Healthcare systems in the United States and Europe are under financial pressure, causing healthcare providers to look for new ways to manage costs while improving the quality of care. Research by McKinsey suggests that in the United States alone there is scope for medical technology companies to work with providers to address these tasks that could be worth $44 billion (Exhibit 1).1 Moreover, a McKinsey survey of 157 hospital executives in the United States and Europe identifies where the opportunities lie, and the obstacles that some med-tech companies will need to overcome to capture them.2

Among the survey’s findings:

Despite early skepticism, there is growing awareness among hospitals of the contribution that partnerships with med-tech companies can make to curtailing costs and improving care. Some 44 percent of respondents have already taken steps toward working more closely with companies, aware of the value of solutions—that is, services that go beyond the purchase of equipment.

There are wide differences in the extent to which different service lines within hospitals use med-tech solutions, as well as in the popularity of different types of solution. For example, many hospitals ask med-tech companies to provide a single service—capital financing or equipment maintenance, say—but relatively few use integrated solutions that combine a product, software, and a service, such as the automated monitoring of sponge use to reduce surgical malpractice.

The survey suggests many hospital executives still shy away from buying in beyond-the-product solutions because they have yet to be persuaded of their value. In the United States, 59 percent of C-level respondents said they were aware of integrated solutions and in Europe 46 percent. Yet in either geography only 21 percent of respondents use them (Exhibit 2).

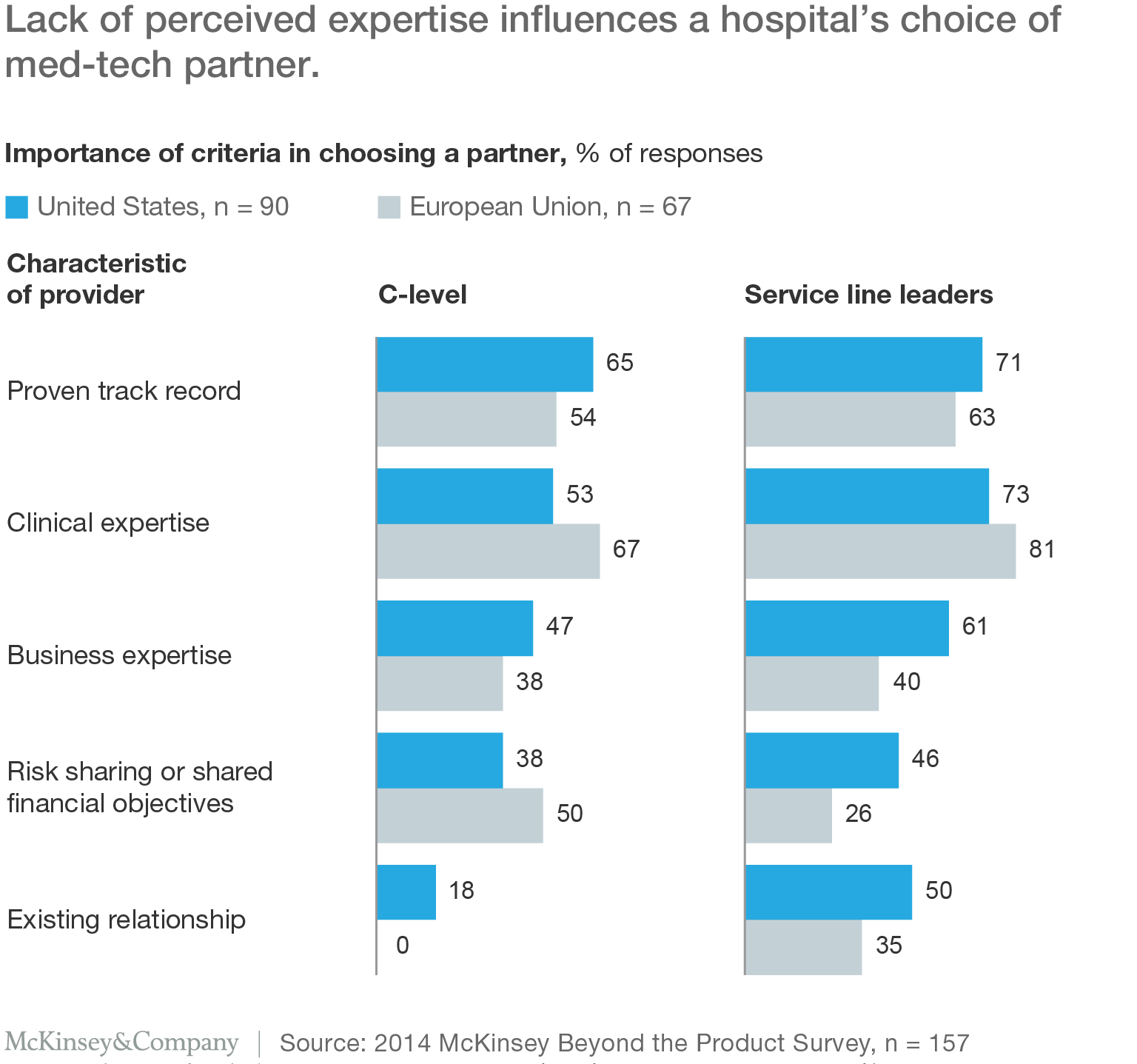

The survey identifies several obstacles that med-tech companies seeking to work more closely with healthcare providers may need to overcome. Building awareness of the value of their solutions is one. Building credibility is another. Fewer than half of respondents ranked the clinical and technical expertise of manufacturers of large equipment as excellent. For suppliers of devices and consumables, that figure falls lower still. And fewer than 20 percent in the US and Europe said large equipment manufacturers understood their business (Exhibit 3).

Contractual arrangements are also important in building credibility. With few exceptions, med-tech companies do not offer to share risk with their hospital customers. They focus on marketing the technical features of their products and price accordingly. Yet providers say they are more willing to work with med-tech partners if they know they share the risks as well as the benefits of the arrangement.

Getting a foot in the door is a further challenge. Expertise and risk-sharing are important, but so is a track record (Exhibit 4). Hospital executives are also influenced by competitors’ choices, particularly in relation to integrated solutions. And size matters. Respondents stated a clear preference for working with larger firms.

Fifty percent or more of the respondents indicated that they are either neutral or dissatisfied with service and solution delivery. This excludes the performance of the service where there were notably higher levels of satisfaction. This is likely due to the fact that there are different representatives for each component of a solution and no key account management (Exhibit 5).

For many companies, removing these obstacles will require new business models. Companies will need to rethink the design of the sales force and the way it operates. They will need to devise new ways of contracting risk and work closely with providers to find ways to measure success and set rewards. They will have to move away from a model that depends on huge clinical trials to test a standard product, toward one that identifies the needs of different customer segments. Med-tech companies will need to become comfortable with new ways to develop solutions for customers by testing and learning through pilot programs, and subsequently optimizing for scale up. And they will have to build new capabilities—not only from the ground up but also through M&A and innovative partnerships with companies in the value chain.