Despite great uncertainty about the effects of the new US health care law on company finances and employee benefits, a majority of executives in the United States personally think reform was a good idea, according to the latest McKinsey survey, which was in the field just two weeks after the bill was signed.1 Moreover, among executives based outside the United States, 75 percent think reform was a good idea and only 5 percent think the new law will weaken the competitive position of non-US companies with a significant proportion of employees in the United States.

The results also show that while companies will continue to rein in operating costs, they are also planning a range of bold steps in the next 12 months to take advantage of improved economic conditions. Although the top priority on CEOs’ agendas for 2010 is stabilizing company finances, more companies will focus on increasing productivity and introducing new products or services than on reducing costs. Further, 42 percent of executives now expect their companies will hire at some point this year, up from 29 percent just two months ago.

On the question of the outlook for the global economy, executives remain wary but hopeful of a shift toward increased stability over the next three months. When asked about the scenario most likely to describe the global economy in the near future, just 36 percent pick “constrained global markets perpetuate imbalances,” down from the 46 percent who selected this choice only two months ago. In addition, a more optimistic scenario—“stable fundamentals underpin global economic outlook”—is gaining traction quickly.

How executives view US health care reform

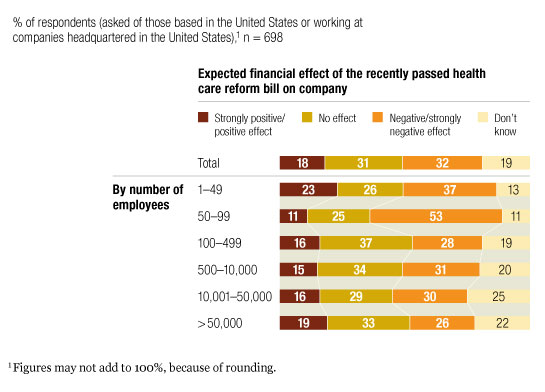

Among executives either in the United States or working at companies headquartered in the United States, 63 percent believe health care reform is a good idea. However, they don’t have a clear picture of how the new law will affect their companies’ finances or the benefits offered to employees (Exhibit 1). Nearly half think reform will have either a positive financial effect or no effect at all. However, 32 percent expect a negative impact on their companies’ finances, and 19 percent—a surprisingly high share—don’t know what to expect.

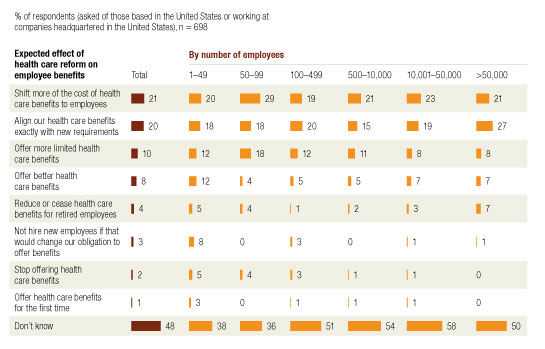

When it comes to employee benefits, the uncertainty is more acute (Exhibit 2). Forty-eight percent of executives don’t yet know how reform will affect the benefits their companies offer employees. Among the 52 percent expecting changes, 21 percent say their companies will shift more of the cost of health care benefits to employees; another 20 percent expect to align health care benefits exactly as required by law. Only 3 percent of the executives that expect changes say their companies will not hire employees if the new law changes their employee benefit obligations. However, the proportion, albeit small, rises to 8 percent among respondents at companies with less than 50 employees, the point at which many new regulations take effect. At the same time, executives at the smallest companies are nearly twice as likely as those at their larger counterparts to offer better benefits as a result of the new law.

What effect?

Uncertainty around benefits

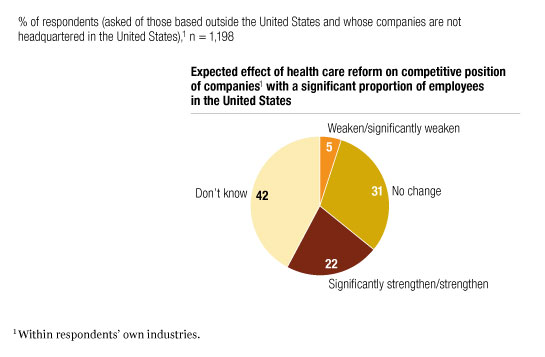

The perspective of executives based outside the United States is uncertain as well—but leaning toward a positive view of the law’s impact: 75 percent agree with their colleagues in the United States that reform was a good idea, but 19 percent aren’t sure. Fifty-three percent say the competitive position of companies with a significant proportion of employees in the United States will be strengthened or remain the same as a result of the new law (Exhibit 3).

Impact on competitive position?

Cautiously proactive in an improving economy

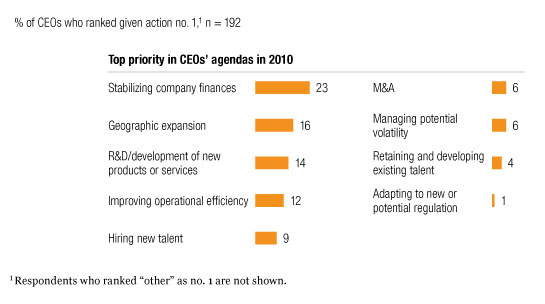

Executives are preparing to take advantage of better economic conditions in 2010 as company and country prospects improve. The priority that is ranked number one by more CEOs than any other is to stabilize their companies’ finances, followed by priorities that emphasize growth, such as geographic expansion and the development of new products and services (Exhibit 4). Objectives such as managing volatility and adapting to new or potential regulation don’t appear as close to the top of CEOs’ agendas.

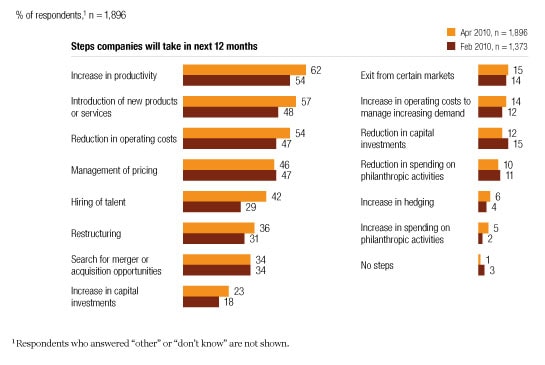

Although executives see low demand as the biggest risk to growth in the next 12 months, fully 60 percent expect demand from their own customers to increase during the same time period. Accordingly, over the next 12 months, executives expect their companies to capitalize on greater consumption by increasing productivity and introducing new products or services to gain market share from weakened competitors—strategies that have gained prominence since the beginning of 2010 (Exhibit 5). Notably, 42 percent of executives expect to hire sometime this year (up from 29 percent two months ago).

Top priorities in 2010

Taking bold steps

However, as indicated by their focus on stabilizing finances, executives remain cautious in the near term: a notably smaller 31 percent expect to increase their workforces in the first half of 2010.

Hopeful about country prospects and the global economy

Two-thirds of respondents rate economic conditions in their countries as better now than they were six months ago; and another two-thirds expect more improvement by the end of the first half of 2010. In addition, more than 80 percent of respondents think their countries’ GDPs will increase in 2010—the highest proportion since January 2009.

At the global level, most executives (36 percent) say the likeliest description of the global economy in the near future is “constrained global markets perpetuate imbalances.” However, the percentage of respondents who rank this scenario number one is down ten percentage points from two months ago, while “stable fundamentals underpin global economic outlook” is gaining traction, up eight percentage points (to 28 percent), indicating that respondents expect a shift toward increased stability by the end of the first half of 2010. This scenario anticipates strong growth in emerging markets, modest growth in corporate revenues, and weak consumption in developed markets until income and job growth recover—which, the results indicate, may happen in the second half of the year as executives begin to capitalize on improved economic conditions.

Encouragingly, 42 percent of the respondents say an upturn has already begun, and 60 percent see signs of economic improvement in their daily activities at home and work. Respondents cite improvement in economic indicators such as rising consumption and salary increases, as well as perceptions of colleagues taking more time off, friends being more likely to get or change jobs, restaurants and stores being busier, and the “phone ringing with new work.”