Aggressive valuations among technology companies are hardly a new phenomenon. The widespread concerns over high pre-IPO valuations today recall debates over the technology bubble at the turn of the century—which also extended to the media and telecommunications sectors. A sharp decline in the venture-capital funding for US-based companies in the first quarter of the year feeds into that debate,1 though the number of “unicorns”—start-up companies valued at more than a billion dollars—over that same period continued to rise.

The existence of these unicorns is just one significant difference between 2000 and 2016. Until seven years ago, no venture capital–backed company had ever achieved a billion-dollar valuation before going public, let alone the $10 billion valuation of 14 current “deca-corns.” Also noteworthy is the fact that high valuations predominate among private, pre-IPO companies, rather than public ones, as was the case at the turn of the millennium. And then there’s the global dimension: innovation and growth in the Chinese tech sector are much bigger forces today than they were in 2000.2

All of these factors suggest that when the curtain comes down on the current drama, the consequences are likely to look quite different from those of 16 years ago. Although the underlying economic changes taking place during this cycle are no less significant than the ones during the last cycle, valuations of public-market tech companies are, at this writing, mostly reasonable—perhaps even slightly low by historical standards. A slump in current private-sector valuations would be unlikely to have much impact on the broader public markets. And the market dynamics in China and the United States are far from similar. In this article, we’ll elaborate on the fundamentals at work, which extend beyond the strength of the current pipeline of pre-IPO tech companies, and on the funds that have washed over the venture-capital industry in recent years.

The lessons of history

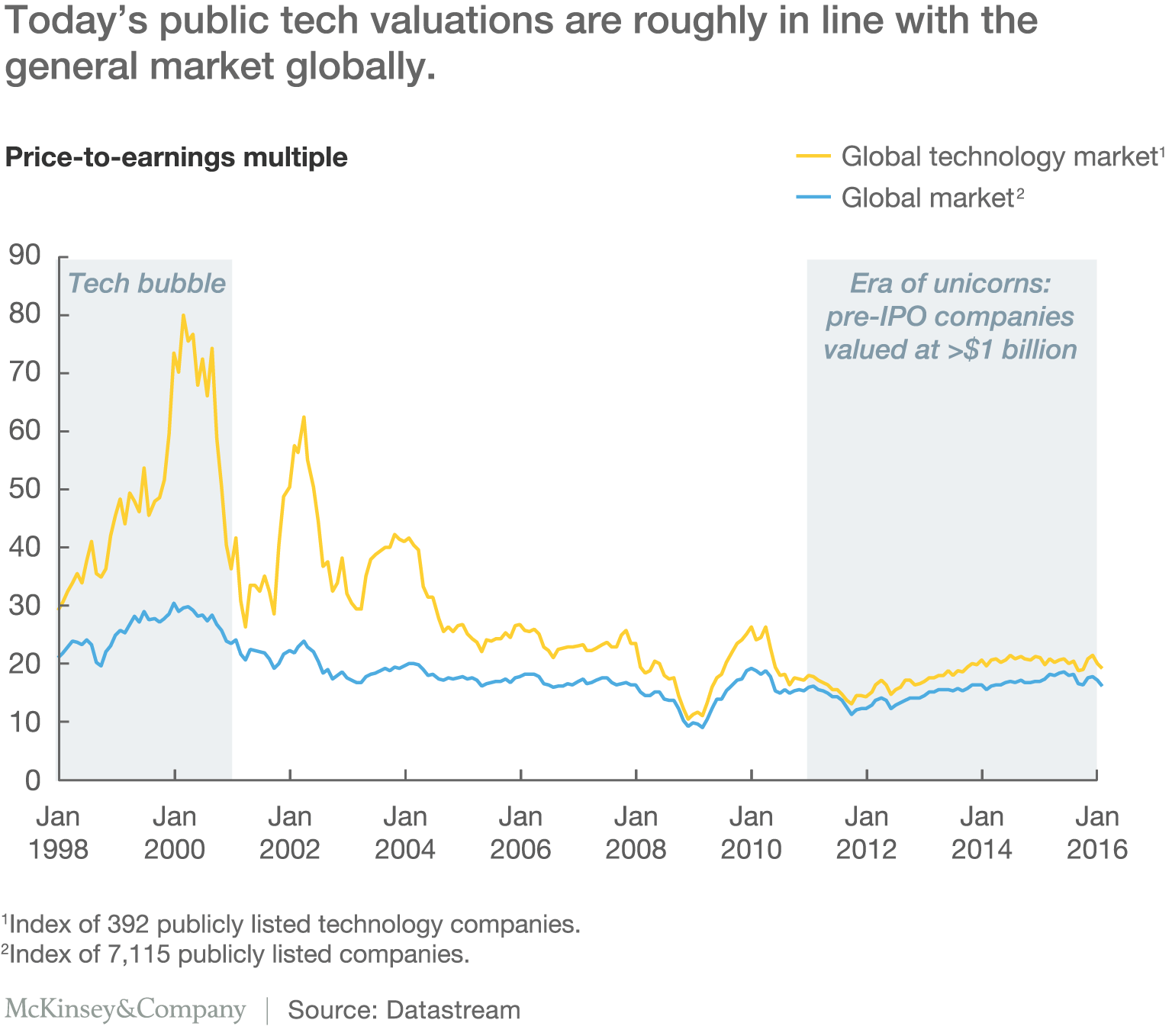

The defining feature of the 2000 tech bubble was that it was a public-market bubble. At the start of 1998, valuations for tech companies were 40 percent higher than for the general market: at the peak of the bubble in early 2000, they were 165 percent higher. However, at that point the largest-ever venture-invested tech start-up we could find evidence of barely exceeded a $6 billion valuation at IPO—a small number by today’s standards. Moreover, a considerable part of the run-up in valuation came not from Internet companies but from old-school telecom companies, which saw the sector’s total value grow by more than 250 percent between 1997 and 2000.

Would you like to learn more about our Strategy & Corporate Finance Practice?

Equity markets seem to have learned from that episode. In aggregate, publicly held tech companies in 2015 showed little if any sign of excess valuations, despite the steadily escalating ticket size of the IPOs. Valuations of public tech companies in 2015 averaged 20 times earnings, only 10 percent above the general market, and they have been relatively stable at those levels since 2010.

By historical standards, that’s relatively low: over the past two decades, tech companies on average commanded a 25 percent valuation premium, often much more. During the technology and telecommunications bubble of 2000, the global tech-sector valuation peaked at just under 80 times earnings, more than 3 times the valuation of nontech equities. And over the five years after the bubble burst in 2001, the tech sector enjoyed a valuation premium of, on average, 50 percent over the rest of the equity market (exhibit). Even with a focus limited to Internet companies—the sector most often suspected of runaway valuations—there is no obvious bubble among public companies at present.

Nor do these companies’ valuation premiums appear excessive to the general market when viewed in the light of their growth expectations. Higher multiples are in most cases explained by higher consensus forecasts for earnings growth and margins. The market could be wrong in these expectations, but at least it is consistent.

China is a notable exception, though equity valuations in China always need to be viewed with caution. Before 2008, Chinese tech companies were valued on average at a 50 to 60 percent premium over the general market. Since then, that premium has grown to around 190 percent. Why? In part because the Chinese online market is both larger and faster growing than the United States, and the government has ambitious plans to localize the higher-value parts of the hardware value chain over the next few years.3 The growth in China’s nonstate-owned sector is another part of the story. Many of the new technology companies coming to the market in the past five years have been nonstate-owned, and nonstate-owned companies are consistently valued 50 percent to 100 percent higher than their state-owned peers in the same segments.

This time, it’s different?

Where the picture today is most different from 2000 is in the private capital markets, and in how companies approach going public.

It wasn’t until 2009 that a pre-IPO company reached a $1 billion valuation. The majority of today’s unicorn companies reached that valuation level in just the past 18 months. They move in a few distinct herds: roughly 35 percent of them are in the San Francisco Bay area, 20 percent are in China, and another 15 percent are on the US East Coast.

Notable shifts in funding and valuations have accompanied the rising number of these companies. The number of rounds of pre-IPO funding has increased, and the average size of venture investments more than doubled between 2013 and 2015, which saw both the highest average deal size and highest number of deals ever recorded. Increases in valuation between rounds of funding have also been dramatic: it’s not unusual to see funding rounds for Chinese companies involving valuation increases of up to five times over a period of less than a year.

Whatever the quality of new business models emerging in the technology sector, what’s unmistakable is that the venture-capital industry has built up an unprecedented supply of cash. The amount of uninvested but committed funds in the industry globally rose from just over $100 billion in 2012 to nearly $150 billion in 2015, the highest level ever. And where buyout, real-estate, and special-situations funds all have the luxury of looking across a range of deal sizes, industries, or even asset classes, venture capitalists have less flexibility. Many venture funds fish in the same pool of potential deals, and some only within their geographic backyard.

The liquidity in the venture-capital industry has been augmented by the entry of a new set of investors, with limited partners in some funds looking for direct investment opportunities into venture-funded companies as they approach IPO. This allows companies to do much larger pre-IPO funding rounds, marketed directly to institutional investors and high-net-worth individuals. These investors dwarf the venture-capital industry in scale and can therefore extend the runway before IPO, though not indefinitely: their participation is contingent on the promise of an eventual exit via IPO or sale.

Thus valuations of individual pre-IPO start-ups need to be viewed cautiously, as the actual returns their venture-capital investors earn flow as much from protections built into the deal terms as by the valuation number itself. In a down round (when later-stage investors come in at a lower valuation than the previous round), these terms become critical in determining how the pie is divided among the different investors.

The IPO hurdle

Private-equity markets do not exist in isolation from public markets: with few exceptions, the companies venture capitalists invest in must eventually list on public exchanges, or be sold to a listed company. The current disconnect between valuations in these two markets will somehow be resolved, either gradually, through a long series of lower-priced IPOs, or suddenly, in a massive slump in pre-IPO valuations.

Several factors incline toward the former. Some late-stage investors, such as Fidelity and T. Rowe Price, have already marked down their investments in multiple unicorns, and it’s increasingly common for start-up IPOs to raise less capital than their pre-IPO valuations. Given the still-lofty level of those valuations, this no longer attracts the extreme stigma that it did in 2000. Regardless of how the profits divide up, the company is still independent and now listed.

Tech companies also are staying private for, on average, three times longer.4 A much greater share of companies wait until they are making accounting profits before coming to market. From 2001 to 2008, fewer than 10 percent of tech IPOs were launched after the company had reached profitability: since 2010, almost 50 percent had reached at least the break-even point. The number of companies coming to market has remained relatively flat since the 1990s technology bubble. But the average capitalization at IPO time has more than doubled in the past five years, reflecting the fact that the companies making public offerings are larger and more mature.

What happens post-IPO? Over the past three years, 61 tech companies have gone public with a market cap of more than $1 billion. The median company in this group is now trading just 3 percent above its listing price. The valuations of a number of former unicorns are lower still, including well-known companies like Twitter in the United States and Alibaba in China.

Valuing high-tech companies

History paints a challenging picture for many of these recently listed companies. Between 1997 and 2000, there were 898 IPOs of technology companies in the United States, valued collectively at around $171 billion. The attrition among this group was brutal. By 2005, only 303 of them remained public. By 2010, that number had declined to 128. In the decade from 2000 to 2010, the survivors among these millennials had an average share-price return of –3.7 percent a year. In the subsequent five years, they returned only –0.8 percent per annum—despite soaring equity markets.

The geographic dimension

The current crop of pre-IPO companies is far more diverse than in 2000. It will be particularly interesting to see which of the two largest geographic groups—the US and the Chinese unicorns—weathers the shakeout best. Consider just Internet companies. The total market value of listed Internet companies today is around $1.5 trillion. Of this, US companies represent nearly two-thirds, and Chinese companies—mostly listed in the United States—almost all of the remainder. The rest of the world put together amounts to less than 5 percent.

The differences between the unicorns in these regions are revealing. Of the more than 100 unicorns operating in the United States and China, only 14 have overlapping investors, and just two—the electronics company Xiaomi and the transportation-network company Didi Chuxing (formerly Didi Kuaidi)—account for two-thirds of the combined valuation of all of them. Three-quarters of the Chinese unicorns are primarily in the online space, compared with less than half of the US unicorns, and these serve separate user bases as a result of regulatory separation of the two countries’ Internet markets.

It is not obvious which group holds the advantage. The local market to which Chinese Internet companies have access is substantial, with well over twice as many users as in the United States; the e-commerce market is significantly larger and growing almost three times as fast. Moreover, the three Chinese Internet giants, Baidu, Alibaba, and Tencent, have invested in many of the Chinese unicorns, giving them easier access to a platform of hundreds of millions of users on which to operate.

The Chinese unicorns also have a much higher proportion of “intermediary” companies—start-ups that act primarily as channels or resellers of other companies’ services and take a cut of earnings. Around a third of the Chinese unicorns have business models of this kind, compared with only one in eight of their US counterparts. Finally, the US start-ups tend to adapt faster to a global audience. Although there are several established Chinese technology companies that have successfully made the leap to the global stage, such as Huawei, Lenovo, and ZTE, very few of the companies founded in the past five years have reached that point.

For all the differences between the tech start-up markets of today and those of 2000, both periods are marked by excitement at the potential for new technologies and businesses to stimulate meaningful economic change. To the extent that valuations are excessive, the private markets would appear to be more vulnerable. But perspective is important. The market capitalization of the US and Chinese equity markets declined by $2.5 trillion in January alone. Any correction to the roughly half a trillion dollars in combined value of all the unicorns as of their last funding round is likely to seem milder than the correction of the last technology bubble.

Related Articles

Valuing high-tech companies