When it is done right, customer experience in retail banking leads to more satisfied customers, happier team members, increased efficiency, accelerated growth, and reduced operational risk.

Done wrong, customer experience initiatives can lead to cynicism—huge amounts invested, generally happier customers, but limited financial returns.

To figure out which parts of the experience are working and which are not, banks run “voice of the customer” programs to get broad customer feedback. This data then informs customer experience investment decisions.

While the intent behind these programs is right, they are often poorly designed or involve simplistic approaches to the data and analytics, leading banks to focus on the wrong things. Common failure modes include:

- Solving for customer experience scores as an end in the themselves, especially with arbitrary net scores such as 9s and 10s, minus those who give a 6 or below

- Gathering customer feedback primarily on individual interactions or touchpoints, rather than full journeys (e.g., onboarding, issue resolution)

- Asking the same few questions of all customers, which makes it hard to analytically define the underlying drivers or determine which issues matter most

- Failing to integrate with customer-level segmentation, operational and financial data

Simple customer experience metrics—what we often call “topline” metrics, such as “overall customer satisfaction” and its proprietary peers—can be an important part of creating cultural change and focusing on the voice of the customer. But they should not be the primary factor in more specific decisions, such as which parts of the experience to transform first and how to do so.

We encourage a more value-oriented and analytically informed approach to prioritizing investments in CX:

- Get more useful feedback: Gather feedback journey-by-journey, ask questions about what shapes the customer experience, and optimize the approach to ensure representative feedback. This means asking different customers about different elements of experience so that no one customer is overwhelmed.

- Integrate “customer voice” with operational and financial data, as well as advanced analytics: Connect feedback from individual customers to customer-specific operational and financial data, including their digital footprints, other channel interactions, product usage, cost-to-serve, and revenue data. Tell the full story using “journey analytics” (that is, connecting disparate channel interaction data to paint a comprehensive picture) and increasingly with predictive analytics (for example, to infer sentiment for the vast majority of customers who do not respond to surveys).

- Analyze data for two kinds of insight: First, identify where changes in experience will result in different customer behavior that creates more value. Second, find “breakpoints”—places in the journey where changing a particular element of the experience will have a disproportionate effect on the overall outcome.

Most of the banks we work with are seeking a more actionable view of current state experience. We ask customers about their journey-specific experiences, what shapes their experience, and how they interact with their banks as a result.

The specific changes that deliver value will differ from bank to bank. We integrate operational and financial data to ensure as nuanced and actionable a picture as possible, while minimizing the questions we have to ask customers. And we use our annual benchmarking of more than 25 leading US banks and lenders to talk about where and how to look for the opportunities, using industry-level data as a point of departure.1

When we analyze customers’ experiences by journey and how those experiences effect their behavior, four themes jump out:

- “I’ll be loyal to my bank, unless they treat me really badly.”

- “Teach me how to make the most of digital tools.”

- “Help me figure out which product is right for me.”

- “Explain the process more clearly.”

Unpacking these four messages illustrates how a different approach to customer experience feedback and analysis can yield better results and reduce wasted investment.

1. “I’ll be loyal to my bank, unless they treat me really badly.”

Customers do not switch banks because one provides an “okay” experience while another is amazing. They switch banks because they are fed up with their current bank. Conversely, highly satisfied customers are not necessarily the biggest driver of value for customer experience efforts.

For example, only 7 percent of customers who ranked their satisfaction with their primary bank a 10 out of 10 said they would buy new products there. However, 45 percent of customers who gave their overall experience a 4 out of 10 said they would close some or all of their accounts and look for an alternative provider.

Customers appear to go through a two-step process when they are unhappy with their banks: first, frustration makes them look at other options, despite the hassle; second, now that they are in the market for a new bank, they determine which of the alternatives is the right fit.

In other words, when customers break up with their banks, they’re most often doing so because they are very unhappy with their current bank, rather than because they are drawn away from an otherwise good experience by their excitement about another bank’s new and even better experience. (Note that this marks a contrast between experience and price, where the latter is more likely to pull an otherwise satisfied customer away, for example with a better rate on a loan.)

A mortgage example: In our research, the roughly 10 percent of customers who rank their overall mortgage experience a 4 out of 10 or less are two to five times as likely to refinance elsewhere than customers who give a 5 or higher (Exhibit 1).

These figures explain the valley of despair so many banks face with their customer experience investments. Banks have finite resources for CX investments; simply trying to move customers as a block from “unhappy” (6 or less) to “okay” (7 or 8) to “great” (9 or 10) is not necessarily the best way to move the needle.

Banks need to find the breakpoints where small changes in experience will boost loyalty the most—the challenge is that these points vary among customer segments, journeys and products, and so the specifics of the analysis matter.

2. “Teach me how to make the most of digital tools.”

Leading retail banks have invested billions of dollars in creating digital experiences for customers—and if the proliferation of 5-star app ratings is any indication, a number of banks have built great digital offerings.

The problem is that great digital experiences are not automatically translating into great customer experiences overall. Unsurprisingly, customers who use mobile apps most frequently are the most satisfied with their bank (Exhibit 2). So far, so good. However, the second-happiest group of customers hardly ever use a mobile app at all.

Between these two poles are customers using their banking app between a few times per year and a few times per month. When we factor in qualitative feedback from customers, it becomes clear that this group is “caught” in the digital transition.

Once again, the typical approach to measuring customer satisfaction can lead to misdirected investments. Many banks use a “90-day active” number as a baseline for measuring mobile engagement; but according to the numbers we cited above, applying this measure would lump the least happy cohort (customers who use mobile once every three months) in with the most satisfied customers.

Indeed, we believe that the biggest banks have lagged their regional peers in customer experience (despite their much larger digital investments) in part because more of their customers are in the midst of the dip associated with the digital transition, while for some regional banks a larger number of their customers have not yet started.

“Build it and they will come” is not a sound strategy for banks seeking to increase digital adoption. There is a significant opportunity for banks to invest in their branch and contact center experiences, and in well-designed marketing, to help coach customers on how to make the most of these digital tools. Doing so will cost a fraction of what banks are spending on technology today, while amplifying the returns meaningfully.

3. “Help me figure out which product is right for me.”

Banks have invested heavily in improving the application experience. The business case for doing so is clear—reduced fallout from applications is one of the best ways to improve overall sales funnel performance.

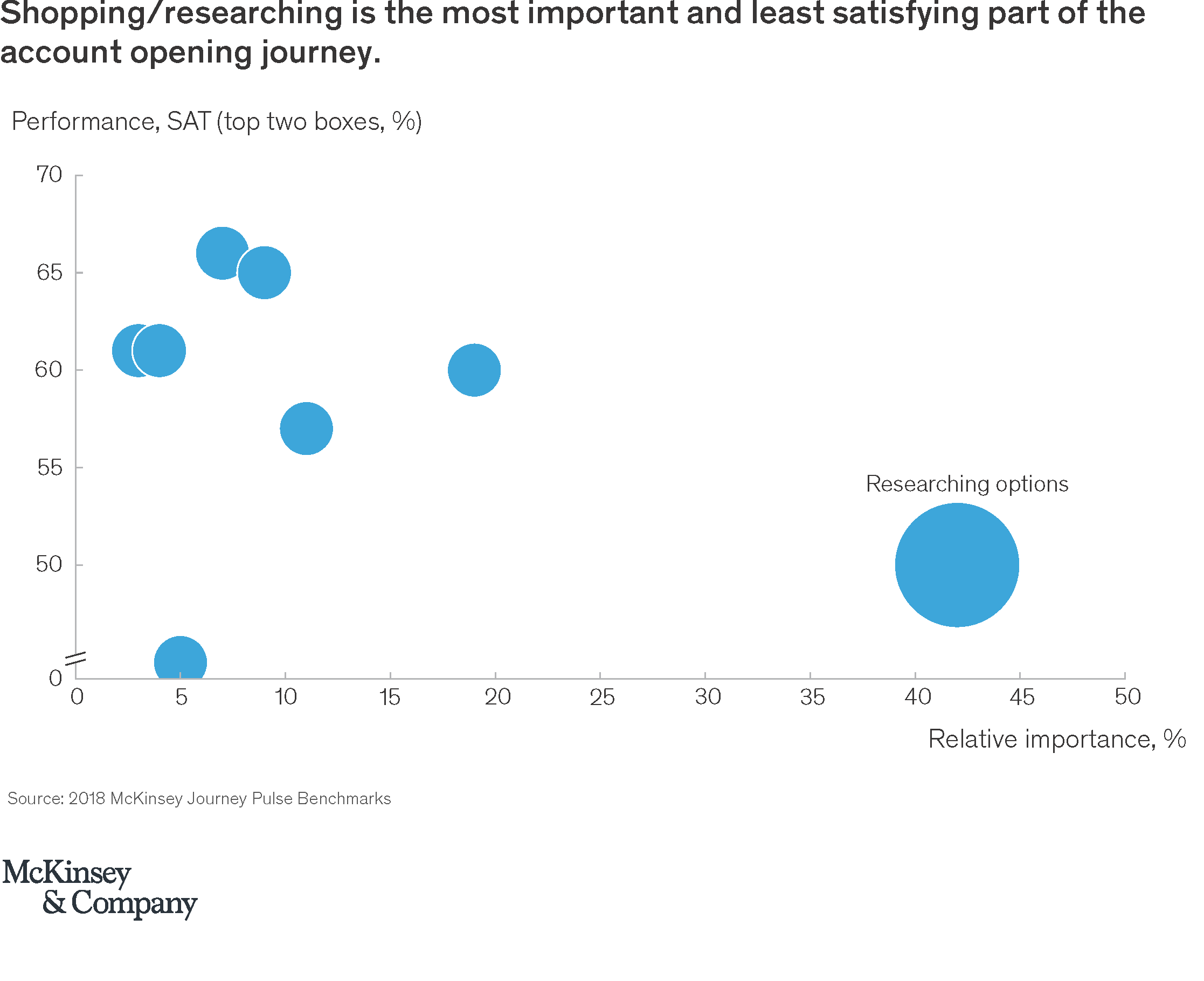

Now, however, customers are asking for help earlier in the process, but banks are failing to deliver. “Researching options” is one of the worst-performing steps in the onboarding journey and twice as important to overall onboarding satisfaction as any other single step (Exhibit 3).

Many retail banks seek to excel at advice. This is a worthy goal, but customer feedback suggests there is a more attainable near-term response that can significantly boost satisfaction: explaining currently available products clearly and simply, so customers can better tell for themselves which one is best for them.

4. “Explain the process more clearly.”

There is a similar dynamic at play in issue resolution. Banks have invested a tremendous amount in making customer service faster and training their teams to be warm and friendly. And those investments have paid off.

Now that a new baseline has been established, however, customers are expressing a desire for clearer communications and well-managed expectations (Exhibit 4). While banks have done well to reduce long wait times and raise the bar on the friendliness of their customer service staff, the next wave of improved experience with customer service is likely to be based on clear explanations and transparency into processes.

In other words, customers do not need the pizza delivered faster, but they would like to know exactly when it will arrive.

Every bank’s customer experience opportunities can be laid out in 10 to 20 analyses like those above, integrating customer feedback with operational and financial data to suggest specific worthwhile investments and flag those that can be deprioritized. Chasing topline scores alone, using arbitrary cut-offs to define good and bad experiences, and making choices without an analytically informed view of the drivers are recipes for wasted investment.

Leaders gravitate toward customer experience because it is the only management approach and strategy that makes it possible to address issues for customers, team members, shareholders, and regulators with a single concerted effort.

Doing so without analytical rigor fosters wasted investment and cynicism.

Done right, customer experience offers a path forward that puts banking on the right side of customers in a sustainable way. That is worth fighting for.

The authors would like to acknowledge the contributions of Victoria Bough and Marc Levesque to this article.

1. McKinsey’s Journey Pulse is a proprietary solution for understanding customers’ overall and journey-specific experiences and the drivers of those experiences. It is the basis for the benchmarks described in this post. For individual institutions, Journey Pulse integrates operational and financial data to ensure as nuanced and actionable a picture as possible, while minimizing the questions asked of customers.