Increasingly, Chinese consumers are behaving like their counterparts in the developed world. They are more demanding and pragmatic than ever as their horizons expand beyond basic concerns about product features. Also, they are willing to pay for better value and quality and are spending more time researching and are exploring product nuances. Yet McKinsey’s 2010 survey of China’s consumers also found that they are blazing a uniquely Chinese trail (see sidebar “About the research”). The country obviously offers some of the world’s biggest growth opportunities—but only for consumer product companies that understand and respond to this rapidly evolving marketplace.

Chinese consumers remain brand conscious but, unlike shoppers elsewhere, they focus on value so intensely that brand loyalty is often secondary. The needs or interests of their families have greater importance for them than for their counterparts in the developed world. Word of mouth has become a more significant source of product information than it is elsewhere, thanks largely to fast-growing use of the Internet, which Chinese consumers see as a credible information source (see sidebar “Chinese consumers and the Internet”).

Most intriguingly, though, China’s consumers prioritize purchases across different product categories by trading off among them: the Chinese maximize their buying power by spending more in the categories they care about most and less in others. Also, the size and reach of China’s far-flung markets mean that any trend’s impact may vary from place to place, depending on local circumstances (see sidebar “A geographically diverse consumer base”).

These trends bear witness to a transformation in the behavior of the Chinese as they develop into some of the world’s most complex consumers. China is now the planet’s second-biggest economy, after the United States, and its consumer sector may be the healthiest of any major country. In the past, consumer companies could enter China with their existing products, strip them down to basics, and then sell them at low prices throughout the country, thus hitching their wagons to China’s double-digit consumption growth. Today, local consumers, like those in developed markets, appreciate and demand better products. Many companies that have struggled to find a niche in China may therefore now find a market for their products and attract partners. Conversely, companies that have relied on low-cost, low-quality business models may end up on the losing end of trade-off decisions and could require a shift to value. In this article, we highlight the major changes in Chinese consumer behavior and offer some ideas about how to address them.

Fewer trips, bigger baskets

Historically, Chinese consumers have shopped about five times a week more often than their US counterparts, but their average basket size has been only a quarter of the US equivalent. Our research this year, however, found that shopping frequencies were declining and basket sizes growing. Overall, in China’s home and personal-care category, the number of weekly purchasing trips fell from 0.6 in 2008 to 0.5 in 2010; the average basket size rose from 18.42 renminbi in 2008 to 24.10 renminbi in 2010.

The trend toward fewer but more costly shopping trips reflects the Chinese consumer’s convergence with developed-world norms. One reason for this change is that Chinese shoppers are increasingly attracted to modern retail formats such as hypermarkets, which offer a broad selection of attractively priced goods of consistent quality. Also, the Chinese have more money than they did and can spend more on each shopping excursion, so they don’t have to waste time making multiple trips to stores. This finding suggests that as the Chinese consumer’s quality of life improves, time becomes more valuable.

One unusual aspect of the evolving behavior of Chinese consumers is their enthusiasm for shopping as entertainment: families transform shopping trips into fun days at the mall or hypermarket. In our survey, some 73 percent said they regarded shopping as a leisure activity, 45 percent identified it as one of their favorite pursuits, and just over half said it was among the best ways of spending time with the family. Those numbers are greater—by an order of magnitude—than those for consumers in the West. Chinese consumers often shop without any intention of buying. Sometimes they are window-shopping or comparing prices. At other times, they may be shopping as a sport, competing with friends to find the best deals.

Chinese consumers still shop much more frequently than their counterparts in developed markets do, but we expect the trend to fewer visits and bigger basket sizes will continue, at least among segments such as young professionals with families. As a result, we think many current global retailing practices will become more relevant in China—from bigger package sizes to home delivery services to loyalty programs. Also, fewer shopping trips mean fewer chances to hook consumers, so companies will have to maximize each opportunity, perhaps using promotions such as instant coupons and bundled-product discounts. Compelling in-store displays will rise in importance.

Attracting consumers to the stores will increasingly be front of mind. In several cities, the French hypermarket chain Carrefour runs a fleet of regularly scheduled buses for shoppers and offers free parking. In the future, making the shopping experience even more a form of family entertainment could prove fruitful—for example, putting restaurants on the premises of stores, adding children’s play areas, or opening adjacent movie complexes.

More than the basics

For years, Chinese buyers have regarded a product’s functional attributes—does it work reliably or taste good?—as the most important buying factor. That’s still true, but our survey also found a shift toward more sophisticated criteria. Flat panel–TV buyers, for example, are now concerned not only with picture quality but also with aesthetic appeal or innovative features. Purchasers of laundry detergent increasingly demand a “good scent” (up to 61 percent this year, from 40 percent in 2008) and “appealing package design” (28 percent today, compared with 16 percent in 2008). As in other parts of the world, this development reflects a transition to an environment where consumers have the means to demand more than basic product features, and catering to refined tastes is increasingly the norm.

Nonetheless, a local perspective informs purchase decisions. After a spate of food safety scandals, Chinese consumers, like their counterparts in the developed world, have become more health conscious. Much more than elsewhere, fear of possible contamination has driven a broader concern about unsafe products, especially everything used by children (food, beverages, toys, and apparel). As a result, Chinese mothers have become among the most sophisticated in the world at looking for materials or ingredients they deem potentially harmful for their children.

Chinese shoppers are also moving in the direction of consumers elsewhere in that emotional considerations increasingly influence purchase decisions. In particular, the importance of any given purchase’s status value has grown strongly since 2008, especially for aspiring or lower-middle-class consumers, for whom the appearance of success is most significant. Another fast-growing key buying factor is the “what fits me” (or “what’s good for me”) category emerging in China’s younger (and more affluent) mass-market demographic. These shoppers are less concerned about following the crowd or the way what they buy defines them in the eyes of others than about how specific products fit their real-life needs. This factor is the main reason consumers trade up when their circumstances change and also explains why they tend to be more satisfied with better products. The “what fits me” mentality, prominent mainly in major cities such as Shanghai, will probably grow in significance nationwide as incomes rise throughout the country.

In addition, intangible, emotional factors are beginning to drive the purchase decisions of younger, often better-off consumer segments. This trend favors companies that had problems marketing products in China but can now create effective strategies resembling those long used in Western markets. These companies could create emotionally driven consumption occasions (in social settings, for example) or introduce brands aimed at satisfying emotional needs (for example, self-indulgence or rewards).

Brand appeal, but only at the right price

One tenet of Chinese retailing is that consumers are extremely brand conscious: 45 percent believe that higher prices correspond to better quality, compared with just 16 percent in the United States and 8 percent in Japan. Likewise, far more Chinese consumers than shoppers elsewhere are willing to buy more expensive branded products.

Chinese consumers are extremely pragmatic, however, so they base purchase decisions on more than just branding. Indeed, the fact that Chinese consumers are conscious of brands does not necessarily mean they are loyal to them. While consumers tend to gravitate toward the biggest brands, the assessment of relative value offered by a handful of competing products is often the basis of choice. Our survey showed that 23 percent of shoppers in China would go out of their way to buy from stores that offered the best prices, compared with 18 percent in the United States and 12 percent in Japan. While quality remains a critical consideration, value is the most important one.

Chinese shoppers first budget for purchases, then compile a shortlist with a handful of specific brands, and finally hold a “beauty contest” to determine the most appealing one. The decision often involves significant research, perhaps conducted in leisure time window-shopping. Since consumers generally make the final purchase decision in stores, promotions and ads in their premises are still effective to tip the balance toward particular brands. In addition, promotions often lead shoppers to make impulse purchases as they seek to maximize value by stocking up on perishables.

The pragmatic trade-off

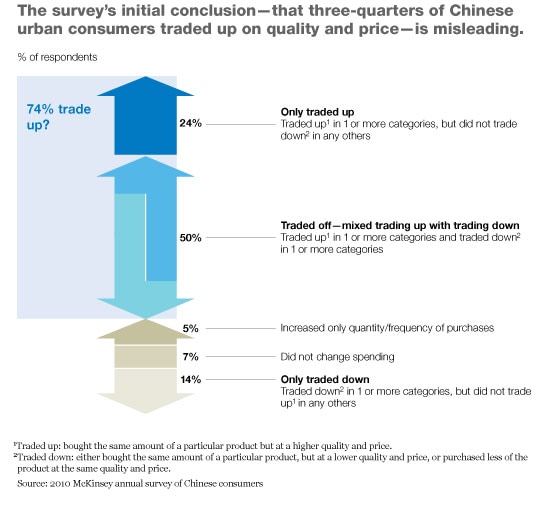

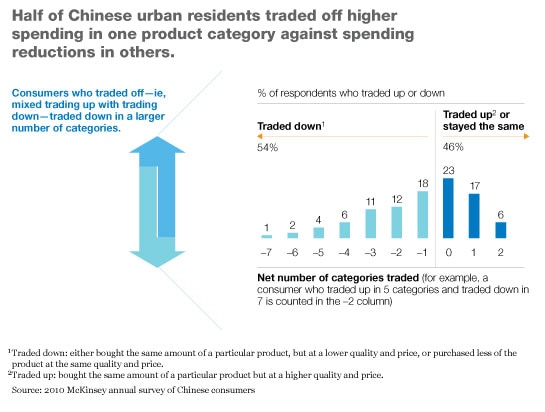

As income rises in China, so does the desire to buy more and better products. In our survey, we found that three-quarters of urban households said they had traded up in at least one product category. This trend accounted for half of all consumption growth nationwide in 2009. But trading up is only half the story. Chinese consumers are doing so by explicitly choosing to finance increased spending in categories that mean the most to them by “trading off”—cutting expenditures—in less important categories. That’s why 2010’s 74 percent upgrade rate is misleading (Exhibit 1); in reality, only 24 percent of consumers upgraded without trading off. Fully 50 percent of Chinese urban residents actively traded off spending increases in one product category with reductions in others. Trading up in one to three categories involved corresponding reductions in as many as seven (Exhibit 2).

Obviously, trading off isn’t a specifically Chinese phenomenon. When we compare China with developed countries, differences are clear, however. Consumers elsewhere tend to trade up as they get wealthier. Some start relying on credit, often spending more than they can afford. Not in China. Consumers there remain very concerned about financial stability and spend within their means. When Chinese consumers decide to spend more in a category they particularly value, they generally trade down in one or more less compelling categories. These behavior patterns underline our assertion that the Chinese have become among the world’s most pragmatic consumers, willing to make explicit choices about spending their growing income. This is an important insight for marketers seeking growth opportunities.

Our survey found significant trade-off activity in seven product categories. More than 70 percent of trade-up demand for dining out and 50 percent for alcohol come from white-collar men who want to improve their standing with clients or colleagues and trade down on personal-care and packaged-food and snacking products to balance their overall spending. Some 80 percent of trade-up demand for higher-quality clothing, shoes, and accessories came not from high-income “fashionistas” but from lower-middle-income consumers looking to impress job interviewers or advertise their ascent from the working to the consumer class. In each case, trade-down decisions in three to four product categories balanced increased spending.

This distinctive consumption trend has implications for the way companies develop local marketing strategies. For one, they can invest more in consumer education (for example, through corporate Web sites or in-store promoters) to encourage trading up. Manufacturers that focus on convincing consumers of the importance of a particular category—and, within it, of a better, more expensive product—have a stronger chance of persuading potential buyers to upgrade in that category rather than another one. Apparel manufacturers, for instance, often emphasize the importance of owning better, trendier clothes to showcase one’s status. We find that consumers who buy into this idea are much more likely to upgrade their purchases of clothes and accessories, trading off in other categories.

Companies can also use cross-category promotions to influence purchase decisions in a category consumers have targeted for upgrading. Since consumers who upgrade their entertainment venues may well upgrade their alcohol consumption, wine and spirit vendors might partner with trendy bars and restaurants. Consumers who upgrade dairy products are likely to upgrade their snacks, chocolates, and health supplements, creating further copromotion possibilities.

Smarter shopping and word of mouth

Chinese consumers have adopted various techniques to help them decide which products to buy. Online comparisons or reviews are increasingly important research tools for younger audiences and for the middle class and above—the Internet had about 420 million users in mainland China by June 2010.1 These trends are broadly in line with consumer behavior throughout the world.

In our 2010 survey, 56 percent of Chinese consumers said they regarded online advertising as credible, up from 29 percent in 2009. Similarly, 70 and 67 percent of Chinese shoppers said they found retailers’ and manufacturers’ Web sites, respectively, credible. (In the developed world, by contrast, consumers prefer to get product information from third-party sites.) The fact that online information is so highly regarded in China makes the Internet extremely important for shaping consumer opinion. On average, 25 percent of mainland shoppers said they never buy a product without first checking the Internet, compared with half that percentage in the United States. For big-ticket items, the proportions can be significantly higher in China, approaching 45 percent for autos.

Chinese consumers do much more research before purchasing a product than average consumers in the developed world do, so middle-class consumers often take a long time to make decisions, if only because some things can cost more than their monthly income. In a survey on PC purchases, for example, Chinese consumers said they might take three to six months to buy a computer and visit a store three to five times. Decision making is especially protracted for big-ticket items but can take quite a while for foods, beverages, and personal-care offerings, as well, given the increasing number of brands and new products available.

Word of mouth has grown strongly in recent years as a source of consumer information: shoppers are sounding out family and friends and getting advice online through chat forums. True, television advertising continues to dominate in China as an information channel for products and brand awareness. But word of mouth is by far the next most popular source of leads: in 2010, 64 percent of respondents said that it influenced their purchasing decisions, compared with 56 percent in 2008. Word of mouth and online research also play an important role in complementing TV ads by helping consumers to analyze the merits of different products and to arrive at their final decisions.

Word of mouth may be more powerful in China than in developed countries. An independent survey of moisturizer purchases, for example, observed that 66 percent of Chinese consumers rely on recommendations from friends and family, compared with 38 percent of their US counterparts. Word of mouth seems to have become such an important channel because a huge number of brands and offerings now tempt Chinese consumers—who are not accustomed to such product diversity—as well as the fast pace of product innovation. While TV demonstrates which brands are big (and therefore a “safer” choice), it is not a trusted medium; in-store information is critical but mostly influences the final decision. Chinese consumers therefore want to shape their short list with help from family and friends. Often, they also aim to make sure that their choices make them look smart.

For companies, these findings suggest that it has become essential to invest in and develop a world-class Web site that provides extensive information to consumers. Viral marketing is crucial too. In one product category we recently researched, we found that recommendations from SMS (short message service) text messaging accounted for nearly a quarter of the influence on the final brand selected. Some manufacturers have set up sites on the Web to promote discussion of their products in forums they control.

One of the clearest messages from our 2010 survey is that as Chinese consumers become more like their developed-market counterparts, they are also creating a distinct identity. They have not only distinctive tastes and priorities but also unique ways of choosing and buying products. As new offerings emerge and more people in China find themselves with significant discretionary income and choices, consumer product companies must adapt their strategies to capture the opportunity.

Related Articles

Capturing the world’s emerging middle class

Building a second home in China