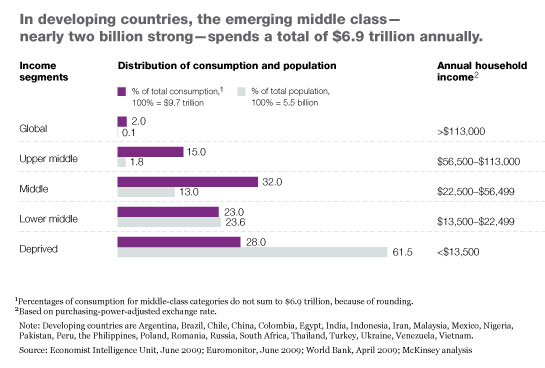

The rapidly growing ranks of middle-class consumers span a dozen emerging nations, not just the fast-growing BRIC countries,1 and include almost two billion people, spending a total of $6.9 trillion annually. Our research suggests that this figure will rise to $20 trillion during the next decade—about twice the current consumption in the United States (Exhibit 1).

These new spenders offer an opportunity for early winners to gain lasting advantages, just as companies in Europe and the United States did at similar points in their development. In 17 product categories in the United States, for example, we found that the market leader in 1925 remained the number-one or number-two player for the rest of the century. These companies include Kraft Foods (Nabisco), which led in biscuits; Del Monte Foods, in canned fruit; and Wrigley, in chewing gum.

Despite having strong global brands, multinational companies face challenging competition in emerging markets, as these economies already boast aggressive local players that have captured a significant portion of spending. Chinese beverage maker Hangzhou Wahaha, for example, has built a $5.2 billion business against global competitors such as Coca-Cola and PepsiCo by targeting rural areas, filling product gaps that meet local needs, keeping costs low, and appealing to patriotism.

Further complicating matters is the fact that the multinationals’ business models are based on practices established in the markets of the developed world, where the game is won slowly by finding cost savings and making product improvements that capture single percentage points of market share over time. Among emerging markets, perhaps only China can provide enough short-term growth to justify that strategy. Meeting the needs of most consumers in emerging markets requires a different course, which often elicits anguished cries in the corridors of the multinationals: “You want me to change my business model and go across the world for $50 million in revenue?” It’s an understandable lament for executives who not only fear ending up with little to show for their efforts but also are wary of the battles already under way among emerging-market champions.

While there are multiple approaches to capturing emerging-market consumers, the two critical factors are speed and scale. Our experience suggests that one way multinationals can quickly gain the scale they need is to identify clusters of similar consumers across multiple markets. That approach allows these companies to build revenue and profit streams that are collectively material and justify significant, ongoing capital investments to fuel growth. Another tack is to work at a more local level, gaining scale in specific regions and categories by teaming up with deeply knowledgeable on-the-ground partners. They can help not only in product development but also in distribution and market positioning—the crucial final steps to reaching highly local consumer markets.

All of this is easier said than done, of course, because consumers in emerging markets are extremely diverse. In some ways, they resemble those in developed nations: they are aware of and have a fondness for brands and want access to a variety of products at different prices, including products they aspire to but can’t currently afford. Yet their tastes are often localized, and while they are middle-class in regional terms,2 they are still not wealthy enough to replace products regularly, because their percentage of truly discretionary income is lower: in China and India, for example, about 40 percent of average household income is spent on food and transportation, compared with 25 percent in the United States.

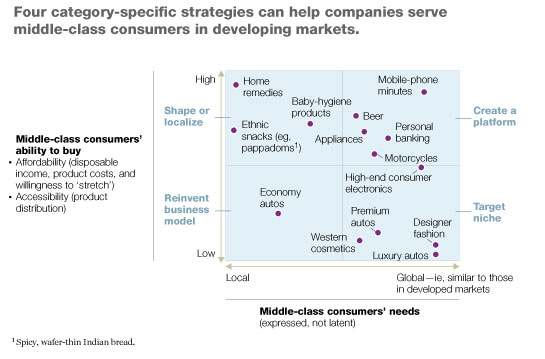

The best way to make sense of this picture is to take a granular view using product categories. For individual categories, multinationals should first identify whether consumer needs in emerging markets are fundamentally global or local. A good proxy for this issue is the similarity of product offerings across geographies, as shown on the horizontal axis of Exhibit 2. Second, multinationals can assess the consumer’s ability to afford a given product. Useful approximations include category penetration and product availability in key developing markets, as well as the willingness of consumers to “stretch” to buy less-affordable products. By developing a perspective on whether and to what extent consumer tastes are global or local and combining that with a clear view on the affordability and accessibility of a given product, multinationals can go a long way toward determining the strategies and business models that will allow them to gain scale quickly.

Identifying consumers with similar needs across markets

The first category, at the top right of the matrix, comprises products and services for which consumer needs are quite similar across geographies and affordability is not a constraint. There is little need to create marketing plans to roll out such products in different countries, one after another: we’ve found that it’s most efficient to identify similar consumer segments across countries and to build scalable business models for each cluster. Examples of products in this category include personal banking, mobile communications, consumer electronics, and pharmaceuticals, which have similar industry structures, rates of consumer adoption, and socioreligious factors across geographies.

A leading multinational retail bank’s marketing team, for example, used longitudinal consumer data to identify five clusters across multiple Asian countries. These segments included one of conservative users very loyal to their local banks (in India, Indonesia, the Philippines, and Taiwan) and another of remote-channel users who were highly price sensitive (in Hong Kong, Singapore, and South Korea). The bank successfully designed and implemented a specific product and channel strategy for each of these five segments across countries.

Targeting premium consumers in product niches

The category on the bottom right of Exhibit 2 comprises emerging-market consumers who have the means to buy products and services that are widely available or even mass market in the developed world. (For the vast majority of the emerging middle class, however, these products and services are neither affordable nor accessible—they are premium items.) While we forecast that less than 3 percent of total emerging-market households will be in this bottom-right category in 2025, their prosperity and the fact that their behavior resembles that of consumers in the developed world has historically made this category appealing to multinationals.

Capturing the loyalty of these consumers and, as they develop new needs, upgrading them is the key. Since emerging-market consumers want value—even in this category—companies should offer products at “mass premium” price points. Consumer electronics manufacturer LG has found that people in many developing markets are more willing to pay for better service than are their counterparts in the developed world. The company launched a premium offering that not only gives consumers a full-time contact person who acts as a go-between with LG and monitors the health of products but also guarantees maintenance visits within 6 hours (compared with the normal 24-hour commitment).

Shaping the market by localizing

The third category, on the top left of the matrix, comprises affordable and accessible products, such as low-cost snacks and highly localized baby-care hygiene products. In this category, there’s clear merit in evaluating how companies can scale up across markets, even if needs are local. One approach is to shape the market through minor product enhancements and sharper positioning that encourages consumers to shift toward more globally convergent offerings over time and allows companies to enjoy greater economies of scale and lower delivery costs. In India, for example, PepsiCo successfully shaped the snack market by creating a new platform, called Kurkure, for younger consumers. The product feels entirely local, though it is packaged and distributed by Frito-Lay.

Other strategies for penetrating this affordable, accessible, and local market are to use celebrity endorsements and to leverage local knowledge, either selectively, in areas such as distribution, or through more comprehensive alliances. The partnership between Norwegian telecommunications company Telenor and Bangladesh’s Grameen Telecom, for example, resulted in the creation, in 1997, of Grameen Phone, now the country’s largest mobile operator.

Reinventing the business model

The final category, on the bottom left of the matrix, represents products and services for which needs are (and will probably remain) very local and affordability is a challenge. In this segment, the potential available market share is high, though the market looks small, since consumers often substitute cheaper products, from adjacent categories, that satisfy similar needs rather than buy a higher-priced global product. The first step for multinationals is to define the market by measuring current total consumption, examining product alternatives that satisfy similar needs, and studying potential spending likely to be unlocked once incomes grow. Companies then need to make their products more affordable and accessible, looking at everything from capital expenditures to product features to distribution. There’s real value in working with local players to drive product, distribution, and sales innovations in that “last mile” before reaching consumers.

Beer manufacturer SABMiller, for example, decided it could not achieve price points that would spur demand in Africa without changing its business model. It retooled its factories for cheaper, locally sourced ingredients (such as cassava and sugar rather than barley and maize) and used local distributors to ensure the availability of its products. The result: lower prices, growing demand, and significant increases in market share across several African countries.

Traditional approaches in which companies enter markets one by one and focus on a handful of brand and market combinations will not meet the challenges of the developing world’s large and growing body of middle-class consumers. Companies need to become adept at building and sharing customer information across markets and more willing to work with others to gain scale quickly. In some regions, such as Africa, multinationals may even need to work with the public and social sector to ensure that consumers have adequate income to generate demand.

Structural changes might also be required. Because multinationals may have to adopt different business models by market, category, and brand, they need flexible and responsive organizations. Cisco, for example, has created a second world headquarters, in India, to spearhead its push into the country, while other companies are establishing centers of excellence to identify, recruit, and develop staff that can be deployed locally. Using local vendors is critical to running a lean operation: many multinationals have found, for example, that capital outlays in emerging markets are often only 30 percent of those required for a factory in the West if they use local resources for plant and process engineering and to execute projects.

Finally, companies need to be aware of perhaps the biggest bottleneck to seizing the emerging middle-class opportunity: talent. Relying excessively on expatriates is likely to stifle an organization’s ability to scale up adequately across markets—there simply won’t be enough staff. We believe that building talent academies inside companies to accelerate leadership development is a good step. Yet the rapid growth in many emerging markets may make traditional “grow your own” or “hire from within” approaches manifestly inadequate to meet staffing needs. By addressing these structural and operational imperatives and identifying the best approaches to achieve the scale needed to serve the growing middle class, multinationals can meet their high expectations for international growth.