Given the chaos in the financial economy, it should come as no surprise that M&A activity fell sharply in the fourth quarter of 2008. Since 1980, US recessions have led to steep declines in the value of global M&A activity—typically, of around 50 percent during the first year. That falloff results from factors we see in the current downturn as well, including lower deal values in sinking equity markets; difficulties with financing, particularly for very large transactions; and a general fear about the economic outlook, which forces acquirers to put plans on hold. Moreover, in December 2008 stock markets were down 40 to 50 percent from their January levels. Corporate earnings expectations have been substantially lower too, and access to funds is challenging, to say the least.

The current environment is grim, and nobody knows how the M&A market will develop in the short term. The last quarter saw a sharp drop in activity, and there is still considerable uncertainty about the ability of capital markets—particularly the debt markets—to provide enough financing to support deals. We believe that over the longer term, however, the trends that emerged over the past cycle will remain important. As a result, the pattern of M&A activity in the current downturn will be quite different from that of previous cycles.

Stock markets peaked in the fourth quarter of 2007, and the world economy has been progressively slowing through 2008. But the 2008 M&A market should be seen in context: the value of announced M&A activity for the whole year reached $3.4 trillion globally, the third-highest level of all time. If 2007’s volumes now look like a departure from the trend, 2008 seems to mark a return to it rather than a complete collapse: volumes fell by 25 percent from 2007, back to levels comparable to those of 2006, the second-highest year of all time. Moreover, volumes went up significantly quarter by quarter until the slowdown in the fourth one—despite a 40 to 50 percent decline on stock markets, the collapse of expectations for corporate earnings, and limited access to funding. In the fourth quarter, a significant number of large deals, such as BHP Billiton’s bid for Rio Tinto, were withdrawn. Yet though the volume of withdrawn deals for that quarter was relatively high, for the whole year it wasn’t so—about 15 percent of deals by value, and 4 percent of deals by number for the year, versus an average 13 percent and 5 percent for deal value and deal numbers respectively since 1995. Indeed, though the cycle peaked in 2006 and 2007, just over 60 percent of the deals announced in those years were completed, versus 87 percent for the previous decade.

M&A activity got a boost in 2008 from restructuring transactions that were generated by the crisis: government-sponsored deals represented 25 percent of those in the financial-institutions sector, which accounted for 23 percent of total deal volumes in 2008. The effects of these deals were perhaps more limited than most observers think, however. The top ten transactions for financial institutions repre-sented 4.5 percent of total deal volumes in 2008, in line with the 5 percent of 2007.1 Even excluding these transactions, underlying volumes remained surprisingly healthy in 2008, and M&A proved to be resilient for the year as a whole. The question, of course, is what 2008’s activity portends for 2009.

A different kind of cycle?

During the previous M&A cycle, volumes peaked in 1999 and then fell almost by half during the following year before they hit bottom, in 2002—the cycle ended suddenly and decisively. It’s impossible to say where the M&A market will go in the short term, and nobody is anticipating a fast recovery. But when you think about the trends in the previous cycle and the market’s performance in 2008, the picture that emerges is quite different from the traditional boom-and-bust pattern of previous cycles. Certain characteristics of deal activity in the previous up cycle suggest that M&A may be more resilient and more relevant to the general economy in this downturn than in previous ones.

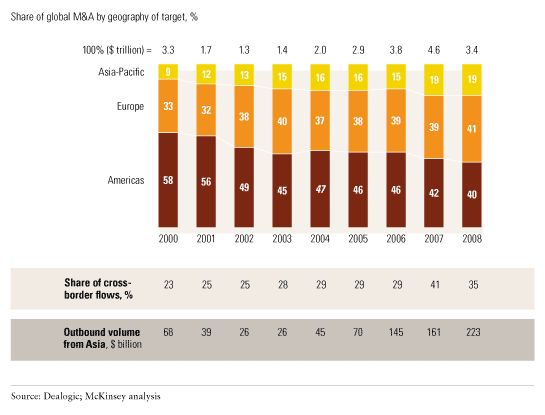

M&A is increasingly global rather than dominated by a few countries with little linkage among them (Exhibit 1). In 2000 and 2001, the United States, Europe, and Asia accounted for approx-imately 60, 30, and 10 percent of deal volumes by target, respectively. From 2005 to 2008, the distribution was much more balanced, at approximately 40, 40, and 20 percent. Cross-border M&A activity grew from 23 percent of the total in 2000 to 29 percent in 2006 and 41 percent 2007, falling back to 35 percent in 2008. Emerging markets, particularly in Asia, played an important role in this transformation; China and India together represented some 12 percent of all cross-border deals in 2008.

A global market

One defining feature of the past few years were megadeals—transactions valued at more than $10 billion—which were driven by the market’s confidence and by a trend toward greater industry concentration. In 2008, the focus of such deals changed sharply: most of them were restructurings in the financial sector (for instance, Bank of America’s acquisition of Merrill Lynch). The 37 such deals, with a value of almost $833 billion globally, represented a significant proportion of total M&A. When the economic and financial crisis subsides, megadeal activity may shift back toward large-scale transformational deals in other industries, such as energy, materials, and telecom. The 2001–02 downturn did not put many major companies in financial distress. But this coming downturn will, paving the way for a higher number of large, industry-shaping deals.

Hostile activity, peaking in 2007, became increasingly prominent as a result of very strong market confidence and extraordinary financial conditions. Surprisingly, the pace of such deals was still high in 2008: in the first three quarters of 2008, they were still running at around $50 billion a quarter, in line with the average 2000 to 2007 level, before declining to $21 billion in the fourth quarter. They were typically large—for instance, German ball bearings manufacturer Schaeffler’s $35.6 billion bid to acquire car parts manufacturer Continental.

Private equity reached unprecedented levels of activity and importance during this cycle, expanding from 4 percent of the global M&A market in 2000 to a staggering 20 percent in the first half of 2007. In part, this explosion reflected a need to deploy funds under management, which rose by 3 percent a year from 2000 to 2004 and by a whopping 33 percent a year from 2004 to 2007, so that the global buyout industry had upward of $900 billion to spend. The assets of North America’s top ten private-equity firms rose more than ten times during the past decade. Combined with easily available and cheap credit, these developments sparked a spending spree unprecedented in private equity’s history.

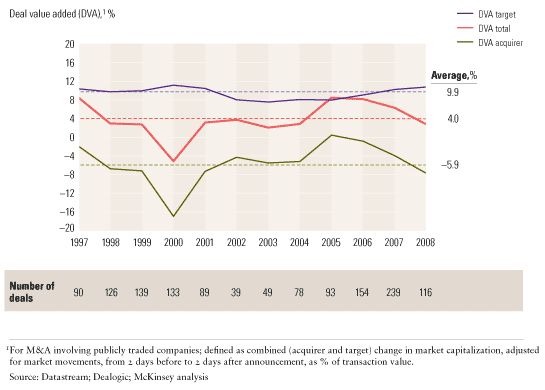

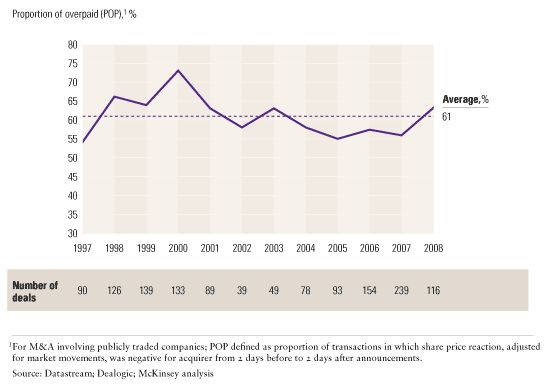

This trend came to an abrupt end in 2008 as credit markets sputtered. Overall volumes of private-equity deals fell by about 72 percent from the levels of 2007, representing about 6 percent of total M&A deal volumes. What’s more, the nature of the private-equity deals that closed changed dramatically. Since it is hard in the current climate to build consortia for club deals, private-equity involvement in megadeals screeched to an almost complete halt. In 2008, a single transaction above $10 billion was announced, only to be later withdrawn; no such megadeals were completed in 2008, compared with 9 completed in 2007 and 14 in 2006. In the absence of cheap credit, private-equity firms have found themselves restricted to deals with a much higher equity content. Often, they take minority stakes in circumstances in which they would previously have assumed control or looked at alternative asset classes, such as distressed debt. Given the large decline in private-equity activity that has already taken place, it cannot collapse much more. Most likely, it will rise once the financial crisis starts to subside.Strategic buyers, showing discipline, didn’t lose sight of value. In M&A booms, acquirers are often tempted to overpay, but not in this boom cycle: the value created by M&A increased consistently. Some worrisome signs did emerge in 2008, however. The total level of value created has started to decline, and the target is capturing a majority of it,2 despite premiums paid remaining low. In 2008, the average deal value added (DVA)—our proxy measure of the total value created for buyer and seller—had decreased from the 2007 level (6.4 percent), to 2.8 percent, which is below the long-term average of 4.0 percent (Exhibit 2).3 This decline resulted entirely from a sharp fall in the creation of value for acquirers; for targets, it even slightly increased in 2008 compared to previous years. To understand what has happened, you must look at the reaction of the market to deals—in particular, the proportion of them in which it thinks the acquirer overpaid.4 From 2004 to 2007, this figure hovered around 55 to 57 percent, below the long-term average of 61 percent. In 2008, however, it rose to 63 percent (Exhibit 3).

Trends in deal value added

The overpayers

Most of these themes are likely to persist in 2009. The events of the past year undoubtedly dealt a major blow to the confidence of many companies. Nonetheless, M&A volumes remained healthy. Companies went into this downturn with relatively strong balance sheets,5 and valuations have become much more affordable. As the slowdown progresses, good companies in many sectors will certainly come close to financial distress. The megadeals of 2006 and 2007 were ambitious acquisitions of healthy companies facilitated by cheap financing; those of 2008 were resuscitations of failing banks. Although financing conditions are now considerably more challenging, this does not spell the end of megadeals: in 2009 and 2010, there will probably be a number of well-planned takeovers of struggling industrial giants. A few have already appeared on radar screens.

The next few years will present considerable opportunities for ambitious and disciplined acquirers—and these are not in short supply, as we have seen over the past few years. Asian acquirers, less affected by the credit crisis than their counterparts in Europe and the United States, will have a stronger incentive to look for overseas acquisitions.

What will be different?

Although we see little change in the themes driving the M&A market, the way companies think about the execution of deals has already changed visibly. M&A in a rising market with easy access to capital is very different from acquisitions in a downturn, when opportunities arise and decisions must be made very quickly. The key differences fall in three specific areas.

Speed

The interval between the announcement and the closing of deals valued above $1 billion has fallen dramatically, from about 130 days (1995–2007) to about 60 in 2008.6 Companies have already started to realize that if they want to close successfully in turbulent markets, they must undertake fast, targeted due diligence on the main issues and then use reps and warranties more extensively to address minor ones.

Managing stakeholders

In today’s market, a company can’t start to negotiate deals without knowing for sure whether it will have the necessary support at the end: there is no longer much time to build an internal consensus among the board, nor can executives assume that shareholders will extend the benefit of any doubts. In particular, a company must actively establish realistic expectations for growth and profitability. Coming out of the past few years, many board members and shareholders will have unrealistic ones—the downturn is not yet reflected in future earnings estimates, and this problem will have to be managed to frame external growth moves correctly.7 It is likely that we will see a greater proportion of deals financed by equity, due to the economic uncertainties: this will make solid investor and board support even more important.

Opportunity scanning

The best opportunities in a downturn are often good pieces of a distressed portfolio forced into a fire sale. Success in this environment will depend on choosing the right targets to stalk: these will be very different from the sorts of deals business-development teams have considered during the past few years. Now is the right time to put aside conventional thinking about M&A and take a fresh look at your industry: do not assume that any company will simply be “not for sale” over the next few years. Which companies will experience difficulty? Which parts of which businesses would tempt you? How can you put together creative deals that will snare them?