Optimism is on the rise that a solid economic recovery is taking hold around the world, but the cost cutting so prevalent during the recent recession looks to remain a strategic priority for some time. Indeed, the number of executives reporting steps to reduce operating costs in the next 12 months increased significantly between February and April, even as confidence in the economy grew.1 Yet any successes companies have at cutting costs during the downturn will erode with time.

Many executives expect some proportion of the costs cut during the recent recession to return within 12 to 18 months2 —and prior research found that only 10 percent of cost reduction programs show sustained results three years later.3

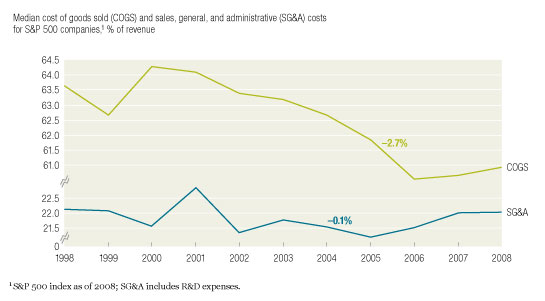

On either schedule, any programs initiated in the early months of the downturn are already beginning to fail—just as savings would be most useful to finance growth. Sales, general, and administrative (SG&A) costs prove to be particularly intransigent. While manufacturing efficiencies have enabled an average S&P 500 company to reduce the cost of goods sold (COGS) by about 250 basis points over the past decade, SG&A costs have remained at about the same level (Exhibit 1).

Intransigent costs

Why is it so difficult to make cost cuts stick? In most cases, it’s because reduction programs don’t address the true drivers of costs or are simply too difficult to maintain over time. Sometimes, managers lack deep enough insight into their own operations to set useful cost reduction targets. In the midst of a crisis, they look for easily available benchmarks, such as what similar companies have accomplished, rather than taking the time to conduct a bottom-up examination of which costs can—and should—be cut. In other cases, individual business unit heads try to meet targets with draconian measures that are unrealistic over the long term, such as across-the-board cuts that don’t differentiate between those that add value or destroy it. In still others, managers use inaccurate or incomplete data to track costs, thus missing important opportunities and confounding efforts to ensure accountability.

While there’s no single silver bullet to ensure that cost-management programs will stick, large, multibusiness unit organizations can better their chances by improving accountability, focusing on how they cut costs, drawing an explicit connection to strategy, and treating cost reductions as an ongoing exercise.

Assign accountability at the right level

Few would dispute that the support of top executives is necessary for cost-management efforts to succeed. Involved CEOs and CFOs, in particular, can help mediate the inherently political nature of such exercises and provide critical energy and motivation. Yet in our experience, the involvement of top managers is not by itself sufficient—especially in a period of growth, when they naturally turn their attention to other initiatives.

Instead, most cost innovation happens at a very small and practical level. Breaking costs out in this way helps managers to find the specific groups or individuals responsible for them and to identify and swiftly deal with pockets of expense mismanagement. Take, for example, the cost-cutting program at one multinational high-tech company. Initially, the CFO had little actionable information on who was responsible for which costs. Profit-and-loss (P&L) statements were reported only for product-based business units, even though geographic sales units had higher costs. This lack of detail made it very difficult to assign responsibility for overall cost reductions. For instance, if freight costs for a business unit increased from year to year, it was difficult to determine whether this happened because of shipping behavior by factories or costs incurred by the sales organization in delivering third-party parts to customers.

To resolve these issues, the company redefined the way it collected and reported information, to ensure that costs were broken out for each of 100 organizational units. That helped managers quickly identify two headquarters units and a sales organization that were responsible for large cost increases. Together, the managers came up with a plan to control future costs. Among other things, the plan assigned cost accountability to the company’s more than 60 separate organizational units. This approach ensured that the people managing costs were those closest to the decisions, who could ensure that cost management was not hurting the business.

Importantly, the process planners who run such programs as Six Sigma improvement efforts are generally the wrong choice to manage cost-cutting programs. Typically, they lack both the content expertise and the authority to make difficult trade-offs in areas that often require more detailed knowledge of where costs occur and the ability to make keen subjective judgments about which costs to cut. Only someone at the level of, say, a sales manager has the detailed knowledge and authority to decide whether it’s really necessary to travel to one client meeting in person, while conducting another by videoconference. Such informed cuts are more likely to endure because the people responsible for them can be held accountable through appropriate incentives, such as performance evaluations, that consider both costs and business performance.

Focus on how to cut, not just how much

Cost reduction programs often lose effectiveness over time because top management kicks off the effort with broad cost reduction targets (“How much do we want to save?”) but then leaves decisions on how to meet those targets to individual line managers. The presumption is that they have a more detailed understanding of their particular area of the business and will take the right actions to control costs. While this is true in some instances, we have seen too many cases where managing to a number has resulted in flawed decisions, such as delaying critical investments, shifting costs from one accounting category to another, or even cutting costs in a way that directly undermines revenue generation. Clearly, the benefits of such cost cuts are likely to be illusory, short lived, and at times damaging to long-term value creation.

A more enduring approach includes changing the way people think about costs by, for example, setting new policies and procedures and then modeling the desired behavior. If a company announces, say, a new travel policy, senior managers need to set the tone with their own actions—for example, by aggressively using videoconferences instead of travel or eliminating catering for in-person meetings. Even something as simple as no longer providing sandwiches for lunch meetings can be part of a pattern of behavior that signals real and enduring change. And since backpedaling on this kind of behavior when the economy picks up again would send the reverse message, managers should model only cost cuts they intend to stick with. If they know they’ll eventually restore catering for in-person meetings, it could well be better not to cut it in the first place.

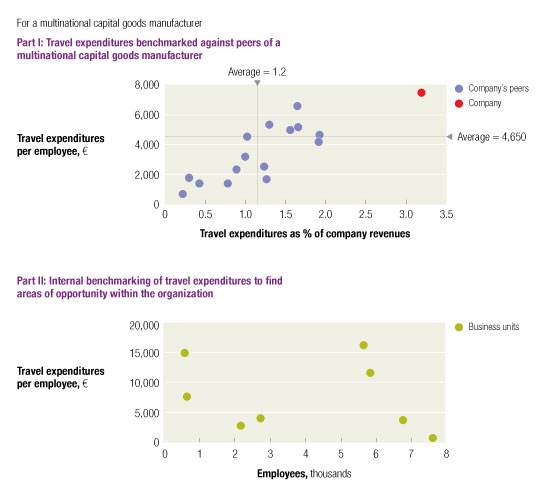

Benchmarks matter. External ones on some measures may be difficult to get, but where they are available—for example, on travel expenses—they can enable managers to compare performance across different units and identify real differences, as well as trade-offs that may not be in line with the organization’s overall strategy. Internal benchmarks are easier to access and provide great insights, especially because managers are more likely to understand and adjust for differences among their company’s organizational units than among different companies represented by external benchmarks.

One multinational capital goods manufacturer combined the two perspectives, analyzing the major categories of expenditure and developing targets based on both internal and external benchmarks. Using external ones for travel spending, managers found that the company’s travel costs were higher than those of any peer—both per employee and as a percentage of revenue (Exhibit 2). They then set an aggressive target to reduce travel expenses—and, to make the effort stick, instituted new travel policies on booking hotels and airfares. By examining internal benchmarks across suborganizations (such as departments, business units, or locations), managers also identified which executives needed to better educate their organizations on travel policy. In addition, they increased accountability by tracking each unit’s performance on a monthly basis to measure compliance and encouraged underperforming divisions to manage their travel costs more aggressively. The effort changed travel behavior across the entire organization as subunits shared best practices.

Benchmarking costs

Don’t let P&L accounting data get in the way of cost reduction

CFOs often manage cost reduction efforts by tracking accounting data in their companies’ P&L statements. These can be a useful starting point in a crisis, if other data are unavailable. But over the long term, P&L categories, such as overall SG&A costs, don’t give the kind of per-unit insights that help focus cuts in, say, travel expenses on the units that can best afford to cut them.

Unfortunately, few companies have the kinds of systems they need to track costs at a fine-grained level—and they face a number of challenges in establishing them. Multiple data systems may make it difficult to aggregate and compare data from different geographies. Inconsistent accounting practices between businesses or time periods may lead to significant distortions. Changes in organizational structure (as a result of acquisitions, divestitures, or even changes in the allocation of overhead costs) may similarly distort tracking. Finally, one-time expenses in either the baseline or the tracking period may become excuses for deviations from the plan. As a result, business or functional managers often use data issues to divert attention from their lack of progress.

Indeed, one medical-product company experienced all these issues simultaneously in the initial stages of its cost transformation program. Business unit heads objected that tracking numbers from the central financial database were flawed because of a range of factors.4 As a result, the company couldn’t reduce costs during the first several months of its program, and discussions focused on the integrity of the data rather than potential initiatives.

To resolve the problem, companies must continuously track, in some detail, the expenses behind the P&L to identify areas of underperformance, without worrying about the formal accounting of the costs. Identifying, measuring, and controlling their most important drivers is more important than how the savings are booked and reported. To manage costs at the necessary level of detail, the CFO of the company above gave each business unit head and controller full access to a centralized cost database linked to the official P&L. Each controller received a standardized template to record any adjustments affecting the baseline, along with exact amounts, periods, and offsetting adjustments. The CFO then aggregated the data into a simple cost-tracking report that he shared with all involved.

After two months, the increased transparency eliminated all data disputes—and the organization met its full-year cost reduction target in just six months. Two by-products were increased standardization of internal accounting and a dramatic reduction in several cost categories bucketed under “other costs.” By getting the data right and moving quickly beyond questions about data integrity, the organization significantly simplified the effort of cost reporting, making it much easier to maintain the cost program over time.

Clearly articulate the link between cost management and strategy

Strategy must lead cost-cutting efforts, not vice versa. The goal cannot be merely to meet a bottom-line target. Indeed, among participants in a November 2009 survey, those who worked for companies that took an across-the-board approach to cost cutting in the recent downturn doubt that the cuts are sustainable. Those who predicted that the cuts could be sustained over the next 18 months were more likely to say that their companies chose a targeted approach.5

Yet in our observation, many companies do not explicitly link cost reduction initiatives to broader strategic plans. As a result, reduction targets are set so that each business unit does “its fair share”—which starves high-performing units of the resources needed for valuable growth investments while generating only meager improvements at poorly performing units. Moreover, initiatives in one area of a business often have unintended negative consequences for the company as a whole. For example, a global low-tech medical-device company’s initiatives to reduce manufacturing and product costs were led at the plant level, without input or customer insights from sales and marketing teams. The leaders of the cost-cutting effort in manufacturing nearly rendered several products defective because they did not know how customers used the products. Consequently, the effort led to the loss of accounts and market share.

To create value through cost cutting, managers need to understand the best ways to allocate operating expenses, such as selling costs and R&D. To do so, they must understand, at the most detailed possible level, the return on invested capital (ROIC) and the growth of the markets in which a company plays. Mapping costs against business units and geographies will reveal both opportunities for cost reductions and areas in which the business should increase its investments to take advantage of growth opportunities or to “double down” in high-ROIC businesses. At a high-tech company, for example, the granular mapping of R&D spending by product families identified some that despite their aging technological and growth profiles were still receiving R&D and marketing investments. Clearly, these low-ROIC businesses did not warrant a high level of new resources. Management could redirect them to growth units because it was able to map costs at a very granular level.

With such insights, managers will also be able to deliver a consistent message on how cost reductions would make a company stronger—a message reducing short-term resistance and even inspiring the organization to support the effort. Moreover, once these practices are baked into the company’s standard operating practices, cost reductions will become a more enduring part of its strategy for long-term health.

Treat cost management as an ongoing exercise

Most companies treat cost management as a one-off exercise driven by the need to manage short-term profit targets—and some of these exercises do succeed in the short term because of constant pressure from the CEO or CFO. Yet such hasty cost-cutting activity typically goes into reverse once the pressure is removed and rarely results in sustainable changes in cost structure. In our experience, the reason is that one-off exercises don’t require internal capability building.

A better approach is to use the initial cost reduction program as an opportunity to build a competency in cost management rather than in mere cost reduction. Cost-management programs need to be scoped as two- to three-year initiatives rather than as immediate-term efforts with one-year horizons. Also, effective cost-management programs, by their very nature, include plans for dealing with changing business conditions—for instance, by adjusting for activity-level changes, competitive drivers, or both.

In the case of the multinational manufacturing company, many of the processes introduced as part of the cost reduction initiative became the basis for ongoing cost management. The finance and accounting group created a system for monitoring costs at a detailed and accurate level, where none had existed before. Managers encouraged greater communication between finance and accounting, the business units, and functional groups such as IT. Better communication uncovered inconsistencies in accounting practices. Changes in performance-management systems and incentives further promoted the cost-management approach. Purchasing managers found clear areas of waste that could be sustainably removed from the cost base. Toward the end of the third fiscal quarter of the effort, detailed plans for building upon and sustaining the initiative through the next fiscal year were developed and vetted. These plans and practices enabled the company to manage costs in the long term.

Companies must improve their processes and capabilities if they hope to reduce or contain costs in a sustainable manner. Rethinking common practices in cost management should help to realize this goal. In particular, achieving a more fine-grained perspective on where costs occur should be a centerpiece of any successful cost-management program.

Related Articles

A better way to cut costs