If focusing on competitors leads strategists inexorably to the notion of sustainable competitive advantage, focusing on the customer leads them to the notion of value. In the 1981 staff paper "Market strategy and the price-value model," Harvey Golub and Jane Henry introduce a framework designed for industries whose products have a sizable share of intangible or subjective value. Every product or service gives customers some benefit, for which they are willing to pay up to some maximum price. In microeconomic terms, this maximum is the "reservation price," or, in Golub and Henry’s lexicon, simply the value the customer ascribes to the product. The strength of the buying proposition for any customer is a function of its value to that customer, minus the price—in other words, the surplus value that the customer will enjoy once that product is paid for. Golub and Henry’s model plots all products in a certain market on a two-dimensional price-value graph, enabling the strategist to identify underpriced and overpriced products and to spot regions of price-value space that are relatively free of products and therefore ripe for new entries.

Another price-value model, designed more for business-to-business equipment sales than for the consumer goods market, is described in a 1979 staff paper by John L. Forbis and Nitin T. Mehta. Their "Economic value to the customer" framework is based on a simple observation. To get customers to switch from some other product to yours, you have to give them at least as much value beyond the price they are paying—that is, at least as much surplus value—as they are receiving from the product they currently use. This paper is a good example of the emphasis on detailed analysis and quantification that pervades all of McKinsey’s strategy work.

A 1988 staff paper by Michael J. Lanning and Edward G. Michaels combines the value maps developed in the price-value models with the idea of the "business system," which was introduced in 1980. The paper, "A business is a value delivery system," emphasizes the importance of a clear, well-articulated "value proposition" for each targeted market segment—that is, a simple statement of the benefits that the company intends to provide to each segment, along with the approximate price the company will charge each segment for those benefits. Lanning and Michaels use value maps for each customer segment to reveal which value propositions are most likely to appeal strongly to specific segments. Then, to help managers implement their value propositions throughout their companies, the authors introduce an important extension of the business system: the concept of the value delivery system, which is geared toward advancing the value proposition at each stage of production and distribution.

Of the dozen articles in this section, some have emphasized sustainable competitive advantage and other aspects of rivalry-based competition, while still others—especially those based on price-value models—have been more concerned with meeting the needs of the customer. In a 1988 article published in Harvard Business Review, Kenichi Ohmae addressed these competing strains of strategic thinking head-on. At the time, the business culture of the United States was obsessed with Japan and the rivalry-based competitive model that had apparently given rise to that country’s world-beating economy. In "Getting back to strategy," Ohmae questions the wisdom of a single-minded focus on rivalry and industry structure. He reminds us that the best strategists, though they will not walk away from battles that clearly must be fought, avoid competition whenever they can, and he argues forcefully that strategy should be less about defeating the competition and more about creating value for your customers.

Market strategy and the price-value model

Harvey Golub and Jane Henry

Everyone knows what is meant by the "price" of a product. But just as important for strategic purposes is a product’s value to the customer, something that is far less conspicuous because it often depends on the customer’s subjective assessments. A product’s value to customers is, simply, the greatest amount of money they would pay for it. In other words, a product will rarely be purchased when its price exceeds its value to the customer. Conversely, whenever the value of a product exceeds its price, customers can improve their lot by buying it.

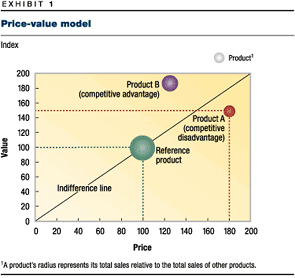

From a strategic perspective, price and value are the only parameters that really matter to the customer, so it is important for managers to understand the interaction between them. We designed the price-value model for precisely that purpose. To apply the model, start by choosing a reference product or reference service—usually the one with the biggest market share in the industry. (If your own firm leads the market, the second-biggest seller will do.) Exhibit 1 shows that if you plot the product according to its price and value to its average buyer and define that point at (100,100), you can then plot all other products in the market against the reference product. For instance, if a product sells for 180 percent of the price of the reference but gives customers only 150 percent of the value, the product should be plotted at (180,150), like Product A in the exhibit. The radius of each bubble is proportional to sales.

Remember to define the market broadly enough to show the full range of product substitutes. For instance, when Southwest Airlines was setting its prices for flights within Texas, it sought to compete with bus and automobile travel as well as with other airlines. As a rule of thumb, you can expect that consumers will be equally willing to buy products that lie anywhere along the diagonal line passing through the reference product—which is why we call it the "indifference line." For instance, if a product costs twice as much as the reference but also yields exactly twice the value, it is just as good a deal, and customers should be equally happy with either product.

The tricky part of constructing a price-value map is estimating a product’s value to the average customer. Often, with a general knowledge of the industry and a modest amount of analysis, you can arrive at a number that is close enough to highlight the important strategic issues. We recommend that analysts identify a handful of product or service features that customers care about most and then try to determine—empirically, in many cases—the approximate value of each. For instance, someone drawing a price-value map for Federal Express might decide that the industry’s key components of value are speed of delivery, the number of cities served, reliability, and the existence of a tracking service and a pick-up and delivery service. The analyst would then try to measure the importance of each element to various classes of consumers.

Under the conditions of perfect competition, all products and services should cluster around the indifference line. But in reality they can lie above or below as a result of such things as government regulation, customers’ imperfect knowledge of their options, and other deviations from perfect market conditions. As a general rule, products below the line lose market share over time, and those above it gain, as buyers steer themselves toward products that give them more value for their money. To reveal particular segments that are being over- or undercharged for the value they are receiving, it is sometimes useful to represent customer segments with different bubbles on the same chart.

The model works best when used to compare products with great intangible or subjective value. When a product’s value is more concrete, as in the case of an industrial product whose owner will enjoy predictable increases in sales or decreases in costs, we recommend starting with the "economic value to the customer" model, discussed below.

In the best case, the price-value model can help a company visualize its current competitive position in the market and assess all available options: changing the price of the product (to some or all customers), changing its value (again, to some or all customers), and any combination of the two. For instance, a product far to the left of the indifference line for a particular market segment is likely to be underpriced. Its producer might want to hold its value constant and raise its price or hold its price constant and lower costs in a way that sacrifices some value. A large gap along the indifference line often represents a market opportunity, since a company that creates a product or service to fill that gap has no close competitors.

In general, many of the numbers used for "value" in a price-value map will necessarily be informed guesses. Still, even an approximate map is much more useful for strategic purposes than no map at all, and it can also serve as a good internal communication device for explaining a company’s strategic marketing decisions.

About the Authors

Harvey Golub and Jane Henry are alumni of McKinsey’s New York office. This article is adapted from a McKinsey staff paper dated August 1981.

Economic value to the customer

John L. Forbis and Nitin T. Mehta

Few suppliers go to the trouble of estimating exactly how much economic value the customer receives from their products. But we feel that determining economic value is such a worthwhile exercise that we have developed a tool for that very purpose.

The goal of EVC (economic value to the customer) is to quantify the additional value a product brings to customers above what they already receive from their present suppliers. The model can be used to figure out how much the customer will pay to switch from one product to the other, so it is a useful tool for solving strategic pricing problems. EVC can also help a supplier discover which customer segments value its product most and why—enabling the supplier to segment the market more precisely, to design its product to meet the needs of the most profitable segments, and to charge those segments a premium for the extra value they receive. The model is particularly well-suited to industries that sell to business or, more generally, to industries that require buyers to absorb significant start-up or operating costs to use their products. (For most consumer products, whose value to the customer is less tangible and whose start-up and operating costs are low, the price-value approach makes more sense.1

Since EVC varies from one customer segment to the next, the first step of the process is to choose a particular segment to focus on. Next, select a "reference product"—often a competitor’s—that a typical customer in the segment is assumed to be using at the outset. Finding the right reference product is critical. Depending on the strategic choice you are trying to make, you can employ the product that is currently being used by the customer segment, the product of any particular competitor, or even your own company’s last-generation product. But don’t draw your candidates from too narrow a pool: any product the customer uses to satisfy the same underlying need that your product satisfies can be a valid choice.

What would make the customer switch?

The main principle of EVC is that for any customer currently using the reference product, there are two possible ways of benefiting from switching over to yours. First, your product may have better functionality; it may simply do its job better or faster (a more comfortable airplane, a faster computer, or a production line with lower error rates). In the business-to-business context, functionality often means that your product enables the customer to charge its own customers higher prices, to work more efficiently, or to earn more profit in some other way.

Second, your product might outstrip the reference product by placing lower burdens on the customer. Especially if you are focusing on business equipment, the reference product might require its buyer to incur certain start-up or postpurchase costs. By "start-up costs," we mean such things as insurance, installation, and employee training. By "postpurchase costs," we mean maintenance, data entry, ongoing employee training, and so on.

These ideas lead naturally to EVC in the following way. Economic value to the customer is simply the purchase price that customers should be willing to pay for your product, given the price they are currently paying for the reference product and the added functionality and diminished costs provided by your product. Start with the purchase price of the reference product and then add improvements in functionality and cost savings to the customer. You are left with the amount you should be able to charge customers for your product and still take their business away from the maker of the reference product.

Working out how much you can charge

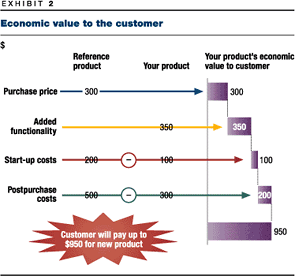

Let us look more closely at the example illustrated in Exhibit 2. The reference product—the one that the customer already uses—costs $300. By switching to your product, the customer gains an extra $350 worth of functionality (yellow arrow). This $350 often shows up in increased profit because your product works faster, works better, appeals more to consumers, and so forth.

In addition to improved functionality, the customer who switches to your product enjoys a $100 savings in start-up costs (red arrow). Those costs were $200 with the reference product but are only $100 with yours. Finally, the customer’s postpurchase costs will drop from the $500 needed to operate the reference product to the $300 needed to operate yours—a savings of $200 (green arrow).

By switching from the reference product to yours, the customer will therefore gain $350 worth of functionality improvements (which may or may not mean $350 in profit improvements), plus $100 in lower start-up costs, plus $200 in lower postpurchase costs. (These last two obviously do mean straightforward profit improvements for the customer.) The customer, then, will enjoy a total of $350 + $100 + $200, or $650, in added benefits. A customer who is willing to pay $300 for the reference product should be willing to pay $300 + $650, or $950, for your product. That is the "economic value to the customer" for which the model is named. The EVC is exactly $950, as shown in Exhibit 2—and, in rough terms, that is what you could charge the customer if you wished. In reality, in the example shown in the figure, charging the full $950 for your product would leave the customer perfectly indifferent between the reference product and yours. Therefore, you might want to charge somewhat less than $950—say, $825 or $850. In other words, you want to cede only enough value to customers to make them switch to your product, but not much more. EVC can help you do just that.

Start-up costs are basically a one-time expense for the customer. To simplify our explanation, we have also represented a product’s functionality and postpurchase costs as one-time items. In fact, they are really streams of revenues or expenditures that will be realized over the years. In practice, a present value, calculated with an appropriate discount rate, should be used to account for these value streams.

A big strength of EVC analysis is that it highlights the different values for each customer segment. Customers in one segment may value a product much more highly than those in another, and EVC provides a way of quantifying these differences. By finding a few key product variables that explain the differences in EVC across various segments, you can often come up with powerful, sometimes counterintuitive ways to segment the market. It helps if you think broadly: don’t limit yourself to market segments served by your company. Other segments might find your product useful if only they could be persuaded to try it.

Of course, the whole EVC process is only as good as the information put into it. Computing a product’s true value to the customer often calls for a series of detailed field interviews. But it is frequently worth the trouble. It can not only help you solve pricing problems but also, over the long term, permit you to do the kind of creative market segmentation that can yield strategic advantages.

About the authors

John Forbis and Nitin Mehta are alumni of McKinsey’s Cleveland office. This article is adapted from a McKinsey staff paper dated February 1979.

A business is a value delivery system

Michael J. Lanning and Edward G. Michaels

Customers base their buying decisions on two criteria: the benefits of a particular product or service and its price. The benefits can be reduced to a single number: the most the customer would be willing to pay for that product or service. That number, minus the price, represents the product’s value to the customer. If you are willing to pay up to $2 for something and its price is $1.50, buying it nets you 50 cents’ worth of value. In general, customers will purchase the good or service, among competing alternatives, that creates the most value for them.2

Increases in a product’s share of the profit in any market almost always reflect a perception that the product is giving its customers superior value. So the delivery of superior value—through higher benefits, lower prices, or some combination of the two—lies at the heart of any winning business strategy. Often it is possible to deliver superior value only to a particular subgroup of customers, perhaps one or two customer segments. That is no cause for concern. But make no mistake: to thrive, a company must deliver superior value to someone.

We believe that behind any winning strategy must stand a superior value proposition—a clear, simple statement of the benefits, both tangible and intangible, that the company will provide, along with the approximate price it will charge each customer segment for those benefits. All of the company’s customers should see significantly more benefit from the transaction than they are being asked to pay. For instance, Frank Perdue transformed the chicken business when he produced a more tender chicken with a consistently golden skin color. He believed that he could charge a premium of 10 to 30 percent for such a product and still leave many customers with enough value to make them choose it over the available alternatives.

Developing a value proposition

Some managers have a value proposition handed to them—for instance, by a technological breakthrough that happens to occur on their watch. But many have to rely on more systematic methods. The first step, in our view, is to work out exactly which benefits potential customers want and how much they will pay for them.

And we are not talking about vague benefits, such as "good quality." We mean concrete, observable features of the product or service: short waiting times, fast rewind speeds, and so on. Understanding customer preferences at this level of detail almost always calls for a great deal of management time and attention. Usually, it also involves some quantitative market research as well as other diagnostics: systematically listening to customers and distributors about customer preferences, analyzing actual marketplace behavior, and test-marketing new benefit or price concepts.

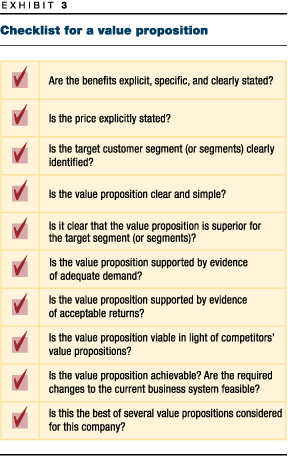

Knowing exactly what customers value enables you to divide potential buyers into segments—groups of potential customers who desire more or less the same product benefits and are willing to pay more or less the same amount of money for them. Once you have a map of all the relevant customer segments, you can assess the opportunities for your business unit to deliver superior value to each. A business unit’s ability to deliver value can vary widely from one segment to another, and the unit will often be able to pursue just one or two segments profitably. That means offering the people in those segments the benefits they desire, at or below the desired price, so that competitors can’t easily match the results. (To test a potential value proposition, go through the checklist given in Exhibit 3.)

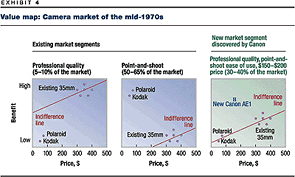

Canon’s strategy in the camera market in the mid-1970s provides an example of canny market segmentation. At that time, the market apparently consisted of two segments: the professional-quality segment, whose members were willing to pay over $300 for a camera, and the point-and-shoot segment, made up of those who didn’t mind photos that looked like snapshots and wanted a camera that cost under $100. Canon thought there might be a third category, containing millions of people who sought the quality of a 35-millimeter camera in an easier-to-use form and at a price between $150 and $200. Canon invested heavily in developing and mass-marketing such a camera—the AE1—and the rest is history.

One device that may help a company recognize the specific value propositions that will appeal to various segments is a value map. To create one, draw a two-dimensional graph for each market segment, showing the total benefit along the y-axis (what those in the segment are willing to pay) and price along the x-axis (what they pay in the current market). Each competing product or service can be depicted as a point on the graph.3 Take a look at Exhibit 4. As you can see from the center chart, for people in the point-and-shoot segment a Polaroid or Kodak camera actually brought more total benefit than a professional-quality 35-millimeter one. And for the new market segment in the right-most chart, the AE1 was better than any of the alternatives. (In general, a new product that lies far to the upper left of the existing alternatives will be preferred by a given segment.)

Having decided how a business unit can bring superior value to various segments, you can estimate the profit and growth opportunities that each segment holds. Then you can plan a long-term strategy by selecting the segments and value propositions that promise the best results.

The value delivery system

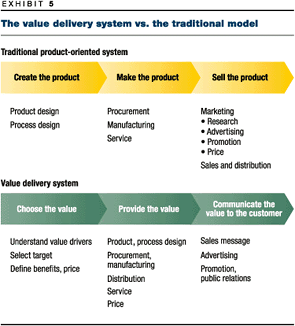

Having selected a particular value proposition, you must see to it that this proposition "echoes" throughout the business system to ensure that each activity of the company serves to reinforce the chosen value. New value propositions can certainly lead to a winning strategy, but so can superior echoing of a more ordinary value proposition. The value delivery system is a useful framework for evaluating this echoing process.

Traditionally, managers break down their business systems in production terms. "Step one: create the product. Step two: make the product. Step three: sell the product." This may be useful for production-side projects such as cost cutting. But if you are trying to deliver a compelling value proposition, it makes more sense to divide up the business system into customer-oriented stages: choosing the value, providing the value, and communicating the value to the customer. A business system thus broken down is called a value delivery system, and in preparing it you should be able to describe the role that each department and employee plays in one or more of these three value-related tasks (Exhibit 5). Only then can you be sure that your chosen value proposition pervades every layer of your organization.

Remember, the winning strategy is often the one that best implements its value proposition, not the one whose proposition has the greatest appeal. Good execution provides its own obstacle to imitation because it is difficult to achieve. If an organization takes the value delivery system seriously, its managers can ask each department to contribute to the chosen measure of value. This may mean that the manufacturing side must compromise its cost-efficiency record to allow for the introduction of a new formula or that the ad agency must develop advertising that communicates the value proposition instead of pursuing some potentially award-winning but irrelevant idea. Each link in the chain will then be less inclined to pursue its own parochial aims and more likely to serve the unit’s overarching goal: adding the right kinds of value for the right customer segments.

About the authors

Michael Lanning is an alumnus of McKinsey’s Atlanta office, and Edward Michaels is a director in the Atlanta office. This article is adapted from a McKinsey staff paper dated June 1988.

Getting back to strategy

Kenichi Ohmae

In economic-policy circles in Washington and Europe, "competitiveness" is the word of the moment. And senior managers, who were wrestling with this issue long before politicians got hold of it, are searching for models that can teach them how best to play the new competitive game. With few exceptions, the models they have found are Japanese.

The main lesson managers seem to draw from the Japanese examples is that a successful strategy means beating the competition. If it takes world-class manufacturing to win, you must beat your competitors with factories. If it takes rapid product development, you must beat them with labs. Only after a painful decade of losing ground to the Japanese are US and European managers learning this simple lesson.

The problem is that the lesson is wrong.

Customer needs should come first

Of course, winning the "battle" over manufacturing or product development is no bad thing. But going toe-to-toe with competitors should not come first in formulating strategy. What should come first is painstaking attention to the needs of customers and a close analysis of a company’s degrees of freedom in responding to those needs. Managers must be willing to rethink, fundamentally, the company’s products and how best to organize the business system that designs, builds, and markets them.

Tit-for-tat responses to competitors come second—after you have formulated a real strategy geared toward adding value for customers. Indeed, a good strategy should aim to avoid competition wherever possible. As Sun Tzu observed around 500 BC, the smartest strategy in war is the one that allows you to achieve your objectives without having to fight. The same is true in business.

Of course, direct competition cannot be avoided at times. The product is right. The company’s direction is right. The perception of value is right. And managers may have no choice but to buckle down and fight it out with competitors. But in my experience, managers are often too willing to leap into these competitive battles simply because this is something they know how to do. They have a much harder time seeing when an effective customer-oriented strategy could avoid the battle altogether.

A number of Japanese companies are now coming to this realization as they seek to solve a common problem: the danger of being trapped between the low-cost producers in newly industrialized countries such as South Korea, where wages are one-seventh to one-tenth those of Japan, and the high-end producers of Europe. Concerned about losing the battle on both of these fronts, some Japanese managers are at last rethinking the premise of head-to-head competition itself.

The analysis goes like this. To meet the South Korean players head-on, a Japanese company would have to work single-mindedly, fiercely, and unceasingly—by full automation and capital intensification—to take the labor content out of its products. South Korean labor is simply too cheap to permit any other approach. A potentially more appealing option is to compete directly with, for example, German companies, in the upmarket game. In practice, however, this has proved hard for the Japanese to do. Their corporate cultures promote an inwardly focused rivalry among the big Japanese firms, stressing market share at any price, rather than an outward-looking, global battle for profits.

Creating value for the customer

What the Japanese companies need is a strategy that avoids head-to-head rivalries with both South Korea and Europe. A few companies are discovering such a strategy, generally by returning to the simple goal of creating value for the customer. Take, for example, Yamaha, which had struggled to capture 40 percent of the world piano market only to see global demand for pianos decline by 10 percent a year. The way out of Yamaha’s doldrums was to be found neither in cost cutting nor in becoming the next Steinway. It was to be found—believe it or not—in player pianos.

Given the shrinking sales figures, the challenge was to wring some value out of the world’s existing 40 million pianos, many of which were sitting in living rooms collecting dust. So Yamaha created a digital and optical technology that could distinguish among 92 degrees of strength and speed of key touch. For $2,500, you can now retrofit your piano, controlled by a floppy disk, to play the way Horowitz did in Carnegie Hall. That is a potential market of $100 billion ($2,500 to retrofit each of 40 million pianos), to say nothing of downstream revenues from tuning, new lessons, and so on—not bad for a declining industry. This is how you create a value-adding strategy: by thinking about how best to provide value to customers rather than by aping the competition.

Some time back, a Japanese home-appliance company was trying to develop a coffee percolator. Executives were asking, "Should it be a General Electric-type machine? Should it be the drip-type of the kind Philips makes? Larger? Smaller?" I urged them to ask a different question: "Why do people drink coffee?" The answer came back—good taste. After further research, the company found that this "good taste" had a few critical components: water quality, coffee-grain distribution, time elapsed between grinding and brewing. Certain things mattered more than others. That got the company thinking differently about the percolator’s essential features. Suddenly, it had to have a built-in dechlorinator and, of course, a built-in grinder.

If you pay attention only to your competitors, you compete only on the features that they, perhaps wrongly, consider important. If you focus on the fact that the new GE machine brews coffee in ten minutes, you will work feverishly to make a machine that brews it in seven. Never mind that the customers are nearly indifferent.

Unless you step back and ask, "What are the customer’s fundamental needs, and what is this product really about?" you may find yourself winning heroic battles in an irrelevant war. You will produce an ultra-low-cost piano that no one wants to buy, or a percolator that can brew a pot of undrinkable coffee almost instantaneously, or a forklift that piles up a record number of boxes but doesn’t allow operators to see directly in front of themselves.

These critical lessons are helping a few Japanese companies see their way out of the false dichotomy between low-cost Hyundai and high-end BMW modes of competition. There is no need to follow any other company’s rules in this way. And it is these lessons that managers in the United States and Europe should be learning from the Japanese example. They should be getting back to strategy—back to the central task of any strategist, which is to find better ways to deliver value to customers.

About the author

Kenichi Ohmae is an alumnus of McKinsey’s Tokyo office. This article is adapted from an article published in Harvard Business Review, November–December 1988. Reprinted by permission. Copyright © 1988 President and Fellows of Harvard College. All rights reserved.