The debate about greenhouse gases is heating up. Across a wide spectrum, some voices argue that emissions and climate aren’t linked, while others urge immediate concerted global action to reduce the flow of emissions into the atmosphere. Even the advocates of action disagree about timing, goals, and means. Despite the controversy, one thing is certain: any form of intensified regulation would have profound implications for business.

Our contribution on this topic is not to evaluate the science of climate change or to address the question of whether and how countries around the world should act to reduce emissions. In this article we aim instead to give policy makers, if they choose to act, an understanding of the significance and cost of each possible method of reducing emissions and of the relative importance of different regions and sectors. To that end, we have developed an integrated fact base and related cost curves showing the significance and cost of each available approach, globally and by region and sector. Our other purpose is to help business leaders understand the implications of potential regulatory actions for companies and industries. Indeed, regulation is already on the minds of many executives. A recent survey1 indicates that half of all companies in Europe’s energy-intensive industries regard the European Union’s Emissions Trading Scheme (EU ETS) as one of the primary factors affecting their long-term investment decisions.

As the baseline for our study, we used the “business-as-usual” projections for emissions growth2 from the International Energy Agency (IEA) and the US Environmental Protection Agency (EPA). We then analyzed the significance and cost of each available method of reducing, or “abating,” emissions relative to these business-as-usual projections. Our study3 covers power generation, manufacturing industry (with a focus on steel and cement), transportation, residential and commercial buildings, forestry, and agriculture and waste disposal, in six regions: North America, Western Europe, Eastern Europe (including Russia), other developed countries, China, and other developing nations. It spans three time horizons—2010, 2020, and 2030—and focuses on abatement measures that we estimate would cost 40 euros per ton or less in 2030. Others have conducted more detailed studies on specific industries and geographies. But to our knowledge, this is the first microeconomic investigation of its kind to cover all relevant greenhouse gases, sectors, and regions.

Reading the cost curves

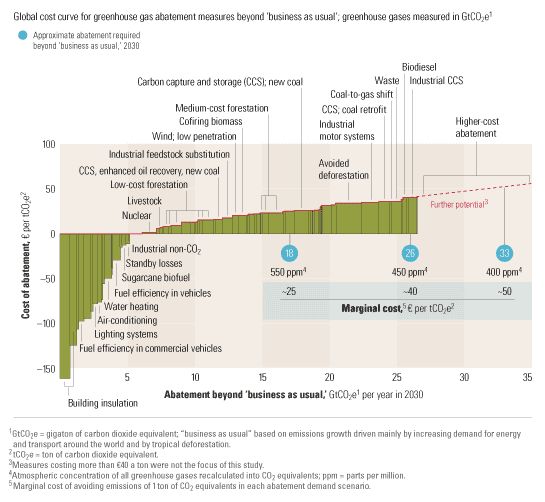

The cost curves we developed show estimates of the prospective annual abatement cost4 in euros per ton of avoided emissions of greenhouse gases,5 as well as the abatement potential of these approaches in gigatons of emissions. The abatement cost for wind power, for example, should be understood as the additional cost of producing electricity with this zero-emission technology instead of the cheaper fossil fuel-based power production it would replace. The abatement potential of wind power is our estimate of the feasible volume of emissions it could eliminate at a cost of 40 euros a ton or less. Looked at another way, these costs can be understood as the price—ultimately, to the global economy—of making any approach to abatement cost competitive or otherwise viable through policy decisions. A wide range of assumptions about the future cost and feasible deployment rates of available abatement measures underlie the estimates of their cost and significance. For example, the significance of wind power assumes that actions to abate greenhouse gases will have already begun across regions by 2008. The volumes in our model (and this article) should be seen as potential abatement, not as forecasts.

Our model for the “supply” of abatement can be compared with any politically determined target (“demand”) for abatement in the years 2010, 2020, and 2030. The science of climate change is beyond the scope of our study and our expertise, however. We thus compare, for illustrative purposes, our findings on supply with three emissions targets discussed in the debate—targets that would, respectively, cap the long-term concentration of greenhouse gases in the atmosphere at 550, 450, or 400 parts per million (a measure of the share of greenhouse gas molecules in the atmosphere). The goal of each target, according to its advocates, is to prevent the average global temperature from rising by more than 2 degrees Celsius. Any of these emissions targets would be challenging to reach by 2030, for they would all require at least a 50 percent improvement in the global economy’s greenhouse gas efficiency (its volume of emissions relative to the size of GDP) compared with business-as-usual trends.

A simplified version of the global cost curve (Exhibit 1) shows our estimates of the significance and cost of feasible abatement measures in 2030—the end year of a period long enough for us to draw meaningful conclusions but short enough to let us make reasonably factual assumptions. We have developed similar cost curves for each sector in each region and for each of the three time frames.

What might it cost?

At the low end of the curve are, for the most part, measures that improve energy efficiency. These measures, such as better insulation in new buildings, thus reduce emissions by lowering demand for power. Higher up the cost curve are approaches for adopting more greenhouse gas-efficient technologies (such as wind power and carbon capture and storage6 ) in power generation and manufacturing industry and for shifting to cleaner industrial processes. The curve also represents ways to reduce emissions by protecting, planting, or replanting tropical forests and by switching to agricultural practices with greater greenhouse gas efficiency.

We have no opinion about the demand for abatement or the probability of concerted global action to pursue any specific goal. But the application of our supply-side research to specific abatement targets can help policy makers and business leaders to understand the economic implications of abatement approaches by region and sector, as well as some of the repercussions for companies and the global economy. Our analysis assumes that the focus would be to capture all of the cheapest forms of abatement around the world but makes no judgment about what ought to be the ultimate distribution of costs. Of course, the ability to pay for reducing emissions varies greatly between developed and developing economies and among individual countries in each group.

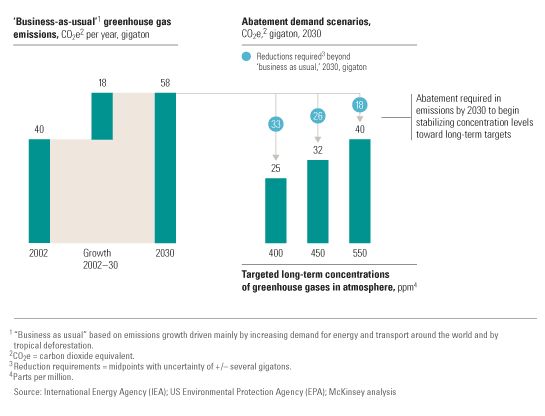

For simplicity’s sake, we compared our cost curve with the 450-parts-per-million scenario—in the midrange of the targets put forward by advocates. This scenario would require greenhouse gases to abate by 26 gigatons a year by 2030 (Exhibit 2). Under that scenario, and assuming that measures are implemented in order of increasing cost, the marginal cost per ton of emissions avoided would be 40 euros. (As a point of reference, since trading under the EU ETS began, in 2005, the price of greenhouse gas emissions has ranged from 6 to 31 euros a ton.)

Three scenarios

We had to make many assumptions about future cost developments for these measures and the practical possibilities for realizing them. We assumed, for instance, that the cost of carbon capture and storage will fall to 20 to 30 euros per ton of emissions in 2030 and that 85 percent of all coal-fired power plants built after 2020 will be equipped with this technology. These assumptions in turn underpin our estimate that it represents 3.1 gigatons of feasible abatement potential.

In a 25-year perspective, such assumptions are clearly debatable, and we make no claim that we are better than others at making them. We believe that the value of our work comes primarily from an integrated view across all sectors, regions, and greenhouse gases using a uniform methodology. This model allows us to assess the relative weight of different approaches, sectors, and regions from a global perspective.

The supply of abatement approaches

Our analysis offers some noteworthy insights. It would be technically possible, for one thing, to capture 26.7 gigatons of abatement by addressing only measures costing no more than 40 euros a ton. But because these lower-cost possibilities are highly fragmented across sectors and regions—for instance, more than half of the potential abatements with a cost of 40 euros a ton or less are located in developing economies—an effective global abatement system would be needed to do so. Politically, this may be very challenging.

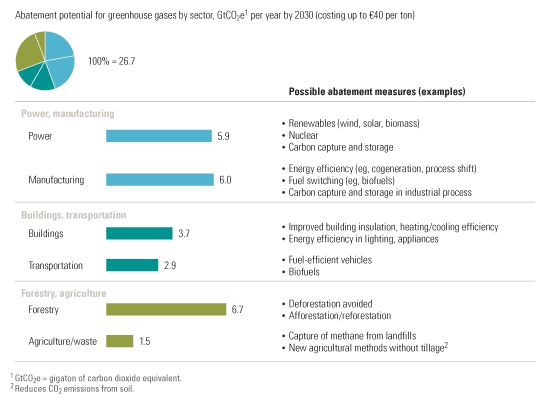

What’s more, power generation and manufacturing industry, so often the primary focus of the climate change debate, account for less than half of the relatively low-cost potential (at a cost of up to 40 euros a ton) for reducing emissions (Exhibit 3). The implication is that if policy makers want to realize abatement measures in order of increasing cost, they must also find ways to effectively address opportunities in transportation, buildings, forestry, and agriculture. This potential is more difficult to capture, as it involves billions of small emitters—often consumers—rather than a limited number of big companies already subject to heavy regulation. Looking at specific measures, nearly one-quarter of the abatement potential at a cost of up to 40 euros a ton involves efficiency-enhancing measures (mainly in the buildings and transportation sectors) that would reduce demand for energy and carry no net cost. The measures we include in this category do not require changes in lifestyle or reduced levels of comfort but would force policy makers to address existing market imperfections by aligning the incentives of companies and consumers.

Abatement potential

Further, we found a strong correlation between economic growth and the ability to implement low-cost measures to reduce emissions, for it is cheaper to apply clean or energy-efficient technologies when building a new power plant, house, or car than to retrofit an old one. Finally, in a 2030 perspective, almost three-quarters of the potential to reduce emissions comes from measures that are either independent of technology or rely on mature rather than new technologies.

The role of developing economies

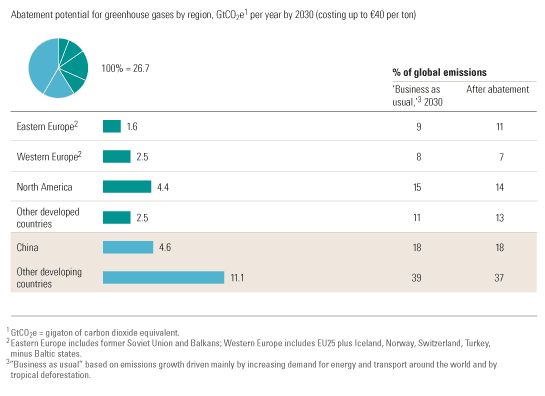

Even though developed economies emit substantially more greenhouse gases relative to the population than developing ones, we found that the latter account for more than half of the total abatement potential at a cost of no more than 40 euros a ton. Developing economies have such a high share for three reasons: their large populations, the lower cost of abating new growth as opposed to reducing existing emissions (especially in manufacturing industry and power generation of high-cost developed markets), and the fact that tropical countries have much of the potential to avoid emissions in forestry for 40 euros a ton or less (Exhibit 4).

Developing economies will play an important role

Forestry measures—protecting, planting, and replanting forests—make up 6.7 gigatons of the overall 26.7 gigatons of the potential abatement at a cost up to 40 euros per ton.7 We estimate that for no more than 40 euros a ton, tropical deforestation rates could be reduced by 50 percent in Africa and by 75 percent in Latin America, for example, and that this effort could generate nearly 3 gigatons of annual abatement by 2030. Major abatements in Asia’s forests would cost more, since land is scarce and commercial logging has a higher opportunity cost than subsistence farming in Africa and commercial agriculture in Latin America.

In agriculture and waste disposal, which produce greenhouse gases such as methane and nitrous oxide, developing economies also represent more than half of the 1.5 gigatons of possible abatements costing no more than 40 euros a ton. Abatement measures in this sector would include shifting to fertilization and tillage techniques that generate fewer emissions and capturing methane from landfills.

Reducing growth in energy demand

An additional 6 gigatons—almost a quarter of the total abatement potential at a cost of 40 euros a ton or less—could be gained through measures with a zero or negative net life cycle cost. This potential appears mainly in transportation and in buildings. Improving the insulation of new ones, for example, would lower demand for energy to heat them and thus reduce emissions. Lower energy bills would more than compensate for the additional insulation costs. According to our model, measures like these, as well as some in manufacturing industry, hold the potential to almost halve future growth in global electricity demand, to approximately 1.3 percent a year, from 2.5 percent.

As for measures that would have a net cost, we found that around 35 percent of all potential abatements with a net cost of up to 40 euros a ton involve forestry; 28 percent, manufacturing industry; 25 percent, the power sector; 6 percent, agriculture; and 6 percent, transportation.

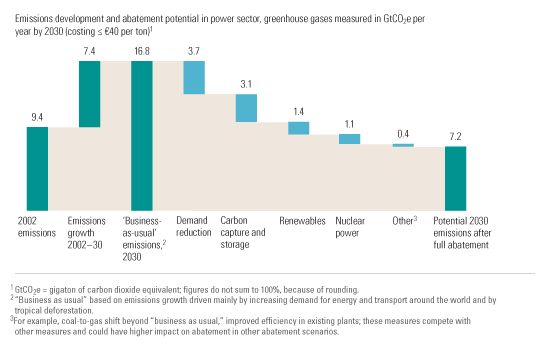

A power perspective

The power sector represented 9.4 gigatons, or 24 percent, of global greenhouse gas emissions in 2002, the latest year that consistent global figures are available across all sectors. In the IEA’s business-as-usual scenario, emissions from power generation will increase to 16.8 gigatons a year in 2030 as a result of a doubling of global electricity demand. Five key groups of abatement measures costing 40 euros a ton or less are relevant to the power sector: reducing demand, carbon capture and storage, renewables, nuclear power, and improving the greenhouse gas efficiency of fossil fuel plants. Combined, these measures hold the potential to reduce the power sector’s total emissions to 7.2 gigatons by 2030 (Exhibit 5).

Abatement potential in the power sector

Among power generation technologies, nuclear (at 0 to 5 euros a ton for avoided emissions) is the cheapest source of abatement and nearly cost competitive with power generated by fossil fuels. We estimate that abatements from carbon capture and storage could cost 20 to 30 euros a ton by 2030; those from wind power could average around 20 euros a ton, with a wide cost range depending on the location and on the previous penetration of weather-dependent electricity sources. In our model, the overall additional cost to the power sector of achieving the target of 450 parts per million, compared with the business-as-usual scenario, would be around 120 billion euros annually in 2030. This figure illustrates the very significant potential implications, for companies in the power sector, of any further actions that regulators may take to reduce greenhouse gas emissions.

Addressing the abatement potential described above would likely create a major shift from traditional coal and gas power generation to coal plants with carbon capture and storage, to renewables, and to nuclear power. In our model, coal-fired plants using carbon capture and storage would increase their share of the world’s power generation capacity from nothing in 2002 to 17 percent by 2030; renewables (including a big but slow-growing share for large-scale hydropower), to 32 percent, from 18 percent; and nuclear power, to 21 percent, from 17 percent. Fossil fuel power generated without carbon capture and storage would decrease to 30 percent, from 65 percent.

Low-tech abatement

The role of technology in reducing emissions is much debated. We found that some 70 percent of the possible abatements at a cost below or equal to 40 euros a ton would not depend on any major technological developments. These measures either involve very little technology (for example, those in forestry or agriculture) or rely primarily on mature technologies, such as nuclear power, small-scale hydropower, and energy-efficient lighting. The remaining 30 percent of abatements depend on new technologies or significantly lower costs for existing ones, such as carbon capture and storage, biofuels, wind power, and solar panels. The point is not that technological R&D has no importance for abatement but rather that low-tech abatement is important in a 2030 perspective.

What are the implications?

Our analysis has revealed a number of important implications for each sector and region, should regulators choose to reduce emissions. We summarize the primary overall conclusions below.

Costs for reducing emissions

For the global economy, the cost of the 450-parts-per-million scenario described in this article would depend on the ability to capture all of the available abatement potential that costs up to 40 euros a ton. If that happens, our cost curve indicates that the annual worldwide cost could be around 500 billion euros in 2030, 0.6 percent of that year’s projected GDP. However, should more expensive approaches be required to reach the abatement goal, the cost could be as high as 1,100 billion euros, 1.4 percent of global GDP.

If, as some participants in the climate debate argue, the cost of reducing emissions could be an insurance policy against the potentially severe consequences of unchecked emissions in the future, it might be relevant to compare the costs with the global insurance industry’s turnover (excluding life insurance)—some 3.3 percent of global GDP in 2005.

Cost-conscious regulation

Should regulators choose to step up current programs to reduce greenhouse gas emissions, they should bear in mind four types of measures to restrain costs:

1. Ensuring strict technical standards and rules for the energy efficiency of buildings and vehicles

2. Establishing stable long-term incentives to encourage power producers and industrial companies to develop and deploy greenhouse gas-efficient technologies

3. Providing sufficient incentives and support to improve the cost efficiency of selected key technologies, including carbon capture and storage

4. Ensuring that the potential in forestry and agriculture is addressed effectively, primarily in developing countries; such a system would need to be closely linked to their overall development agenda

Shifting business environment

For companies in the power sector and energy-intensive industries, heightened greenhouse gas regulation would mean a shift in the global business environment on the same order of magnitude as the one launched by the oil crisis of the 1970s. It would have a fundamental impact on key issues of business strategy, such as production economics, cost competitiveness, investment decisions, and the value of different types of assets. Companies in these industries would therefore be wise to think through the effects of different types of greenhouse gas regulation, strive to shape it, and position themselves accordingly.

No matter whether, how, or when countries around the globe act to reduce greenhouse gas emissions, policy makers and business leaders can benefit from a thorough understanding of the relative economics of different possible approaches to abatement, as well as their implications for business and the global economy.

For an updated version of the global greenhouse gas abatement curve in this article, see Impact of the financial crisis on carbon economics: Version 2.1 of the global greenhouse gas abatement cost curve.

Related Articles