A solid majority of executives from around the world who responded to a new McKinsey survey say the recent reform of the US financial-services industry was a necessary step toward economic stability.1 There is, however, strong disagreement about the bill’s effect on the competitiveness of financial-services companies.

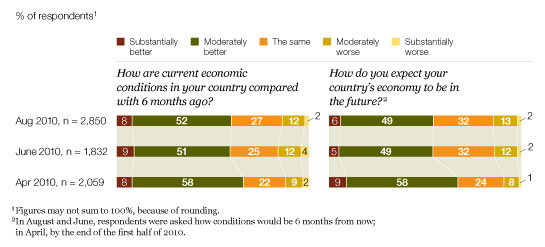

This perceived step toward stability comes during a summer of regulatory uncertainty, significant regulatory or policy changes in some major economies, and stock market volatility. Through all the uncertainty, executives’ expectations for national economies and corporate prospects at the global level have remained about the same as they were in June: more positive than negative, though less hopeful now than last spring. The most notable difference is that North American executives are now the least positive about current and future conditions.

The results show some other positive indicators. Despite ongoing uncertainty, more than half of all respondents say their companies are not postponing capital investments or M&A, underlining hope for growth at companies of all sizes. And a much smaller share of executives—12 percent compared with the 18 percent of the executives surveyed in June—expect that troubled global markets will overwhelm domestic fundamentals by year end.

Effects of financial-services reform

One of the largest uncertainties global financial institutions faced early in the summer was whether and how the US government would reform the country’s financial-services industry. The final bill, signed into law two weeks before this survey was launched, was well received by respondents overall.

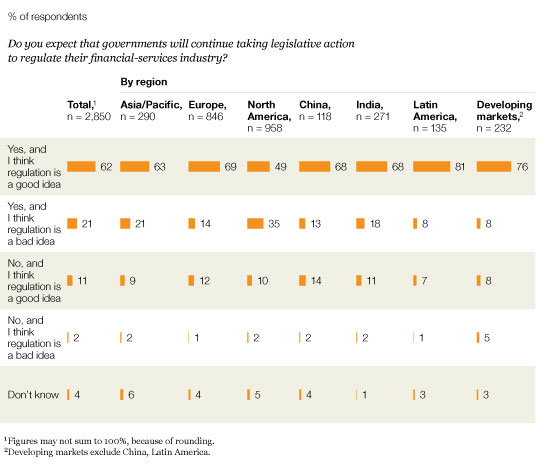

Seventy-three percent of executives outside the United States and 61 percent of executives within it say reform was a necessary step toward economic stability. More than 70 percent say additional government regulation of the financial-services industry around the world is a good idea, although 83 percent expect to see it enacted (Exhibit 1). Two-thirds of all respondents say the global economy would be less prone to crisis with a global regulatory framework. Although financial-services executives are slightly more dubious than those in other industries about the positive impact of additional regulation, more favor it than not.

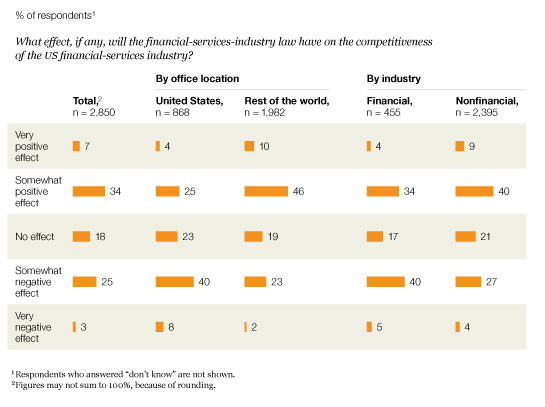

On the law itself, more respondents overall expect its impact on the competitiveness of US financial-services firms to be positive than negative. However, expectations are much less positive among respondents in the United States and in the financial-services industry globally (Exhibit 2). Most respondents say the law will have no effect on their companies’ finances. Interestingly, even 17 percent of respondents at large US financial-services firms have this opinion,2 perhaps highlighting that the law does not cover the full spectrum of companies in the industry.

More regulation?

US financial-services competitiveness

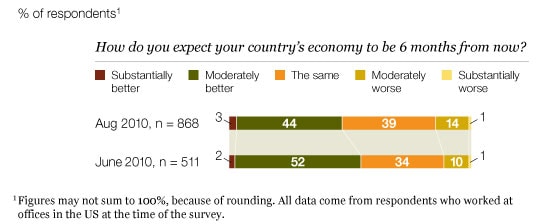

The global economy

More executives are positive than not about their countries’ economic prospects, but expectations at the global level have remained flat over the summer, after steady improvement for more than a year (Exhibit 3). The region with the greatest pessimism, however, has shifted across the Atlantic. In June, European executives were by far the most pessimistic, but, in the current survey, US executives are (Exhibit 4).

Executives’ views on the barriers to growth in their countries have moved away from immediate financial concerns. In June, lack of credit and sovereign-debt defaults were tied with the perennial issue of low consumer demand as the top barriers. Now, low demand is the barrier chosen most frequently by far, selected by 42 percent of executives around the world.3

The results also indicate that executives now see economic volatility as somewhat less likely to destabilize the global economy than it was two months ago, when concern about European sovereign debt was near its highest level. Most notably, the share who say the best description of the global economy at the end of 2010 will be “troubled global markets overwhelm domestic fundamentals” has fallen to 12 percent, from 18 percent; the most frequently chosen option is “constrained global markets perpetuate imbalances,” which has risen five points since June, to 40 percent.

A summer of stasis

The US outlook

Companies investing for the future

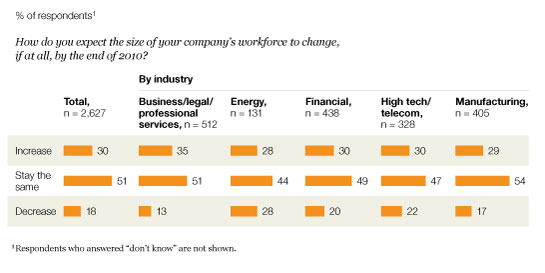

Half of all respondents expect demand for their companies’ goods or services to increase by the end of the year, and a further 40 percent expect it to be stable, with little variation among industries (and no change since June). Nearly three-quarters of respondents expect their companies’ profits to rise this year, a slim increase since June. Just under a third expect to expand their workforce, a figure that has been very slowly increasing since fall 2009 and has remained fairly stable since April of this year. Hiring expectations by industry reveal some notable variations, however (Exhibit 5).

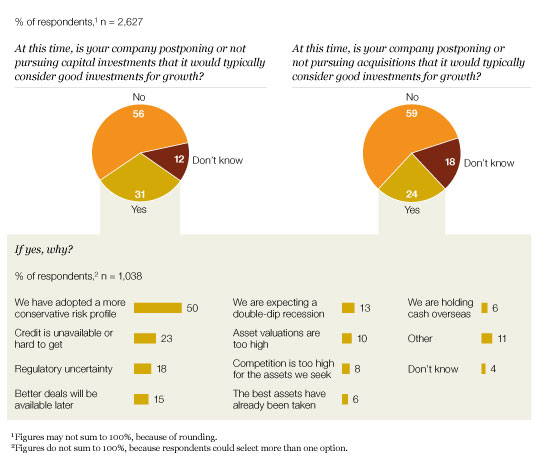

These findings are consistent with responses to a new question on investment. Economists and others have been concerned about companies not investing in growth because of regulatory uncertainty or a lack of funds. This survey offers some reassurance: a majority of companies are not currently forgoing or postponing good opportunities to make capital investments or pursue M&A (Exhibit 6). However, half of those whose companies are postponing or not making investments say it’s because their organizations have adopted a more conservative risk profile. Interestingly, while executives at companies headquartered in China are slightly more likely than those elsewhere to say they are postponing capital investments, more say they’re investing than not. And among respondents in China whose companies are postponing deals, the reasons are different—they are half as likely as others to report adopting a more conservative risk profile and more than twice as likely to expect better deals down the road.

Workforce changes

Capital investments, M&A move forward