Two years after the collapse of Lehman Brothers, 51 percent of executives who responded to our most recent survey say the world economy is in recovery; 58 percent say so about their own countries.1 Most expect corporate profits to rise this year from their level in 2009, and 38 percent expect to hire by the end of the year—the greatest share expecting to hire in the near term since before the crisis.

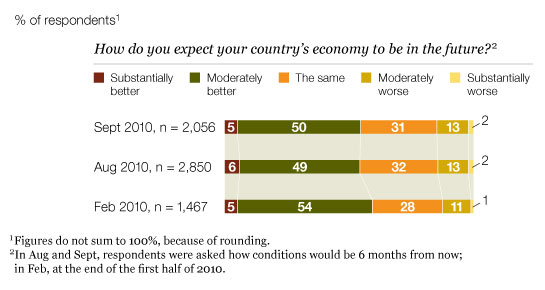

Even if companies are coping with the new economy, the results also indicate that executives’ confidence is tenuous. For example, more expect economic conditions to improve than not, but fewer say so now than did earlier this year. Notably, the share of respondents expecting better conditions in six months is lower than it was a year ago: 55 percent now, compared with 61 percent in September 2009. Furthermore, optimism on the current state of the economy compared with six months earlier started to fall in June and has taken a sharp dive in the past month. Compared with August, 10 percentage points fewer say the economy is better now. The slide is particularly notable in North America, where the share of respondents who say conditions are better has fallen 16 percentage points.

Among the lasting changes that executives say the downturn has produced in their organization are greater attention to changes in markets, improved risk management, and much stronger consciousness of costs. More than half of respondents have changed the criteria they use to make capital-investment decisions, most by applying more rigorous due diligence. Notably, though, most respondents don’t expect permanent changes in their companies’ workforce size or geographic location.

Getting used to trouble?

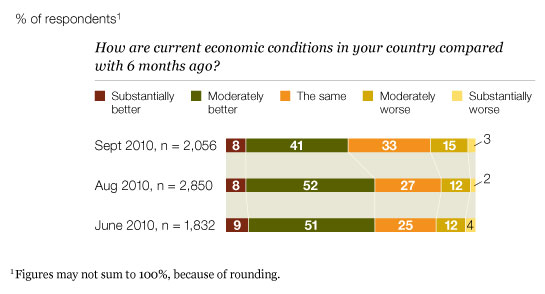

Executives’ economic hopes rose consistently from the depth of the crisis in January 2009 through December of that year but began to falter in February 2010; now, just over half expect better conditions six months from now (Exhibit 1). From January of last year until this June, the share of survey respondents who said that current conditions were better than they were six months earlier continued to grow; that figure remained stable in August but has now fallen (Exhibit 2).

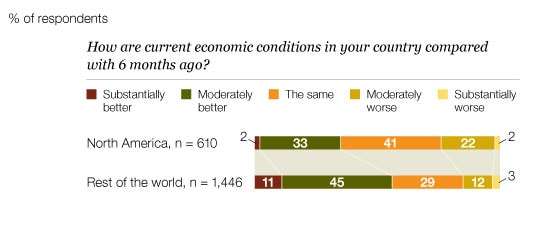

The biggest decline in the share saying current conditions are better is in North America (Exhibit 3), after a smaller drop between June and August. The sharp drops, largely in the United States, came as growth slowed and high levels of unemployment persisted.

Despite executives’ increasing unhappiness with current conditions over the past month, the share of survey respondents expecting economic improvement has remained stable, and 81 percent expect their countries’ GDP to improve this year compared with last year. Earlier this year, executives’ views on current conditions continued to improve even as their hope faltered. But that has switched; now circumstances are almost reversed. This may simply indicate that executives have grown somewhat used to a more volatile economy.

Cautious optimism

Current discontent

North America’s malaise

Companies coping

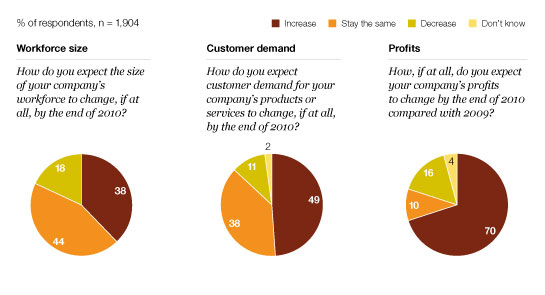

Executives’ expectations for their companies’ performance have remained fairly stable; the share expecting demand to increase is identical to that for August, and the share expecting increased profit is nearly the same. Further, that 70 percent expect higher profits now (Exhibit 4), compared with 42 percent a year ago, suggests that companies are learning to manage successfully in an uncertain economy.

One crucial element of adaptation for companies, it seems, is how they assess risk. Since September 2008, 57 percent of respondents say their companies have changed the criteria by which they make capital-investment decisions, and nearly 70 percent of those say the change has been more rigorous due diligence. Furthermore, although two-thirds of respondents say their companies are not postponing or failing to pursue capital invest-ments or M&A that they would normally consider to be good growth investments, among those that aren’t investing, 59 percent say the reason is that they’ve adopted a more conservative risk profile. Similarly, when asked about the downturn’s lasting effects, many respondents refer to risk management, cost management, or conservation of cash.

Barometers of business change

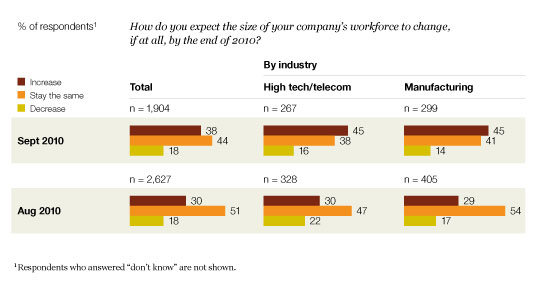

Another finding that suggests companies are coping, if cautiously, is that 38 percent expect to increase the size of their workforce by the end of this year. This is the highest share expecting to hire since before the crisis. Respondents across all regions expect hiring to be up; those in high tech, telecommunications, and manufacturing are the likeliest to say their companies will hire (Exhibit 5). In addition, respondents at small and large companies are equally likely to say their companies will hire,2 though 23 percent of those at large companies expect continued decreases in workforce size.

What’s holding companies back from hiring? Respondents at those companies cite uncertainty about the level of customer demand more often than any other reason, with 42 percent choosing it.3 Also, 35 percent say they’ve streamlined operations to cut positions. That choice is consistent with another finding: 39 percent of respondents say their companies’ response to the economic downturn was a permanent reduction in workforce size, and 32 percent say they’ve permanently reconfigured the geographic location of their workforces.

Finally, the results show that respondents can imagine circumstances in which their companies would significantly boost hiring or make a significant capital investment within the next year. In both cases, the most frequently chosen scenario is an unexpected opportunity to expand in a new market: 59 percent of respondents say this would prompt their companies to hire, and 49 percent say it would prompt capital investment.

Hopes for hiring

Managing public-sector productivity

Governments around the world are running up huge national debts in response to the crisis, causing concern about expenditures; one result has been significant reductions in public-sector workforces. Our surveys have reflected that over the past year, though this survey’s results indicate some degree of stability: most public-sector respondents—60 percent—expect their department to remain the same size, up from half of them a year ago. Only 11 percent expect further decreases.

Nonetheless, public-sector executives responding to this survey overwhelmingly indicate that they have felt pressed to improve their personal productivity: 45 percent say they’ve felt significant pressure, and a further 35 percent report some pressure. They also indicate that their departments have taken certain helpful managerial steps, including managing performance more effectively (chosen by 44 percent), reorganizing people or structures (41 percent), and streamlining processes (40 percent). Only 10 percent say their departments have sought to increase productivity with outsourcing or utilizing public–private partnerships.

A final note

One respondent to this survey describes the downturn’s lasting effect on his company as providing “clarity . . . that even with an excellent business model, prudence is best.” That sums up many other executives’ comments and, indeed, many of the answers to this survey. After two years, it appears that at many companies, ongoing economic uncertainty is being balanced with more rigorous planning and execution of everything from daily operations to M&A. Many companies are smaller, and, at many, morale is damaged. Nonetheless, survey respondents seem to see better times—or at least stronger financial results—ahead.