During tough times—and they haven’t been this tough for generations—directors are supposed to ask difficult questions about their companies. Yet they rarely ask hard questions about themselves, such as, “Are we the right people, asking the right questions, providing the right sort of leadership, challenging management in the most productive ways?” What’s more, except in the banking world, boards haven’t had to take the blame for practices they should have corrected early on.

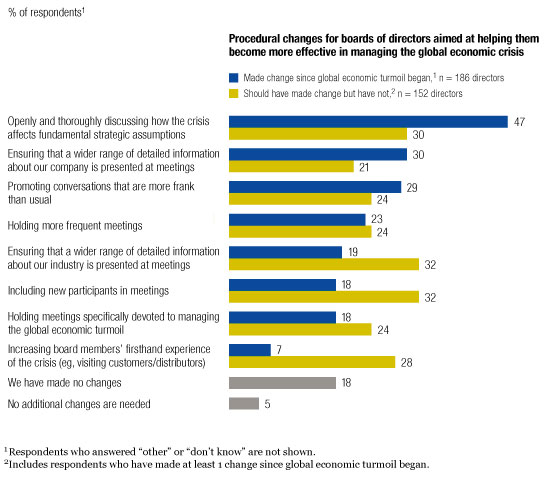

Today, boards are probably underreacting to the stresses—and opportunities—of economic turmoil. Directors themselves seem to agree: a McKinsey survey conducted in conjunction with an article published earlier this year1 showed that only half of the 186 directors responding thought their boards had met the demands of the crisis. Just 30 percent reported that a wider range of information was now presented at board meetings or that conversations were more frank than usual (exhibit). Even among directors who believed that their boards had responded effectively, overall, to the crisis, only 19 percent felt that those boards had really addressed the problems of talent management—meaning not only the composition of the board but also its role in hiring and remunerating senior executives.

Underreacting?

Boards need to assess their performance thoroughly and honestly to figure out what they must change, how urgently they must change it, and where they should start. That view is widely shared: many submissions to the UK Financial Reporting Council’s current examination of Britain’s Combined Code of Corporate Governance, for example, recommend that boards regularly conduct formal performance assessments.2 The ideas we propose here make sense in both bad times and in good.

Assessing the board’s effectiveness

During a crisis, when a board’s agenda is already overflowing with reports from the front lines, it can be hard to find extra time for self-examination. But if a board is going to ask senior executives to reexamine the way their company is managed, it had better reexamine itself as well. In a recent report, the executive search firm Heidrick & Struggles concluded that 51 percent of European boards fail to meet reasonable standards in their “working style.” Three areas were of particular concern: the availability of directors for extra board meetings and discussions; the widespread absence of committees for special topics, such as audits, remuneration, nominations, and strategy; and the excessively long service of some directors.

A simple solution would be to ask each board member to fill out a survey with questions on topics such as the frequency of board meetings, their agendas, the materials presented at them, the time allotted for agenda items, the nature of the dialogue, the contributions of various individuals, access to management and staff, opportunities for less formal discussions, and the way action items are followed up. More elaborate processes can be probed with additional questionnaires reinforced by interviews with directors and conducted by the senior nonexecutive director or an independent adviser. Once the answers have been assembled, the chairman should lead a discussion about them with the whole board.

Care is needed to manage the process. The board’s discussion could be awkward because members may feel reluctant to criticize colleagues or make remarks that might undermine the chairman’s authority. Answers should therefore be presented anonymously and circulated among all board members before open discussion, which ought to consume an entire board meeting. Then the chairman and the senior nonexecutive director should formulate recommendations for change and present them at a second meeting. The open discussion during the first one makes for a wider, freer debate on the issues, without the pressure of decision making. Decisions must nevertheless be made, but at another meeting.

For some boards, a full self-assessment during the thick of the crisis may seem like a luxury. One company decided instead to focus on the immediate changes needed. Directors were asked to rate the degree to which the crisis had disrupted the company’s normal operating environment and how drastically the board needed to change its agenda and style of interaction with management. The responses showed that a majority of board members desired significant change. A rich discussion led to the introduction of an open-issues agenda item at each board meeting, the elimination of some purely informational reports, greater exposure to executives of divisions, and a resolve to change the mix of skills around the boardroom table.

In another case, the assessment resulted in a small but significant change. Principle accounting judgments, normally discussed at length only in the audit committee, were now included on the full board’s agenda. That move has increased the level of scrutiny for critical accounting decisions, generated a lively debate about the financial performance of the company, and helped educate directors less familiar with its important accounting issues.

Past decisions that went wrong are worth special attention. Boards can identify those that now seem unwise—say, an increase in debt to pay special dividends, hiring executives to lead new growth initiatives, or major acquisitions that stretched balance sheets. The chairman can then ask for a review of the board’s decision-making process, including the stated and unstated assumptions and the formal and informal discussions around them.

In many cases, a board will find that a decision was sound when it was made but that the business environment then changed unexpectedly. Some decisions, however, will be exposed as flawed from the start, and the lessons learned from them will help revitalize the board. At a company with two strong divisions, for example, the board concluded that it had supported a disastrous acquisition by one of them at least in part because the other had made a successful acquisition two years earlier. In retrospect, the board concluded that having supported the first acquisition, it had felt it should also, in fairness, support the second. Directors resolved to change the two divisions’ culture of rivalry.

Fresh information and conversations

Boards normally spend most of their time reacting to management proposals. Yet today, as managers focus on cost cutting and survival, boards can look further ahead, to identify “the new normal.” To that end, they will need new kinds of information, as well as new kinds of conversations among their members.

Chairmen can expose their boards to new sources of information—such as new performance benchmarks, new customer demands, or new financial perspectives—in many ways. One involves tapping into the rich experience of nonexecutive and executive directors who also hold external appointments. Each board member can be asked to share one fresh idea as part of a discussion about the company’s future. Given the rich sources of insight a diverse board offers, it’s ironic that some banks have been widely criticized for having directors who are not qualified bankers. When the world is changing rapidly, diversity is more valuable than homogeneity.

One company used a more structured approach built around Porter’s five forces—the intensity of competition, the power of customers, the power of suppliers, the threat from new entrants, and the threat from substitute products—a framework that encourages a comprehensive outside-in view of businesses. Each board member was asked to describe a recent experience that suggested how these forces might shape the company’s future. One mentioned that supermarkets had forced suppliers to offer a 60- rather than 30-day receivables period. Another explained that the margins of his company’s customers were collapsing. A third pointed to new competitors that had entered the bottom of the market in his home country.

The chairman of another company used a more traditional form of analysis to spark fresh thinking and discussion. He asked the finance director to lay out the company’s performance, using the DuPont equation—a ratio analysis tool used to measure the return on equity (ROE)—and then to highlight the operating and financial variables that drive it. The analysis compared the ratios that make up ROE before and after the crisis, showing clearly where it was and wasn’t hitting the business: for example, the cost of debt had increased dramatically and volumes had declined, but the gross margin hadn’t changed. The discussion helped directors decide where they wanted to focus their attention. As a result, they called for additional interest rate forecasts and cash flow information.

A discussion that brings out contrasting points of view is often essential for developing and testing new ideas. Boards can promote such discussions by bringing in facilitators or employing special techniques. For example, in Edward de Bono’s classic colored-hat approach (a thinking exercise designed to encourage group discussion and decision making), each round of debate is explicitly geared, not to the default style of the board member speaking, but to the style defined by the “thinking” hats: such as seeking information, proposing ideas, and skepticism. At a Central European bank, for instance, a normally skeptical executive director who had donned the “proposing ideas” hat turned out to have cogent thoughts about how the company could grow.

Boards should also design more challenging discussions about important current issues, for even when the economic environment is changing drastically, it’s easy to make decisions shaped by old, outdated paradigms. Chairmen ought to help their boards surmount this tendency—for example, by requesting that all significant proposals come with a “red team” report presenting contrary arguments. This document, which should be prepared by an external consultant, need not undermine the CEO’s authority; the chairman would merely request that the board hear arguments for and against any important proposal. The CEO would therefore have to think deeply before submitting the proposal, undecided board members could insist on a fuller discussion, and a rival paradigm might see the light of day.

Reviewing talent-management processes

As Warren Buffett has so crisply explained, “It’s only when the tide goes out that you learn who’s been swimming naked.” He was referring to companies, but the principle is equally applicable to board members and senior executives.

A company should start to appraise its talent-management system by reviewing the composition of the board. The assessment of its processes may have raised concerns about its effectiveness. Even if not, it’s important to make sure that the board’s membership is appropriate in view of the new economic environment. Does the board need one extra finance person and one fewer marketing person? Someone with experience in a banking crisis rather than in creating new growth platforms? An additional person familiar with developing economies, environmental challenges, or government relations? Some banks have been forced to change their boards radically, but most companies have yet to reshuffle the team.

Such discussions are hard to have in an open forum, so the chairman and the senior nonexecutive director may need to review the board’s balance with an adviser, such as a headhunter. The danger, of course, is overreacting by adding people with now-fashionable backgrounds—in areas such as risk, the environment, or China—rather than experiences that will help the board face the company’s probable future challenges. Any review must therefore start with the scenarios that help define those challenges.

The review of the board should also extend to top executives and to the company’s talent and succession processes in general. Some people previously identified as high flyers will now seem to be fair-weather fortune hunters. Others, formerly seen as solid but dull, may be rated more highly because they know how to control operations and costs. If a number of executives are rerated, the next step should be to redesign the processes so that future judgments are more balanced and less influenced by fashion.

At one company, for instance, the board felt that the talent pipeline of managers groomed for senior-executive and top-team positions—including the highest—had too many “growth gurus,” reflecting the zeitgeist of the era when they were hired. The new vision was that the company needed more “operators,” with stronger experience in controlling costs, restructuring, and emergency intervention. The management group had become a little too homogenous, a little too removed from core operating skills, so the board sent the company’s HR processes back to the drawing board for a complete redesign that emphasizied operations.

Boards can also view the crisis as an opportunity to reassess the compensation architecture: base pay, expenses, bonuses, and long-term incentives. Many argue that poorly designed remuneration processes contributed to the problems many companies now face—in particular, that such processes were one reason why so many financial-services firms followed the same risky strategies.

Much criticism has also been directed at the way remuneration committees operate. There are many systems for calculating total returns to shareholders, developing benchmarks, and comparing compensation schemes to those of other companies, for example, so these committees spent too much time on minutiae. They also failed to focus on the big picture because presentations by remuneration experts often dominated their agendas, leaving too little time for broader debate about the overall objectives of the compensation scheme, its appropriateness for the company and the corporate strategy, and the likely reactions of shareholders, employees, the financial press, regulators, and local communities. Public outrage about executive compensation should be a helpful backdrop for a review of the basic pay architecture.

Many boards are underperforming at a time when they desperately need to excel. Any board that expects creative responses and extra performance from its management team must show that it too can raise its game.

Related Articles