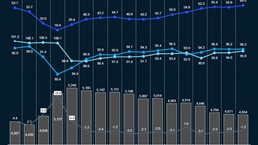

Brent averaged USD62.5/bbl, declining by USD1.3/bbl m-o-m, as the market remained oversupplied (62 MMb/d):

- Global oil demand. Global oil demand stood at 105.26 MMb/d, with an increase of 0.7 MMb/d. This was largely driven by a 0.5 MMb/d and 0.4 MMb/d increase in China and Japan, respectively, due to winter power and fuel needs and declining oil prices, resulting in stockpiling and higher refinery runs. Oil demand in other countries has remained unchanged since October

- OPEC 9 production (excl. Iran, Venezuela, Libya). OPEC 9’s output held steady at 29.1 MMb/d as Saudi Arabia increased its production by 200 kb/d to 9.9 MMb/d, signaling a calibrated move to reassure consumers on supply security while still broadly aligning with the group’s market‑balancing strategy

- Non-OPEC production (excl. US shale). Non-OPEC production decreased by 0.6 MMb/d, to 64.1 MMb/d, driven by Kazakhstan (-0.29 MMb/d due to unplanned export terminal disruptions and weather conditions), and Brazil (-0.1 MMb/d due to maintenance shutdowns at pre-salt FPSOs and delays in ramping up new offshore fields amid regulatory hurdles)

- US shale oil production. US shale output held steady at 9.2 MMb/d, while the rig count stood at 528 in December (32 fewer than a year ago) but no change since previous month

- Iran, Venezuela, Libya production. The combined output from Iran, Venezuela, and Libya stayed flat at 5.6 MMb/d, with Venezuela’s -0.09 MMb/d decline linked to the U.S. naval blockade since Dec 2025, which sharply constrained exports and forced to rely on near-capacity onshore tanks and expanded floating storage, prompting targeted output cuts

- Commercial inventories.1 Global commercial inventories increased by about 62 million barrels in December to roughly 4.8 billion barrels, driven by a build in both non-OECD (+35 million barrels) and OECD (+27 million barrels) stocks. Overall, OECD inventories are now around 160 million barrels above the five‑year seasonal December average of about 2.7 billion barrels

- Market sentiment.December market sentiment for crude was cautiously bearish, as OPEC+ production increase, robust non‑OPEC supply, and above average global inventories, outweighed geopolitical risks, rising demand, and local supply disruptions, keeping prices capped and any upward moves brief

1 Non-OECD share of inventories is estimated, assuming that non-OECD inventories have 50% days of demand cover of OECD inventories

Download dashboard:

Oil supply & demand dashboard: December 2025

Subscribe to Energy Solutions

To receive our oil supply & demand dashboards, please subscribe to upstream oil and gas updates from Energy Solutions.