Banks in Latin America are no longer immune to the global credit crisis. True, it’s had little direct impact on them, because they made only limited investments in US and European mortgage-backed securities. Still, a high dependence on exports and commodity prices pushed Latin American economies into recession after consumer spending and industrial production fell in Europe and the United States. As a result, the rate of growth in lending has begun to decline, nonperforming loans are on the rise, and profitability is down.

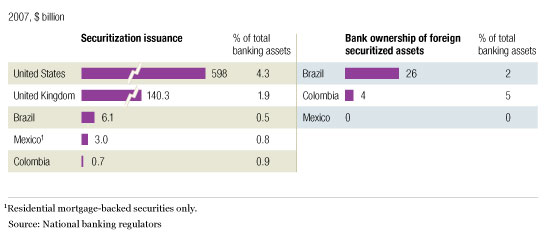

Nonetheless, McKinsey analyses of the banking sectors of Brazil, Mexico, and Colombia1 show that strong starting capitalization, liquidity, and capital should allow their banks to remain profitable and well capitalized. Before the crisis, foreign securitized assets ranged from 0 to 5 percent of total banking assets in Brazil, Mexico, and Colombia, and domestic issuance of securitized assets was far below that of the United States and the United Kingdom. As a consequence, Latin America was relatively unscathed when the value of these assets dropped precipitously.

Less exposed

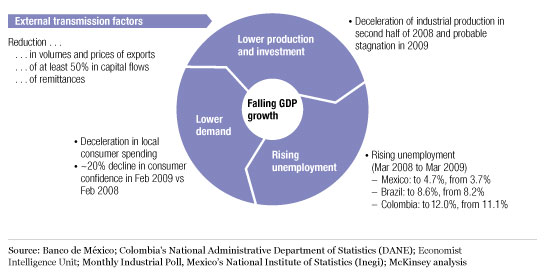

Latin American economies, though, have felt the effects of the financial crisis through a downturn in demand and capital from major world economies. Cross-border trade fell sharply: the Baltic Exchange Dry Index (BDI) of shipping costs for major raw materials sank by 94 percent from May 2008 to November 2008, for example. Growth in real consumer spending in the United States turned negative during the second half of 2008, and commodity prices decreased by 20 to 60 percent for key exports, such as oil, copper, coffee, and soy.

During the first quarter of 2009, the real volume of exports was 9 percent lower in Brazil and Colombia and 15 percent lower in Mexico than it had been a year earlier. Foreign direct investment fell by one-fifth in Mexico and by one-half in Brazil in 2008. Reduced external demand led to declining industrial production, rising unemployment, and a fall in local demand (consumer confidence in the three countries was about 20 percent lower in February 2009 than it had been during the same month in the previous year). In 2009, real GDP is expected to contract by 5.9 percent in Mexico, by 1.8 percent in Colombia, and by 1.2 percent in Brazil.2 The Mexican economy is particularly vulnerable because of its dependence on exports to the United States, which absorbs 80 percent of them.

Slowing down

Governments in Latin America have taken action by reducing reference interest rates and increasing expenditures to spur economic growth, so many governments are also increasing their levels of bond issuance to finance rising deficits. Currencies have recovered somewhat since last autumn’s massive depreciation but are still 20 to 30 percent below year-ago levels. Stock markets have recovered partially but remain about 25 percent down, year on year, in Mexico and Brazil, while Colombia’s has almost fully recovered.3

Declining industrial production and consumer spending in Latin America have slowed the growth of its banks’ loans. Consumer lending, after the rapid expansion of recent years, has suffered the biggest decline in growth, particularly in Mexico (where it fell to –1 percent in 2008, from 29 percent in 2006 and 2007) and Colombia (down to 15 percent, from 38 percent).

A drop in growth

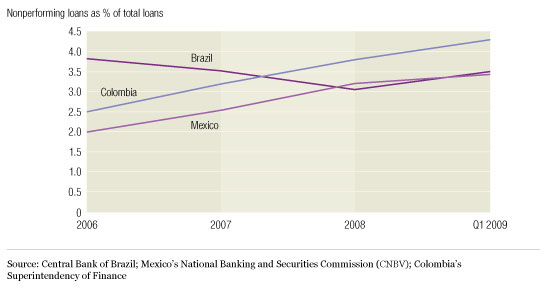

The level of nonperforming loans was up before the crisis, primarily because the increased leverage of existing customers was a major driver of Latin America’s rapid rise in consumer lending. Now, as a result of the recession, rising unemployment is pushing levels of nonperforming loans even higher. Around 8 percent of total consumer loans in Brazil, Colombia, and Mexico were nonperforming at the end of 2008, as were 11 and 28 percent of all credit card loans in Mexico and Brazil, respectively. The increase in consumer nonperforming loans is the major driver of the higher rate of overall nonperformance.

On the rise

In 2008, banking’s return on equity fell to 13 percent, from 20 percent, in Mexico and to 19 percent, from 28 percent, in Brazil, while the sector’s ROE in Colombia remained stable. Banks in Mexico and Brazil experienced a significant decrease in interest income and in fees and commissions, combined with rising provisions. Colombia’s banks, by contrast, raised their interest rates, especially on credit cards and corporate loans, so their ROE remained stable despite rising provisions.

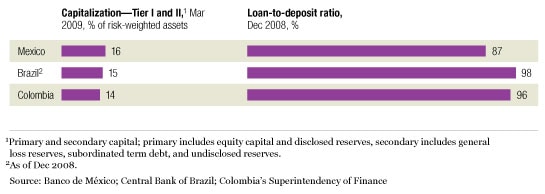

Even so, Latin American banks remain well capitalized, with good liquidity—in part because they implemented international standards for banking regulation and followed conservative strategies after the regional financial crises of the 1980s and 1990s.

Well capitalized

While larger banks have proved resilient in the face of the crisis, small ones and nonbank financial institutions are struggling across the region because they relied on capital market funding that is now both more expensive and harder to get. In Mexico, the total assets of the nonbank finance companies called SOFOLs and SOFOMs declined by 28 percent in 2008.

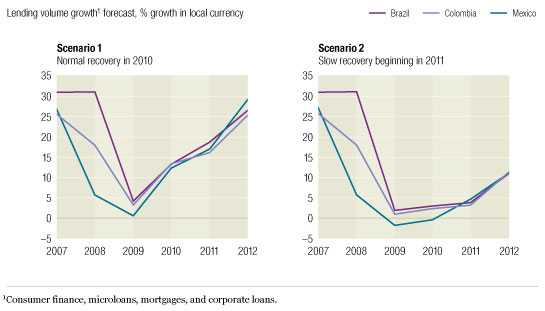

To estimate the recession’s impact on the future profitability of Latin American banking, we forecast loan growth, margins, risk costs, operating costs, and economic profit under two macroeconomic scenarios. The first was a normal recovery from a moderate recession of three to four quarters in 2009, with the economy recovering and beginning to grow in 2010. The other was a slow recovery from a moderate recession of one to two years, followed by slow economic growth starting in 2011. In these analyses, lending comprises consumer finance (including credit cards), microloans, mortgages, and corporate loans.

The normal-recovery scenario leads to slow lending growth this year followed by a recovery next year and a return to 2007 growth rates in 2012. In the slow-recovery scenario, the growth of lending is near zero in 2009—and it actually contracts in Mexico—and recovers to one-third of 2007 levels in 2012. The actual growth of lending in the first quarter of 2009 (shown in Exhibit 3) has been closest to the levels of the slow-recovery scenario.

Growth in lending: Forecasts vary

We then conducted stress tests for each country to see what would happen to the worst-performing major bank under our scenarios. For each country, we chose the bank with the lowest 2008 ROE among the six largest institutions, excluding state-owned banks or banks involved in recent mergers. Using the assumptions from the normal- and slow-recovery scenarios above, we estimated future ROE and capitalization.

In both scenarios, banks in all three countries remain profitable and above both the local capitalization requirements (9 percent in Colombia, 10 percent in Mexico, and 11 percent in Brazil) and the international one (8 percent under the Basel international banking accords). The performance of banks will probably deteriorate, though, as a result of slower growth in their lending portfolios and higher provisions. In the stress test, the Mexican bank performs better in 2009 because its provisioning was much more aggressive in 2008 than that of the other countries’ banks. Actual first-quarter results are more positive for the Brazilian and Colombian banks than the 2009 stress test results, while the Mexican bank’s results are slightly lower.

Even the worst will be OK

The economic decline has affected Latin American banks through a drop in demand for loans, a decline in the quality of borrowers (both individual and corporate), and increased funding costs in the capital markets. While we forecast that the revenue growth of Latin American banks will decline, we believe that they will remain profitable and well capitalized.

In response to the crisis, banks are taking actions in three areas: operations, risk management, and corporate finance and strategy. To offset declining revenue growth, banks have tried to cut operating costs and to raise interest rates or fees for services selectively. Many banks are addressing higher risk costs by imposing more stringent credit policies and working with customers to refinance their loans. To save capital, some banks are delaying their branch expansion plans. Meanwhile, as capital market funding has become more expensive, banks have begun to compete more aggressively for deposits. Some are taking advantage of their competitors’ depressed market valuations to explore M&A opportunities.