The past few months brought an unprecedented level of disruption to China’s biopharma ecosystem. Through my interactions with senior executives at leading multinationals and Chinese biotech companies, as well as discussions with my colleagues and other trusted market experts, I developed a few perspectives on the impact of the COVID-19 crisis, and on what the future implications might be. These views are certainly bound to evolve, as we deepen our understanding of the virus and of its aftermath. As always, I welcome feedback and debate.

Let’s focus first on how the biopharma ecosystem reacted to and was impacted by the COVID-19 crisis. Numbers are still preliminary, but combined with facts and qualitative insights, clear trends are starting to emerge.

- Market regulators stepped up, and for example, have continued to greenlight new drug applications through the crisis. In fact, the total number of National Medical Products Administration (NMPA) applications (including applications for new innovative drugs, indication expansion, and generics) approved in the January-March 2020 period (164), was greater than during the same period in 2019 (141). Also, the NMPA continued to explore new regulatory pathways, granting the first approval for medical equipment based on Real World Evidence (Allergan’s XEN gel stent). The National Healthcare Security Administration (NHSA) and National Health Commission (NHC) issued guidance on BMI coverage guidelines for Internet+ services for chronic diseases and retail pharmacies. The government made mandatory a system of advanced appointments for visits to Class II & III hospitals, and encouraged patient flow to move to Community Health Centers, including by establishing a network of fever clinics (182 in Shanghai alone).

- Patient flow contracted, with greater changes observed in larger hospitals and cities. Early analyses suggest that outpatient numbers declined by around 60 percent in February (based on preliminary data, reported by CphMRA), as patients avoided non-critical visits to hospitals. Instead, patients found new channels to access treatment or refill prescriptions, mitigating the actual impact of patient flow contraction. Retail channels are a clear beneficiary of the trend, while internet-hospitals also benefited from an online shift and rapid changes in regulation, including pilots of reimbursement for online prescriptions. (Exhibit 1)

- From a market stand-point, the impact was moderate for biopharmaceuticals companies, with hospital sales of prescription drugs declining by 16.8 percent year-on-year at the end of February, based on a sample of 690 hospitals. Several other industries, such as automobiles or luxury goods, experienced much steeper drops in consumption, in the 70-90 percent range.Within this relatively moderate impact context for pharma, some drug categories were impacted more than others. New product launches, or requiring initiation in hospital setting, were most impacted, while well-established chronic disease brands were able to navigate changes in prescription rules (i.e., longer scripts of up to 3 months) and channels to mitigate significant impact from the crisis. Drugs linked to elective procedures or treatments were more impacted – similar to what we have seen on the MedTech side, where elective procedures dropped by 50-80 percent over the February-March time period. In short, the market for pharmaceuticals held up relatively well, and is poised to rebound rapidly as hospitals re-open.

- Overall, the mobilization and pace of action of the digital health community was nothing short of breathtaking. Companies such as Ping An Good Doctor, Tencent WeDoctor, AliHealth, Baidu or JD Health were quick to offer new and improved services on their existing platforms. Traffic shot up dramatically, including through adoption by elderly populations. Biopharma multinationals surfed that wave and generally made good use of their idle workforce capacity, with digital programs and outreach activity to engage healthcare professionals (HCPs) and patients ramping up dramatically. Biopharmacos also developed applications to help patients get access to their medications by directing them to alternative channels, for example infusion centers for patients under-going cancer treatment. Several new drugs were launched in February, at the very peak of the crisis, by exclusively leveraging online channels such as large scale webinars.In short, biopharmacos achieved in a matter of a few weeks what would otherwise have taken years to do – mobilize their organization, shift significant resources towards digital, launch new programs, and generate buy-in into the potential of digital as an effective way of engaging customers.

- In contrast to the SARS situation, the China Biopharma innovation ecosystem rapidly sprang into action, with a number of companies joining the race for effective medicines, more accurate and faster tests, and viable vaccine candidates. CanSino Biologics, a company listed in 2019 on the HKEX, moved a COVID-19 vaccine candidate to Phase II trial in record time. Two additional candidates by Sinovac and Sinopharm are now in development, indicating that China, alongside the US and EU, will very much be in the global race to introduce effective and safe vaccines .

- From a supply chain standpoint, major disruptions to the manufacturing and logistics network were avoided. Thankfully, very few manufacturing sites were located in Hubei province, the epicenter of the crisis in China. Supply chain remains an area to watch though, as hospitals and distributors could encounter cash flow challenges that prove disruptive.

- On the clinical development side, while some disruption took place – for example, with ongoing trials struggling to monitor patients or lagging in recruitment goals – the impact could also be limited to a few months of delays for read-outs and potential registration applications. Enrollment for COVID-19 related trials ramped up quickly, to the point of stretching the ability to find sufficient numbers of patients for all trials.

- Company executives in China are now turning their attention to the full “return” phase of their China operations, but also the unfolding crisis in Europe and North America. Inclusion of China in global trials means that disruption impacting those trial sites overseas will impact regulatory timelines in China. Risks to the supply chain are also rising, given the uncertainties impacting multiple critical countries in the value chain (e.g. India). Above all, acute earnings pressure at headquarters could lead to more limited capacity to invest in the Chinese market, at least in the short term.

So a lot has certainly happened in just a few months. The question really is, what does it mean in the mid-term for the development of the China biopharma market? Before the crisis, the market was on a roll. Is that still the case going forward? If you boil it down to its essence, the crisis raises 5 major questions.

- How will healthcare priorities evolve and what will be the impact on budget allocation?

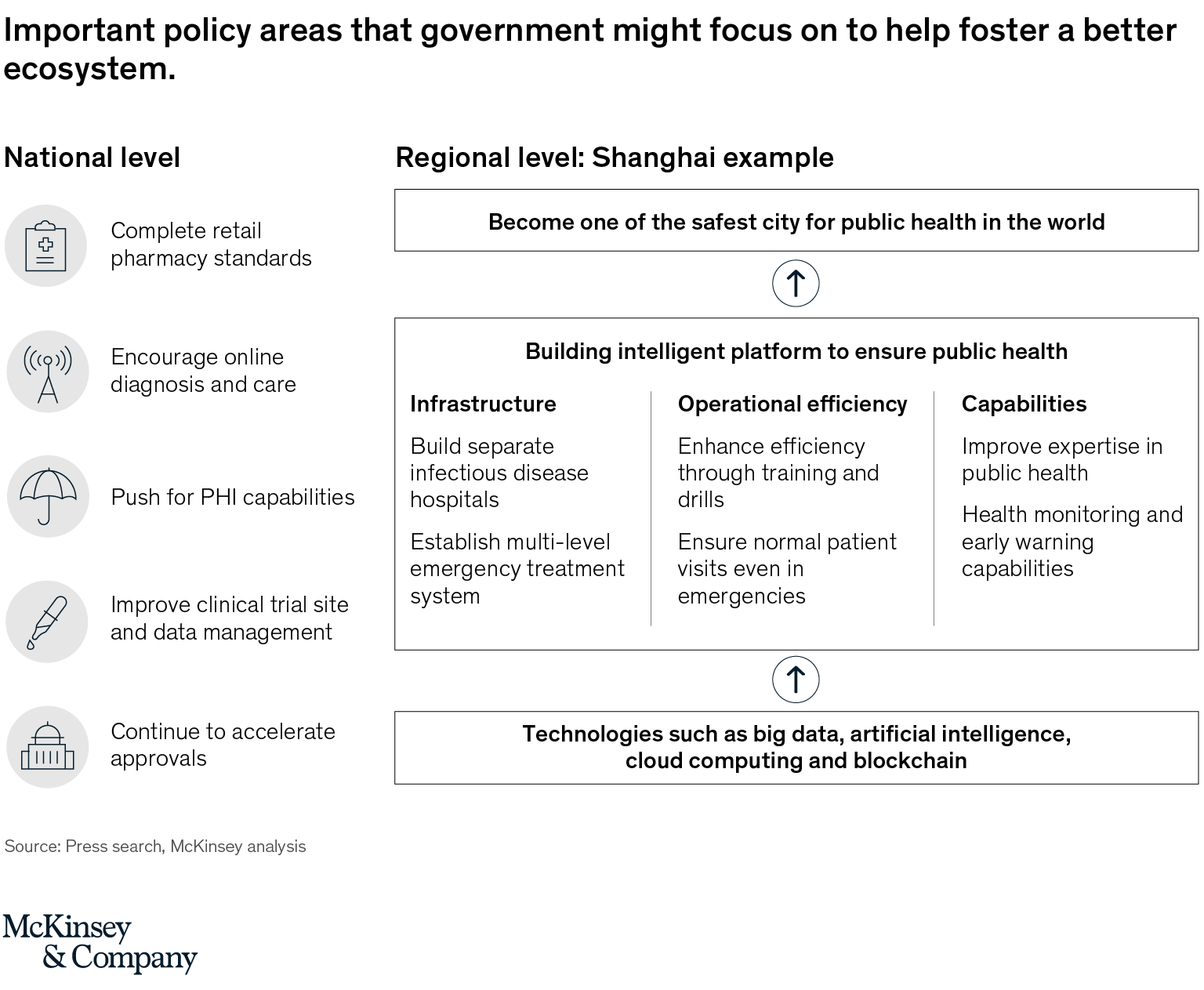

One can look back at the post-SARS years to realize that many policies adopted by the government in the 2004-2008 period found their origin in this deadly outbreak. The same dynamics will be at play here, only on a much larger scale. At central government level, we will see greater attention to public health, prevention, and development of primary care. At local government levels, leaders will pay even more attention to healthcare as a leading indicator of their performance, and they will draft ambitious blueprints for the transformation of their local healthcare system. The example of Shanghai is striking. The new draft plan released recently calls for Shanghai to become one of the safest cities for public health by 2025, supported by a range of initiatives covering infrastructure, operational efficiencies, and new capabilities, and with the goal of building an intelligent platform for public health (Exhibit 2)

Exhibit 2

More broadly, who will be the beneficiaries of the reform? A few potential priorities come to mind:

- Roll out of prevention and primary care system: This is an aspect of market development pushed since the 2008 healthcare reform, and set as a clear goal in the country’s ‘Healthy China 2030’ vision. Progress has been slowed by many factors. One would think that the acute need for a stronger primary care system, demonstrated by the crisis, will push regulators to re-affirm this direction of the system reform.

- Expansion of internet hospitals: Here again, the crisis demonstrates the important role online channels should play in creating a more efficient healthcare system. Considering the number of qualified players entering this part of the ecosystem, and the acute needs of patients resulting from the limitations of the current hospital based infrastructure, we expect the Internet hospital market to finally take off.

- Rise of private health insurance (PHI): As the government seeks to expand funding to support a more ambitious healthcare development plan for China, the role of private payors and channels will rise to complement direct public funding and reach. Technology players, such as Tencent’s WeSure, will play an important role in the design and adoption of new types of health insurance products on a large scale.

From a budget allocation perspective, we can anticipate 2020 to be a down year for healthcare. GDP is likely to show a low single-digit growth rate, if not contraction. Sources of BMI funding will be impacted as many companies struggle to stay in business, and are given exemptions to contribute to the insurance scheme. In the short term, the focus of the government could, out of necessity, shift to more stringent cost containment measures, such as a rapid roll-out of Volume Based Procurement, with waves 2 and 3 already in motion, or a tightening of negotiations during the expected annual National Reimbursement Drug List (NRDL) update. Potentially, some positive policy priorities, put in motion before COVID-19, could take a back seat to more pressing priorities. From 2021 onward, we would hope to see a rapid rebound in economic output, and the share of GDP allocated to healthcare tick upward versus the historic trajectory.

Overall, biopharma companies will need to sharpen their understanding of the evolution of funding pools – be it BMI/NRDL, self-pay, or PHI – to best position their portfolios to capture the full potential.

- Where will the patients go and how will that impact existing and new channels?

The rise of retail and internet hospitals is not a new trend. If anything, the crisis acted as a catalyst to accelerate what was already on the horizon. We can assume that momentum will persist, although more sweeping regulatory changes supporting online prescriptions and reimbursement could still take time as the government works through the challenges associated with the monitoring of that channel. Pharma MNCs are already organizing to capitalize on these trends, with some creating dedicated Internet hospital teams to design and execute new strategies. Foot traffic in large hospitals should rebound and remain a major driver of market development. Here we can look back at the trend post-SARS to see that the short-term drop in patient flow in hospitals was quickly recovered, with further growth. Mid-term, further infrastructure investment behind primary care settings, supported by policies to attract patients, will lead to a more meaningful redistribution of patient flow. Overall, biopharma MNCs and local biotechs will need to hone their coverage model of an increasingly fragmented and complex market landscape. (Exhibit 3)

Exhibit 3 - What will the new go-to-market (GTM) model look like now that ‘proof of concept’ has been established for digital?

The defining characteristic of the crisis is the rise of all things digital. All companies had been experimenting with digital pilots for some time, some more advanced and larger than others. All saw a significant boost in digital activities during the COVID-19 crisis. This included large scale webinars to engage Key Opinion Leaders (KOLs), disease education programs on a scale not seen before, all-digital new medicine launches, etc. Digital has arrived and is here to stay. Yet, offline has not yet disappeared and will continue to play an essential role. The real answer going forward will be found in the ability of biopharmacos to develop customer engagement hybrid models that build on offline and online activities to offer a true omnichannel engagement model. That’s where the battle will be won, and lost, in what promises to be a very competitive environment. Winners will develop new capabilities, differentiate their content and experience, adapt their offering to the various needs and life cycles of therapeutic areas, and critically scale what is working well, while avoiding the temptation of launching many “pilots”. (Exhibit 4)

Exhibit 4 - Will China remain an attractive market for healthcare investing, supporting the emergence of Chinese biotechs and health-techs?

The answer to that question is a resounding ‘Yes.’ In the last few weeks, since China re-opened for business, the following events took place: Qiming Ventures announced a new fund of over US$1.1 billion that will be dedicated to investment in biotech, healthtech or Medtech. Zai Lab licensed the China rights of the CD20xCD3 bispecific antibody REGN1979 from Regeneron Pharmaceutical, for an upfront payment of US$30 million. InnoCare Pharma debuted on the HKEX in March, raising US$289 million, while Akesobio’s US$330 million IPO concluded in April was Hong Kong’s largest this year. Most recently, Legend Biotech raised US$424 million through its NASDAQ IPO, while Everest Medicines completed a record US$310 million series C financing.

In other words, we went back to the heavy flow of innovation news we have become accustomed to since 2016. Through my conversations with various industry insiders, I have come to the conclusion that this flow will continue, and if anything further gain momentum. Policies supporting healthcare will accelerate, cash remains available on a large scale, and returning Chinese are continuing to bring back entrepreneurship and ideas from overseas.

- Will China’s importance to global strategy increase or decrease?

This is potentially the most complex question, with significant long-term implications, in China and beyond. It is clear that the relative importance of China to multinationals has increased the last few years. This is evident in their share of business coming out of China, their hard asset investments in the Chinese market, and external communication by CEOs and senior executives. I wrote a full blog on this just 18 months ago (https://www.linkedin.com/pulse/china-has-become-ceo-level-priority-multinational-companies-le-deu/). One could wonder if this public health crisis could slow down that process. I would argue that the dynamics at play are actually likely to re-enforce the rise of China for large biopharma players. China is the first country to get out of the crisis, and is already taking steps to bolster its healthcare sector. EU 5 markets are disproportionally impacted by the crisis, and given the state of public finances in those countries, we could anticipate a tightening of budget capacity to support healthcare, and at a minimum, further cost containment measures. Overall, China is likely to come out of this ahead, and increase the relative attractiveness of its biopharmaceuticals market for foreign industry participants.

It is still early to draw conclusions about the aftermath of COVID-19 in China given that this humanitarian and economic crisis is still unfolding globally, and that spikes in infections in China cannot yet be ruled out. Some of my specific views could age poorly. But overall, I would be very surprised if COVID-19 does not end up being looked back at as a trigger for accelerated reform of the China healthcare market, leading to greater access for patients, better healthcare outcomes, and greater opportunities for industry players.

I’m a Senior Partner with McKinsey & Company, based in China since 2005 (Shanghai and now Hong Kong). I co-lead our Pharma and Medical Products Practice in Asia Pacific. Please reach out to connect or follow me here on LinkedIn. I’m also on Twitter @fle864.