth is highly concentrated—some 2 percent of the country's households own 60 percent of it—and banks rely heavily on the wealthy few for their profits. Indeed, when measured by the Gini coefficient, a metric of income distribution, the gap between rich and poor is larger in China than in the United States. Bank deposits could dwindle when affluent customers seek a better return, as recent surges in the equity markets and real-estate values around the country suggest they are already doing. Wealthy Chinese can to some extent look abroad for investments. In April 2006 China's authorities announced that individuals may invest up to $20,000 a year in foreign currency to buy overseas bonds, up from the previous limit of $8,000. However, many investors may prefer to hang on to their money in the hope that the currency will appreciate further.

The cost of inefficiency

The banking system's inefficiency has a huge impact on China's economy. The country's banks incur higher costs than do banks in Chile, Malaysia, Singapore, South Korea, or the United States, where the average spread between loans and deposits is 3.1 percent. In China, after the money spent on capital injections into the banks has been included, the margin is 4.3 percent, which costs bank customers an extra $25 billion a year. Even more expensive is the country's poor capital allocation, which sustains inefficient companies at the expense of more productive ones. Addressing this shortcoming would raise China's GDP by $259 billion, or 13 percent.2

Of course, the reforms necessary to achieve such gains will require a drastic change in mind-set while the essential purpose of the financial system evolves from propping up SOEs and ensuring employment to meeting the needs of a modern competitive economy. Nevertheless, China's enormous economic progress over the past 25 years offers the hope that a similar transformation of its financial system is also on the way.