The COVID-19 pandemic continues to expand, and the United States has now surpassed all other countries by number of cases. Few anticipated the pace at which the US economy would shut down and physical distancing would become so pervasive. Like all industries, insurance has been materially affected: since the onset of the pandemic, it has lost $760 billion globally in market capitalization, the third highest among all industries.

Across the US insurance industry, the impact will be uneven. Life and annuity carriers will be the hardest hit because of lower interest rates. Some segments will be affected by rising mortality rates. Commercial property and casualty (P&C) businesses will shrink because of the economic contraction and rising unemployment. Some P&C lines will experience spikes in losses from business interruption, directors and officers, event cancellation, medical malpractice, and trade credit, among others.

At first glance, the impact on US personal auto insurance appears to be more muted. The segment’s growth and performance have been mostly impervious to recessions over the past 20 years. However, the pandemic could precipitate structural changes in the market. For instance, mobility trends may pause if more people choose to own a car and drive everywhere because they think ride sharing and public transportation are too risky during a pandemic. Historically low oil prices will make driving much more affordable. And, while less driving during the shutdown period will result in a lower frequency of accidents overall, cities may see higher frequencies, as less congestion could lead to increased speeding.

There remains much uncertainty about the full impact of COVID-19. In this article, we explore four scenarios (including a “black swan” worst-case scenario) based on several unknowns: What if the economic impact is worse than anticipated, caused by longer lockdowns or more difficulty restarting the economy? What if trauma associated with the pandemic leads to fundamental behavioral changes? There is a chance that personal auto insurance will experience the same volatility seen in the 1970s and 1980s, when nonstandard risk segments, assigned risk pools, and uninsured motorist surcharges threatened the industry’s viability. Indeed, in 1985, one of the leading auto insurers nationally was a state underwriting plan with a 140 percent loss ratio. Could the current pandemic lead to similar levels of strain on the industry? The answers will have implications for how insurers move forward.

How COVID-19 could change auto insurance profitability

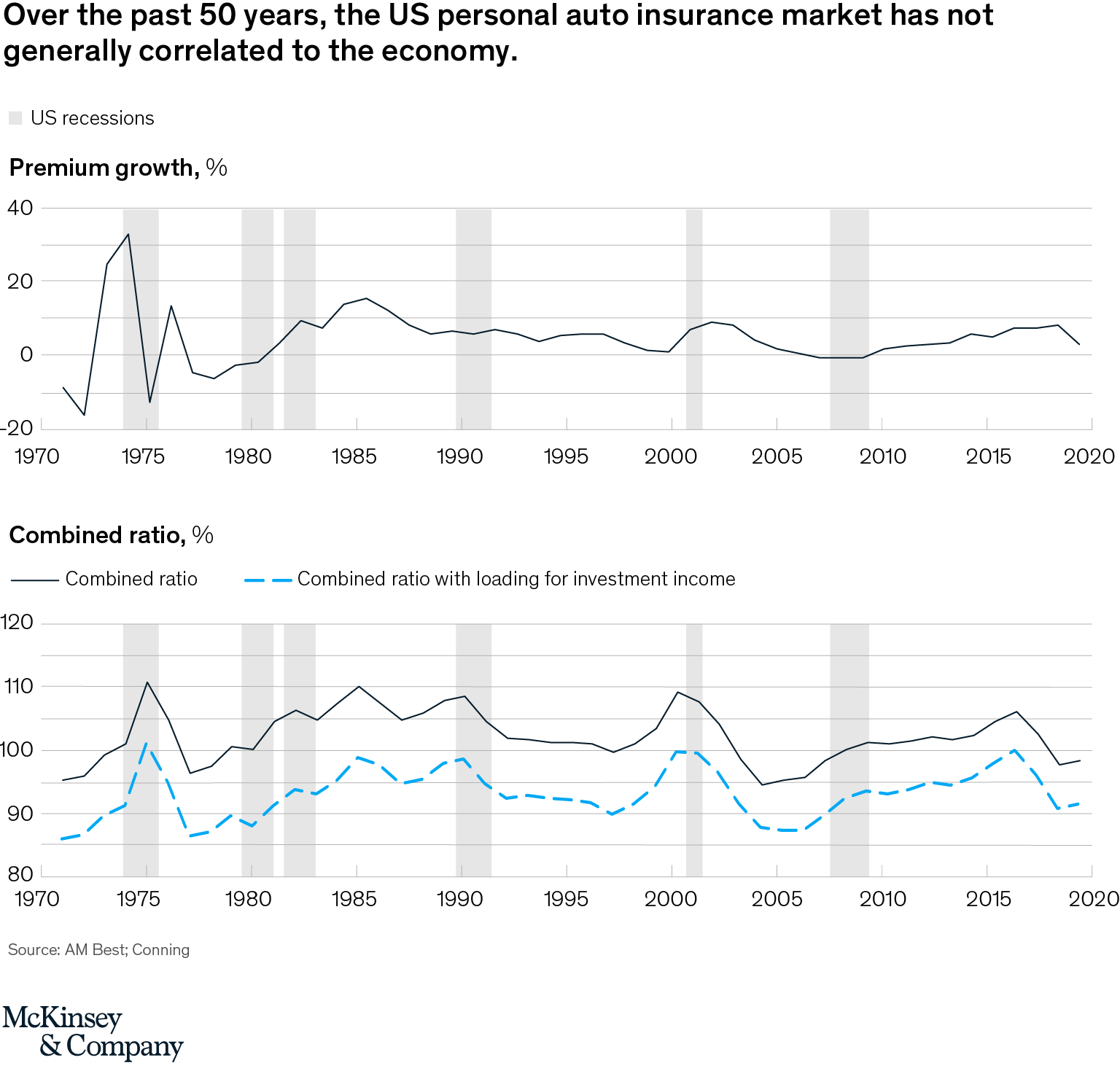

Over the past 50 years, the US personal auto insurance market seems to have been mostly non-correlated to the economy. Since 1980, the market’s premium growth and profitability trajectory were unaltered during five recessions (Exhibit 1). Within two to three years of some recessions, profitability and growth increased. The 1973–75 recession is the exception, when both growth and profitability were strongly affected. At the time, industry underperformance was attributed to poor underwriting discipline by selected companies. Tailwinds at the time, including all-time-high oil prices (resulting in less driving) and a newly imposed nationwide 55-mile-per-hour speed limit, should have improved profitability but did not.

In 2019, the US personal auto combined ratio was 98.3 percent, an improvement from a peak of 106.3 percent in 2016. From 2009 to 2018, personal auto insurance grew roughly in line with the economy, with some additional growth from improved rates. Loss ratio has been trending slightly downward, from 70 points in 2009 to 68 points in 2018 (Exhibit 2). Lower claims frequency has resulted from continued improvements in safety measures and vehicle technology, but this drop has been partially offset in states that have legalized cannabis. Higher severity reflects a continued increase in medical inflation for bodily injury, higher repair costs for cars with expensive sensor technology, and several years of “social inflation,” when verdict awards have trended upward across the US legal system.

COVID-19 will likely affect US auto insurance in two ways.

First, claims frequency will initially go down. As physical distancing is widely encouraged, particularly in states with shelter-in-place directives, individuals have been driving much less. Looking back at previous recessions since 1970, the observed decrease in frequency seems to correlate to less driving (Exhibit 3).

The recent experience in several European countries in March 2020 illustrates this pattern: within less than 20 days of the pandemic reaching 100 cases, driving decreased by 50 and 80 percent in Germany and Iberia, respectively (Exhibit 4). When there is less driving, there is a lower frequency of auto accidents.

Second, insurance companies will face top-line pressure. As new-car sales decrease, auto insurance will slow down. The impact on insurance revenues will not be one-to-one, since most new-car purchases represent a replacement of a currently insured vehicle. The United States is home to approximately 280 million cars, and annual car sales total about 17 million. Top-line revenues will be strained by any drop in new-car sales, although the impact will be moderate relative to the overall volume of insured vehicles. In addition, given the unprecedented exponential increase in unemployment, missed premium payments and policy lapses are likely to increase. The biggest impact could come from insurers returning or reducing premiums for lower usage (an issue further explored later in this article).

Four potential scenarios for near-term COVID-19 impact

The next 12 to 18 months will be shaped by two unknowns: the timing and the magnitude of the economic correction as well as behavioral shifts that could materially change driving patterns.

Observing the immediate impact, it is concerning to note the unprecedented swiftness and magnitude of unemployment claims, which in the past two weeks have reached levels not seen since the Great Depression (Exhibit 5). If the US economy has sustained unemployment of more than 20 percent, the impact will be far-reaching.

Another potential shift is in driving behavior. Public sentiment can be widely altered by traumatic events: the Vietnam War and the attacks of September 11, 2001, were examples of such events. Recent polling by the American Psychiatric Association found that 36 percent of Americans say the coronavirus is having a serious impact on their mental health, and 59 percent say it is seriously affecting their day-to-day lives.1 As populations react to trauma, some cohorts become more risk averse and cautious, while a smaller, secondary cohort engages in more risky behavior—a classic symptom of post-traumatic stress disorder.2

Given that a disproportionate number of auto accidents come from a small cohort with less-disciplined tendencies, a small increase in the activities of this group could cause claims frequency to surge. The spring breakers recently crowding beaches and the “coronavirus parties” that have been reported in some states illustrate the reality of this risk-taking cohort. Recently, the country has experienced a documented increase in speeding, as less traffic from lockdowns has left the road to thrill-seeking drivers. Excessive speeding has been reported across the United States on highways, where several states have seen a major uptick in drivers clocked at faster than 100 miles per hour, and in cities such as Chicago and New York, where individuals have been driving up to 75 percent faster since the pandemic started.3

Assessing possible behavioral changes against the length and magnitude of the economic downturn suggests four potential scenarios: pause and rebound, retrenchment, YOLO (“you only live once”), and black swan (Exhibit 6). This last scenario is unlikely, but given the uncertainty and novelty associated with COVID-19, it should be considered.

Our analysis used a projected combined ratio of 99 in 2020–21 as the starting point. Depending on the scenario, the projected combined ratio ranges from 97 (reflecting a slight improvement) to as high as 120 (reflecting a rapid and significant deterioration) (Exhibit 7).

1. Pause and rebound (combined ratio of 98)

The baseline scenario is that the slowdown will end rapidly, the rebound will be as swift as the contraction, and consumers will exhibit limited behavioral changes. The combined ratio would benefit from decreased claims frequency because of less driving, and the pandemic may lead to more conservative, cautious driving behaviors. Pent-up demand, supply-chain innovation, and infrastructure commitments would pull the economy to near preCOVID-19 levels within weeks.

New behavioral norms would result in less travel, redefine entertainment, and contribute to a more cautious outlook on life. Other important factors, such as the steady increase in vehicles with advanced safety features and more manageable levels of fraud, would also revert to preCOVID-19 levels. The net impact would be a continuation of the decades-long favorable frequency trend after the downward spike in the first half of 2020. If insurance companies return premiums, the projected combined ratio of 98 might be slightly higher.

2. YOLO (combined ratio of 106)

This scenario is defined by a relatively rapid economic rebound but also more aggressive driving behaviors. Some cohorts in the population may exhibit a YOLO outlook on life, similar to the que será, será (whatever will be, will be) exuberance of the 1970s after US soldiers returned from the Vietnam War. Fueled by cheap gas and a disdain for shared mobility, the roads and highways would become more crowded.

In this scenario, the decades-long favorable claims frequency trend would stall. Claims severity would continue its upward trajectory, putting pressure on insurers to raise rates by double digits. The sudden drop in frequency followed by a rapid escalation could strain the accuracy of actuarial techniques and regulatory expectations.

3. Retrenchment (combined ratio of 97)

The economic negative-growth scenario for the industry is defined by an extended economic decline and more conservative driving behaviors. Difficulties managing the spread of the virus and complications from the economic shutdown would produce a lengthy downturn. As in the pause and rebound scenario, after the crisis, new behavioral norms would result in less travel, redefine entertainment, and contribute to a more cautious outlook on life. The net impact would be a continuation of the decades-long favorable trend in claims frequency after the downward spike in the first half of 2020. Claims severity would moderate in line with the more conservative behaviors.

Consistent with economic conditions, a surge would occur in the nonstandard market and state risk pools. Fraud would also spike as a by-product of economic pressures. As in the pause and rebound scenario, if insurance companies return premiums or collect lower premiums, the projected combined ratio would be slightly higher. In addition, regulatory pressure could drive rates down further or force expanded coverage, exacerbating the worsening combined ratio performance. Insurers may face social pressure, in addition to regulatory pressure, to return or reduce premiums during this period.

4. Black swan (combined ratio of 120)

This scenario reflects the worst case for economic contraction and behavioral changes, combining the YOLO and retrenchment scenarios. The result would be new behavioral norms that generate a YOLO outlook on life and compromise policing and enforcement capabilities from the toll of the pandemic. The decades-long favorable claims frequency trend would reverse after the downward spike in the first half of 2020. Claims severity would continue its upward trajectory.

Residual market loads, increased fraud, and the meltdown of subrogation norms would push rate indications north of 15 percent. Markets could mirror the state environments that insurers abandoned in the 1980s. In addition, regulatory pressure could push rates down further or force expanded coverage, exacerbating the worsening combined ratio performance. Insurers may face social pressure, in addition to regulatory pressure, to return or reduce premiums during this period.

Across the above scenarios, the more extreme are, of course, less likely—but, for risk analysis, they are critical to anticipate. The frequency and severity assumptions of these scenarios are summarized in Exhibit 8. Regardless of the scenario, US personal auto lines could be materially affected by COVID-19.

Implications for carriers

While the exact outcome of the pandemic is uncertain, US personal auto insurers must navigate several implications in their response to the crisis and strategic planning:

Reevaluate current pricing models

If the economic contraction is significant and unemployment exceeds 20 percent, credit scores will implode and current pricing schema may fail, especially if aggressive driving behavior becomes prevalent or extreme social-inflation factors exacerbate ongoing severity trends. Data scientists and actuaries should take a hard look at current models and consider recalibrating them.

Prepare for disruption in the standard market

A prolonged recession and high unemployment could result in a surge of risks outside the standard market. Insurers should be proactive in working collaboratively with regulators to shape the appropriate public response, including state funds and assigned risk pools. Potential solutions could include creating fair mechanisms for all stakeholders and adapting products and endorsements to respond to difficult conditions. Insurers should also sharpen their fraud-detection capabilities.

Devise a near-term marketing strategy

Marketing spending represents the largest variable or semi-variable cost for auto insurers and can account for up to ten percentage points of the combined ratio. Executives may consider pausing their spending, whether on internet leads, direct mail, or TV ads. This move may seem counterintuitive to carriers concerned about declining new-business volume, but it makes sense in the face of depressed shopping activities. In downturns, the ROI for retaining customers is often multiples of customer-acquisition spending, so customer retention becomes far more important. Even when marketing resumes, aligning the tone of messaging to address consumer sentiment is key. For example, using recurring humorous themes may not be the right approach in markets ravaged by the pandemic.

Consider ways to support struggling consumers

If mobility trends slow or the country faces a sustained economic downturn, the historic exposure standard of a car month or car half year will be upended. Already, leading US companies have announced programs to return premiums to customers, who no doubt appreciate a tighter economic link to their behaviors. Beyond this, insurance companies may consider other ways to show support and empathy—for example, checking in with customers to see how they are weathering the current crisis.

Anticipate long-term, secular shifts in the industry

The COVID-19 pandemic may have far-reaching consequences in reshaping the industry. Examples include the following:

Accelerated digital-channel adoption. This crisis will increase the momentum already underway for carriers, agents, and consumers shifting to digital channels. In the past few weeks of this pandemic, millions of Americans are becoming more comfortable with virtual meetings, video chatting, and online transactions for previously in-person activities such as grocery shopping. Personal auto has been at the frontline of digitization for the insurance industry, but the pandemic underscores the need to increase the emphasis on digital channels.

Higher adoption of telematics. With the prospect of pandemics recurring in the future, telematics directly addresses the consumer need to pay lower premiums when vehicles have lower utilization during periods of lockdown. Consumers will look for products that “go to sleep” for periods of nonuse, which would maintain compliance with state insurance regulations while allowing insurance protection that reflects reduced usage more appropriately. Telematics would remove the guesswork and ambiguity, allowing usage-based pricing that is more equitable for the consumer and more precise for the insurance company.

New ways of working. In McKinsey’s discussions with executives, many have remarked that the remote mode of working has proved to be more efficient, in many ways, than the status quo. This crisis is a wake-up call to rethink the operating model and build a more efficient, resilient infrastructure. The future may bring more remote-work call centers, lower commercial real estate costs, and more dispersed footprints across geographies, among other changes. The journey to the future-state model may accelerate, given the recognition that subsequent COVID-19 outbreaks or other pandemics could have a similar and sudden impact in the future.

Shifts in driving patterns. The pandemic may change the consumer attitude about shared resources. Individuals may rely less on public transportation and ride sharing to avoid the risk of infection from heavily utilized modes of transportation. The rollout of autonomous vehicles could slow down, given their interdependence with driverless fleets. Conversely, the prospects of driverless fleets could become more attractive, especially as an alternative to public transportation, as long as a robust hygiene protocol ensures adequate sanitation. The utilization of personal vehicles for commercial use may also increase, with more deliveries, whether by small businesses or via digital delivery apps. We already see ride-share drivers becoming more involved with grocery delivery and other services.

As the economy faces the pandemic head on, the impact on the industry at the other end of the tunnel could be marginal or seismic. US auto insurers must engage in rigorous scenario planning for multiple outcomes over the next 12 to 18 months and evaluate investment priorities. Executives should be forceful about reallocating capital and continuing—perhaps accelerating—the transformation activity in pricing, marketing effectiveness, customer experience, and product innovation that may have been underway before COVID-19.4 Insurers must also appreciate the longer-term changes that this pandemic may precipitate in the industry.

Above all, now is the time to show empathy for consumers who are affected by this tragedy, placing human welfare before profitability. It is the right thing to do, and it will lead to stronger customer loyalty and retention.