Most US mortgage originators have struggled to compete profitably in a rapidly transforming competitive landscape. Non-depository originators have been stealing share from banks, doubling their US market share from 25 to 50 percent over the last 10 years. Digital mortgage players are on the rise, and direct-to-consumer (DTC) originations account for a growing share (more than 25 percent) of the market. Meanwhile, customer expectations for speed, transparency, convenience, and personalization are being raised by their digital experiences outside banking.

Suffice to say, there is huge room for improvement. A home mortgage remains the biggest financial transaction of most people’s lives. For many it is also the most frustrating and lengthy financial transaction they’ll ever endure. Recently, we conducted a survey of more than 1,200 residential mortgage customers to better understand their experiences and how banks and non-banks can deploy technologies to improve those experiences. Only 42 to 67 percent of borrowers say they are satisfied with the mortgage process, and banks fared worse than non-banks, lagging by about 20 to 30 percent (Exhibit 1).

These customer satisfaction scores leave plenty of room for improvement, and our survey findings led to four insights that banks can apply to make a strong start.

1. Price is not always king; customer experience is a real differentiator

One of the most interesting findings was that most customers reported that an “exceptional customer experience” was almost as critical to them as getting the “best rate.” In fact, first-time home buyers said that learning—either through online reviews or word of mouth—that a lender delivered an exceptional customer experience was the most important factor in their decision to choose a lender. This speaks to a clear opportunity for originators to differentiate on service without sacrificing pricing and margins.

2. Reassurance, transparency, simplicity, and speed are critical during the mortgage journey

Customers care about four specific dimensions of their mortgage experience: reassurance, transparency, simplicity, and speed (Exhibit 2). They weight these four areas almost equally, though they give reassurance a slight edge. Reassurance here means having helpful, knowledgeable, and accessible employees who can confidently guide and support customer decisions. It also means “getting things right the first time” and avoiding eleventh-hour surprises (e.g., minimizing multiple and unnecessary document requests, sending accurate disclosures on time, and not “missing” information sent by the borrower).

In terms of transparency, customers want accurate and unambiguous information about pricing, the time needed to complete each step in the mortgage process, and real-time application status. As for simplicity, customers want an application with clear next steps, as well as straightforward documentation and credit assessment guidelines that they can easily understand.

And, finally, speed is crucial, both before and after choosing a lender. Customers move fast and expect institutions to be nimble enough to keep up with them. Customers typically select a lender within two to three weeks of starting their research into mortgage providers, and submit an application within another week. Remarkably, up to 35 percent of customers in certain segments (e.g., repeat home buyers) select a lender within just three days after starting their search. They want to complete the application quickly and, if they already have a relationship with the lender, they expect the lender to use the financial data it already has rather than ask them for more documents. Naturally, borrowers also want a quick conditional decision and fast time to close.

While mortgage originators should target improving each of these four satisfaction dimensions, respondents highlighted several particularly critical issues for the customer experience. Originators should prioritize getting things right the first time, offering quick, clear, 24x7 status updates, pre-approval within 24 hours, and providing a single point of contact.

New digital tools—along with customers’ growing comfort using them—make these priorities more achievable than ever. It helps, for example, about 60 percent of customers say that they are comfortable with a completely online application, and that another roughly 30 percent are comfortable with online applications with some combination of phone and/or in-person support.

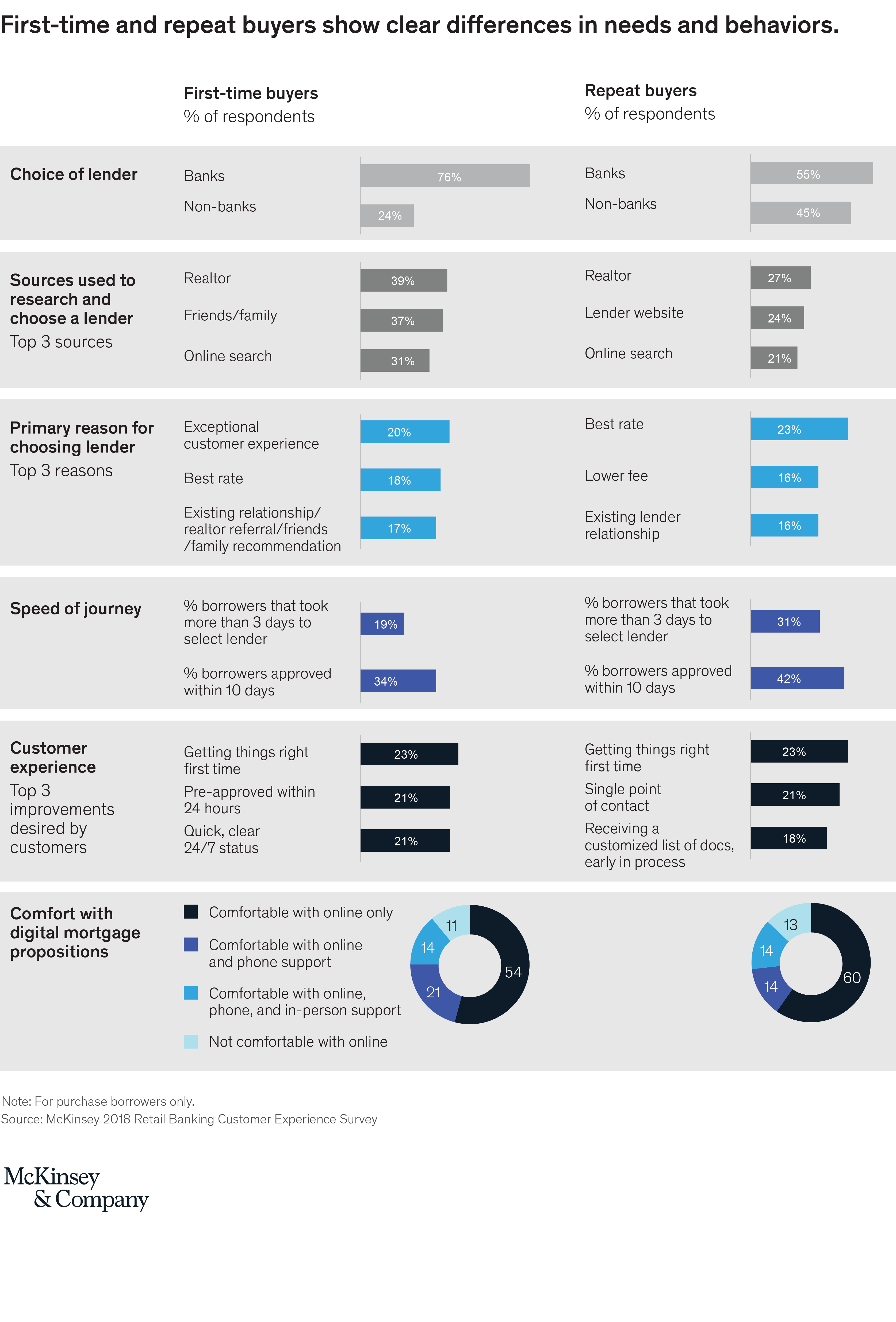

3. Understanding customer behavior and preferences helps lenders prioritize investments in customer experience

Our research on how different borrower segments behave and prioritize specific experiences provides valuable clues for originators on how to target these segments (Exhibit 3). For instance, when looking to attract first-time home buyers, banks should focus equally on online and offline channels. They should also keep in mind that first-time home buyers rank customer experience higher than pricing as a primary purchase criterion.

First-time home buyers, understandably, take longer than their more experienced peers to choose a lender, and are more likely to apply to three or more originators. This makes a streamlined and transparent process, which includes pre-approval within 24 hours and 24x7 status updates, particularly critical for this segment. In contrast, repeat home buyers make their lender selection more than 60 percent faster than first-time home buyers, and prioritize rate and speed.

Similarly, when looking to attract jumbo borrowers, banks should know that interest rate is paramount. That said, having an existing relationship and providing a good customer experience are important factors. Jumbo borrowers put a premium on having a single point of contact at the bank and, especially if they have an existing relationship, they expect the bank to leverage existing financial information instead of asking for repeat documentation.

4. Digital marketing, technology, and operating model investments are crucial for competing with non-banks

Our research also examines how banks can better compete with non-banks to win in specific customer segments. Today, despite underperforming non-banks in terms of customer experience, banks still capture about 75 percent of first-time buyers. But they will need to invest heavily in technology or risk ceding further market share to non-banks. Indeed, many of today’s digital innovations—like mobile digital document uploads, automated quality assurance, application data pre-fill using internal and external APIs—will soon become table stakes. We believe that US mortgage providers will need to compress average purchase cycle times to 15 days, and lower mortgage origination costs per unit from about $8,500 today to less than $5,000.

Banks need to move beyond their reliance on traditional word-of-mouth references, improve their online visibility (for example, through search-engine optimization and digital marketing), and modernize their online customer portals (e.g., with clear propositions and processes, better user experiences and user interfaces, and digital applications).

Banks should also do more to cross-sell to existing customers. In fact, among both conforming and jumbo mortgage borrowers, an existing relationship is one of the top three reasons for choosing a lender. To seize this significant advantage, however, incumbents will require vastly streamlined processes and fewer handoffs. This means redesigning the end-to-end customer journey to eliminate the most critical customer pain points, digitizing and streamlining the operating model, deploying automation to simplify processes and reduce costs, investing in digital marketing to attract attention early, and applying advanced analytics to drive efficiency and growth and improve risk and talent management.

We expect that these four customer experience themes will continue to shape the US mortgage marketplace over the next five years. Unless they adapt, bank originators will struggle, and some may be forced to exit the business. Those that invest in transforming the customer experience will be well positioned to compete.