Our latest survey offers insight into how executives perceive the growing market influence of emerging economies, a topic that has received much attention as the world economy emerges from recession. Strong majorities of respondents expect Brazil, China, and India to become more influential over the next five years, while more expect the influence of the United States, the Eurozone, and Japan to decrease than to increase or even remain the same.1 Nearly three-quarters of those who expect any profit or revenue from emerging markets expect the share to increase. And 61 percent say governments should make it easier for companies to invest or do business in their countries—a share that skews higher among respondents in most developing economies.

In the shorter term, respondents are a little more positive on the state of their nations’ economies than they were three months ago, with just over half now saying conditions have improved and 63 percent saying their countries are now in recovery. They are a little less positive about the near future, though: two-thirds expect inflation to rise in 2011, and concern about sovereign-debt defaults and exchange rate volatility has risen sharply in the past three months, no doubt in response to the ongoing turmoil in the Eurozone. Perhaps also in response to that turmoil, the share of executives expecting an upturn in 2011 has fallen to a quarter, from 35 percent in September.

At the corporate level, expectations for profits and consumer demand to rise or stabilize inched upward in the past three months, and most respondents say their companies aren’t postponing investments for growth. Just under half say their companies have gotten external funding over the past six months, and there are glimmers of good news on the availability of credit.

Emerging influence

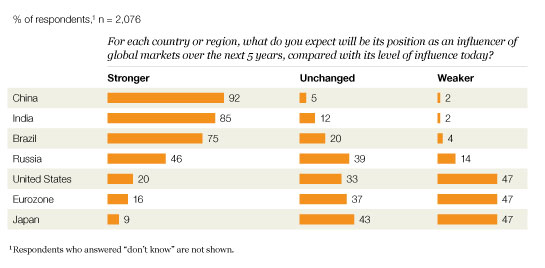

More than three-quarters of all respondents expect Brazil, China, and India to gain influence over global markets during the next five years, and more expect Russia’s influence to increase than the shares of those who expect it to stay the same or decrease (Exhibit 1). Respondents clearly expect this increased influence to come at the expense of the developed economies. What’s most notable about these findings is that, although there are differences of degree, the overall perspective is remarkably stable across executives in all regions.

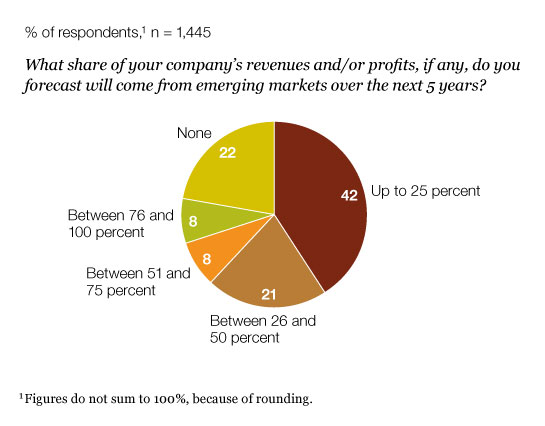

One likely reason that executives expect these markets’ influence to increase is that most expect their own profits and revenues from emerging markets to increase. Among those who answered the question,2 37 percent expect more than a quarter of their profits or revenues to come from emerging markets over the next five years (Exhibit 2). Furthermore, among all executives who expect their companies to see profit or revenue from emerging economies, 72 percent expect the share to increase over that same period.

High expectations for BRIC

Emerging-market growth

It is notable, though, that among respondents at companies headquartered in developed economies—those who have more to gain from emerging markets’ relatively fast growth—23 percent expect no profit or revenue from them.

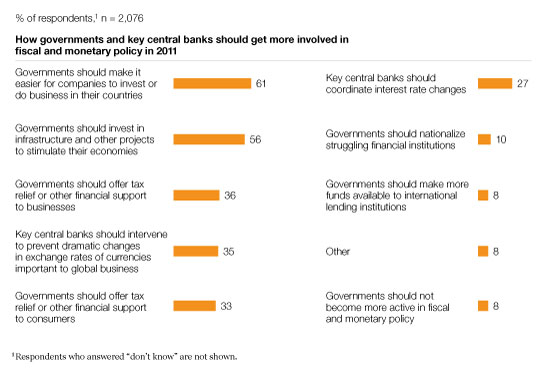

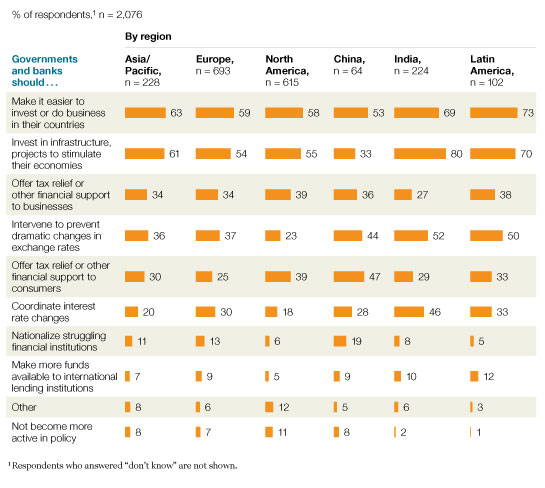

This survey also asked how, if at all, governments should become more active in fiscal and monetary policy over the next year, a question we last asked in November 2008 (Exhibit 3a). The biggest change is a notable rise in the share of respondents saying governments should make it easier to do business or invest in their countries, from 42 percent two years ago up to 61 percent now.3 There are also some interesting regional variations, and respondents in emerging markets are, for the most part, even likelier to choose this option than others (Exhibit 3b).

A call to action

A call to action

How individual countries are doing

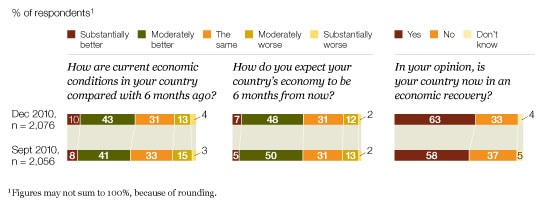

Compared with three months ago, slightly higher shares of respondents say that current economic conditions have improved in their countries and that their countries are in recovery (Exhibit 4). Despite that bump up, the same share as in September expects better conditions six months from now.

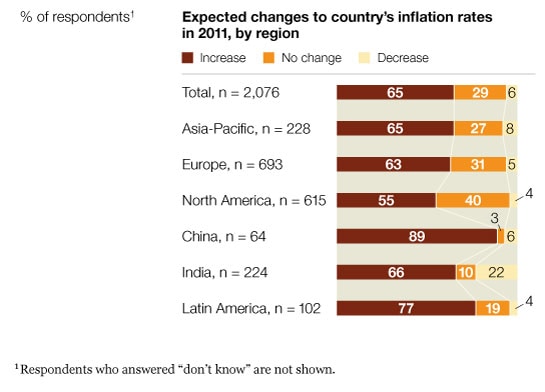

That relatively low share may reflect concern about inflation and interest rates. Nearly two-thirds expect inflation to increase in their countries in 2011; that share rises to 89 percent among respondents in China (Exhibit 5). The findings are similar on interest rates, though slightly lower: 59 percent of all respondents expect a rise and slightly more (35 percent) expect no change.

A similar outlook

Inflation anxiety

Low consumer demand remains the most frequently cited barrier to national economic growth, as it has for more than a year, with a third of this survey’s respondents choosing it. However, this survey’s results also seem to reflect the recent turmoil in the Eurozone: compared with September, the share identifying sovereign-debt default or volatile currency exchange rates as one of the biggest barriers to growth has risen 9 percentage points, to 19 percent, in each case.

Respondents are also a bit gloomier on the overall prospects for an economic upturn. In September, 35 percent expected an upturn sometime in 2011, compared with only 26 percent now. And a third, up from 21 percent, expect an upturn to happen later than the end of next year.4

Companies cautiously investing

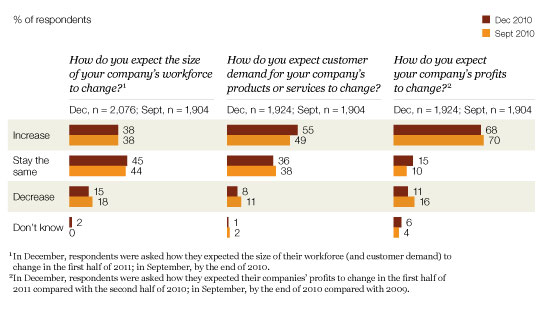

Executives’ expectations for workforce size are the same as they were in September, but their expectations for consumer demand and corporate profits have inched up or stabilized (Exhibit 6).

Executives’ concern about volatile exchange rates at the national level is reflected at the corporate level: 45 percent of all respondents expect exchange rates to affect their profits, with 17 percent expecting an increase and 28 percent a decrease. It’s notable that the share of executives in China expecting an effect is higher than that of any other country, and that the shares expecting an increase and a decrease are almost identical, at 31 percent and 34 percent, respectively. Two-thirds of all respondents expecting a change in profit due to currency fluctuations say their companies have factored that concern into their strategic planning.

Companies are also making other strategic moves. Majorities of respondents say their companies are not postponing or failing to pursue capital investments (55 percent) or M&A (54 percent) that they would typically consider good for growth.5 Executives in the energy and manufacturing industries are the likeliest to say this, with nearly two-thirds of respondents in each industry saying they aren’t postponing capital investments and nearly as many saying the same for M&A.

Even among those whose companies are postponing investment, there is some good news about credit. Though adopting a more conservative risk profile remains by far the most frequently cited reason for not investing, far fewer than in September say they’re postponing because credit is unavailable or hard to get: the share making this choice has fallen from 30 percent in September to 22 percent among those not making capital investments and to only 16 percent among those not pursuing M&A.

Holding steady

That positive trend is bolstered by other results: 44 percent of executives say their companies have obtained funding in the past six months. Among them, two-thirds say one source of funds was existing or new credit lines. However, half of all respondents expect an increase in their cost of capital in 2011—35 percent expect no change, and 7 percent a decrease.6