Over the past three months, executives around the world have grown more pessimistic about their nations’ economies: compared with three months ago, a smaller share say their economies improved over the past six months, and slightly more expect worsening conditions over the rest of 2011, according to our most recent survey.1 At the same time, executives seem to be more intently focused on economic fundamentals and are far less worried about geopolitical instability damaging the economy than they were in March.

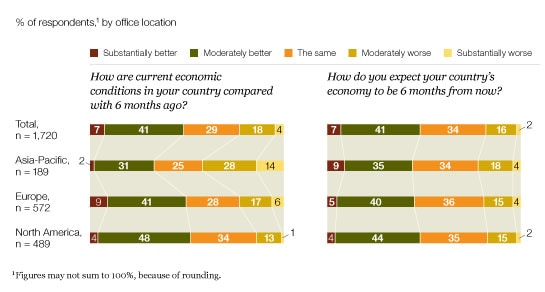

Notably, the share of executives in Europe who see improvement has fallen very little compared with the drops among those in North America and the developed countries of Asia,2 even though the eurozone has been under much-publicized pressure throughout the spring because of Greece’s financial problems. Indeed, 57 percent of all respondents say it’s at least somewhat likely that the eurozone will splinter within the next two years.

However, pessimism about economic conditions hasn't spread to executives’ expectations for their companies. On the whole, expectations for hiring, profit, and customer demand remain positive and stable compared with three and six months ago. The contrast between lower economic expectations and solid corporate expectations is particularly notable among respondents in the developed economies of Asia.

Different regions, different problems

Globally, executives are less positive about economic conditions in their countries than they were three months ago; the drops are most noticeable among executives in North America, where the share who say things are better has fallen from 72 percent to 52 percent, and in the developed countries of Asia, from 54 percent to 33 percent (Exhibit 1). Similarly, the shares of executives in these regions who expect conditions to get worse, though they are small, have risen. No doubt, some of the declining optimism is a reaction to the earthquake and tsunami that hit Japan in March; responses to the March survey were almost entirely collected before those events, so they did not meaningfully affect the data. Nevertheless, the regional differences—in particular, the relatively optimistic findings among executives in Europe—are striking.

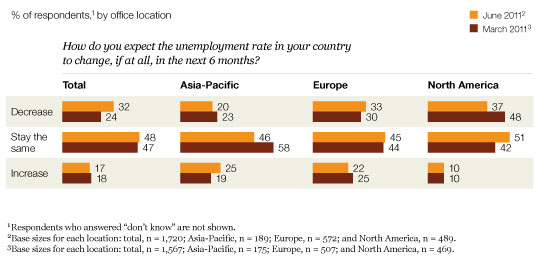

The economic indicator where executives in these three regions differ most is expectations for their countries’ unemployment rates. In developed Asia, the share of executives expecting unemployment to increase has risen six percentage points (Exhibit 2). In North America, although a stable 10 percent expect higher unemployment, the share expecting a decrease is much smaller (at 37 percent) than it was in March (48 percent).3

Current conditions decline

Divided over unemployment

Overall expectations on inflation also have fallen slightly: in March, 73 percent globally were expecting an increase this year, versus only 69 percent in June. However, this forecast is unlikely to explain the regional differences in optimism, since the views of executives in Asia and North America diverge in their general expectations for the economy. The share that expect increased inflation has fallen most markedly among executives in Asia, from 74 percent to 60 percent, with much smaller, similar drops among respondents in both Europe and North America.

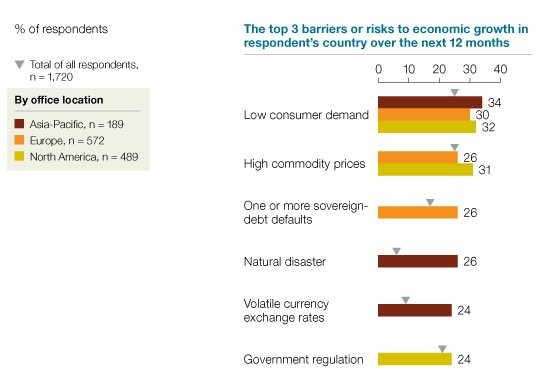

Despite ongoing upheaval in North Africa and the Middle East, executives are less concerned about geopolitical instability as a barrier to growth than they were three months ago. There are, however, notable regional differences among the most-cited concerns (Exhibit 3). Though executives in Europe are more concerned about a sovereign-debt default than those in any other region, they are marginally less likely to expect the eurozone to splinter: 36 percent of them say splintering is not at all likely within the next two years, while just about a third of executives in North America and the developed countries of Asia say the same.

Barriers tied to geography

Regional differences among companies

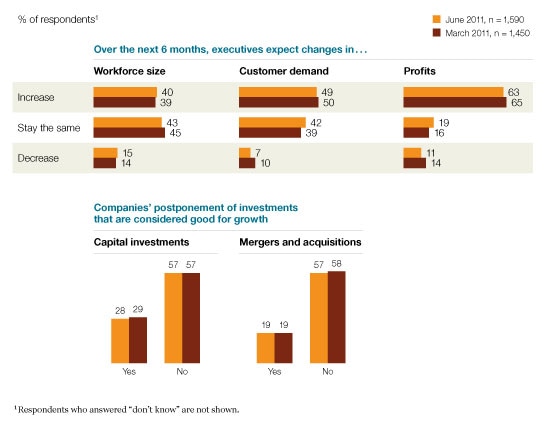

Overall, executives’ expectations for their companies’ workforce size, customer demand, and profit, as well as their companies’ take-up of investment opportunities, have barely shifted since March (Exhibit 4).

The global stability masks some distinct regional changes. Among executives in Asia’s developed countries, the share who expect an increase in customer demand has risen from 48 percent to 58 percent since March. Also, the share of these executives who expect to decrease their workforces is up from 4 percent in March to 14 percent now. Both factors suggest why 68 percent of these executives expect a rise in profits in the second half of this year, compared with 63 percent globally. The expectations of executives in North America have shifted in a similar direction, though not as strongly, and 63 percent of them expect higher profits. A smaller share of executives in Europe expect changes in demand or workforce size, and just 58 percent of respondents there expect higher profits.

Furthermore, and notably, executives in Asia report slightly less appetite for capital investment than they did three months ago: 22 percent say their companies are postponing or deciding not to pursue capital investments they would typically consider good for growth, compared with 15 percent in March.4

A stable company outlook

Though hiring expectations remain tepid globally, 37 percent of all respondents—and nearly half of respondents in China, India, and other developing markets—say their companies have had job openings they couldn’t fill for six months or more. Sixty-nine percent of all respondents say there are some positions for which it is particularly difficult to find qualified applicants. Across regions, the positions most often cited as difficult to fill are managers and technical employees. The reasons why differ: executives in developed economies most often cite insufficient experience or too few applicants, while those in emerging economies cite high wage expectations and insufficient educational qualifications more often than their counterparts elsewhere.