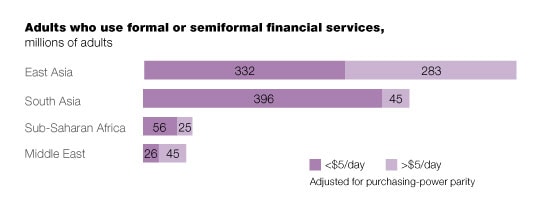

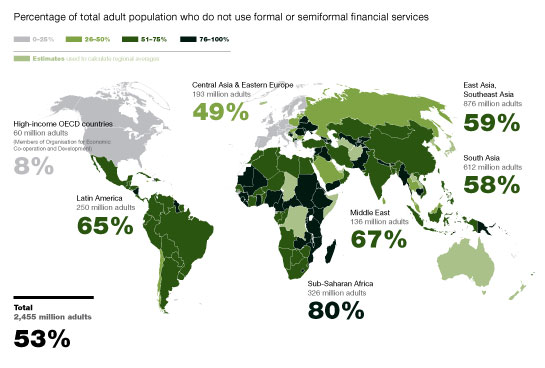

Fully 2.5 billion of the world’s adults don’t use formal banks or semiformal microfinance institutions to save or borrow money, our research finds. Nearly 2.2 billion of these unserved adults live in Africa, Asia, Latin America, and the Middle East. Unserved, however, does not mean unservable. The microfinance movement, for example, has long helped expand credit use among the world’s poor—reaching more than 150 million clients in 2008 alone.1 Similarly, we find that of the approximately 1.2 billion adults in Africa, Asia, and the Middle East who use formal or semiformal credit or savings products, about 800 million live on less than $5 a day (Exhibit 1). Large unserved populations represent opportunities for institutions that are able to offer an innovative range of high-quality, affordable financial products and services. Moreover, with the right financial education and support to make good choices, lower-income consumers will benefit from credit, savings, insurance, and payments products that help them invest in economic opportunities, better manage their money, reduce risks, and plan for the future.

The unbanked are not unservable

Counting the world’s unbanked

Read the full report, Half the World is Unbanked, on McKinsey’s Social Sector page.