At few moments since the end of World War II has downward pressure on prices been so great. Some of it stems from cyclical factors—such as sluggish economic growth in the Western economies and Japan—that have reined in consumer spending. There are newer sources as well: the vastly increased purchasing power of retailers, such as Wal-Mart, which can therefore pressure suppliers; the Internet, which adds to the transparency of markets by making it easier to compare prices; and the role of China and other burgeoning industrial powers whose low labor costs have driven down prices for manufactured goods. The one-two punch of cyclical and newer factors has eroded corporate pricing power and forced frustrated managers to look in every direction for ways to hold the line.

In such an environment, managers might think it mad to talk about raising prices. Yet nothing could be further from the truth. We are not talking about raising prices across the board; quite often, the most effective path is to get prices right for one customer, one transaction at a time, and to capture more of the price that you already, in theory, charge. In this sense, there is room for price increases or at least price stability even in today's difficult markets.

Such an approach to pricing—transaction pricing, one of the three levels of price management (see sidebar "Pricing at three levels")—was first described ten years ago.1 The idea was to figure out the real price you charged customers after accounting for a host of discounts, allowances, rebates, and other deductions. Only then could you determine how much money, if any, you were making and whether you were charging the right price for each customer and transaction.

A simple but powerful tool—the pocket price waterfall, which shows how much revenue companies really keep from each of their transactions—helps them diagnose and capture opportunities in transaction pricing. In this article, we revisit that tool to see how it has held up through dramatic changes in the way businesses work and in the broader economy. Our experience serving hundreds of companies on pricing issues shows that the pocket price waterfall still effectively helps identify transaction-pricing opportunities. Nevertheless, in view of evolving business practice, we have greatly expanded the tool's application. The increase in the number of companies selling customized products and solutions or bundling service packages with each sale, for instance, means that assessing the profitability of transactions has become much more complex. The pocket price waterfall has evolved over time to take account of this transition.

Today, it is more critical than ever for managers to focus on transaction pricing; they can no longer rely on the double-digit annual sales growth and rich margins of the 1990s to overshadow pricing shortfalls. Moreover, at many companies, little cost-cutting juice can easily be extracted from operations. Pricing is therefore one of the few untapped levers to boost earnings, and companies that start now will be in a good position to profit fully from the next upturn.

Advancing one percentage point at a time

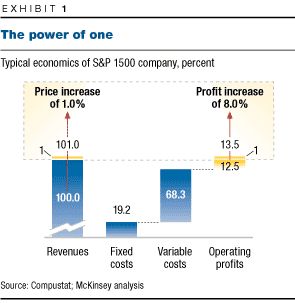

Pricing right is the fastest and most effective way for managers to increase profits. Consider the average income statement of an S&P 1500 company: a price rise of 1 percent, if volumes remained stable, would generate an 8 percent increase in operating profits (Exhibit 1)—an impact nearly 50 percent greater than that of a 1 percent fall in variable costs such as materials and direct labor and more than three times greater than the impact of a 1 percent increase in volume.

Unfortunately, the sword of pricing cuts both ways. A decrease of 1 percent in average prices has the opposite effect, bringing down operating profits by that same 8 percent if other factors remain steady. Managers may hope that higher volumes will compensate for revenues lost from lower prices and thereby raise profits, but this rarely happens; to continue our examination of typical S&P 1500 economics, volumes would have to rise by 18.7 percent just to offset the profit impact of a 5 percent price cut. Such demand sensitivity to price cuts is extremely rare. A strategy based on cutting prices to increase volumes and, as a result, to raise profits is generally doomed to failure in almost every market and industry.

Following the pocket price waterfall

Many companies can find an additional 1 percent or more in prices by carefully looking at what part of the list price of a product or service is actually pocketed from each transaction. Right pricing is a more subtle game than setting list prices or even tracking invoice prices. Significant amounts of money can leak away from list or base prices as customers receive discounts, incentives, promotions, and other giveaways to seal contracts and maintain volumes (see sidebar "A hole in your pocket").

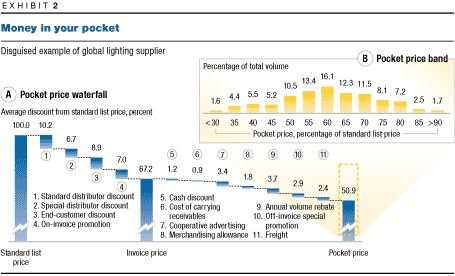

The experience of a global lighting supplier shows how the pocket price—what remains after all discounts and other incentives have been tallied—is usually much lower than the list or invoice price. This company made incandescent lightbulbs and fluorescent lights sold to distributors that then resold them for use in offices, factories, stores, and other commercial buildings. Every lightbulb had a standard list price, but a series of discounts that were itemized on each invoice pushed average invoice prices 32.8 percent lower than the standard list prices. These on-invoice deductions included the standard discounts given to most distributors as well as special discounts for selected ones, discounts for large-volume customers, and discounts offered during promotions.

Managers who oversee pricing often focus on invoice prices, which are readily available, but the real pricing story goes much further. Revenue leaks beyond invoice prices aren't detailed on invoices. The many off-invoice leakages at the lighting company included cash discounts for prompt payment, the cost of carrying accounts receivable, cooperative advertising allowances, rebates based on a distributor's total annual volume, off-invoice promotional programs, and freight expenses. In the end, the company's average pocket price—including 16.3 percentage points in revenue reductions that didn't appear on invoices—was about half of the standard list price (Exhibit 2a). Over the past decade, companies have tried to entice buyers with a growing number of discounts, including discounts for on-line orders as well as the increasingly popular performance penalties that require companies to provide a discount if they fail to meet specific performance commitments such as on-time delivery and order fill rates.

By consciously and assiduously managing all elements of the pocket price waterfall, companies can often find and capture an additional 1 percent or more in their realized prices. Indeed, an adjustment of any discount or element along the waterfall—either on- or off-invoice—is capable of improving prices on a transaction-by-transaction basis.

Embracing a wide band

The pocket price waterfall is often first created as an average of all transactions. But the amount and type of the discounts offered may differ from customer to customer and even order to order, so pocket prices can vary a good deal. We call the distribution of sales volumes over this range of variation the pocket price band.

At the lighting company, some bulbs were sold at a pocket price of less than 30 percent of the standard list price, others at 90 percent or more—three times higher than those of the lowest-priced transactions (Exhibit 2b). This range may seem spectacular, but it is not very unusual. In our work, we have seen pocket price bands in which the highest pocket price was five or six times greater than the lowest.

It would be a mistake, though, to assume that wide pocket price bands are necessarily bad. A wide band shows that neither all customers nor all competitive situations are the same—that for a whole host of reasons, some customers generate much higher pocket prices than do others. When a band is wide, small changes in its shape can readily move the average price a percentage point or more higher. If a manager can increase sales slightly at the high end of the band while improving or even dropping transactions at the low end, such an increase comes within reach. But when the price band is narrow, the manager has less room to maneuver; changing its shape becomes more difficult; and any move has less impact on average prices.

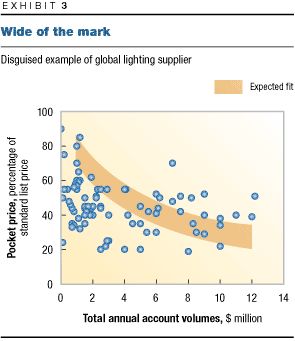

Although the lighting company was surprised by the width of its pocket price band, it had a quick explanation: the range resulted from a conscious effort to reward high-volume customers with deeper discounts, which in theory were justified not only by the desire to court such customers but also by a lower cost to serve them. A closer examination showed that this explanation was actually wide of the mark (Exhibit 3): many large customers received relatively modest discounts, resulting in high pocket prices, while a lot of small buyers got much greater discounts and lower pocket prices than their size would warrant. A few smaller customers received large discounts in special circumstances—unusually competitive or depressed markets, for instance—but most just had long-standing ties to the company and knew which employees to call for extra discounts, additional time to pay, or more promotional money. These experienced customers were working the pocket price waterfall to their advantage.

The lighting company attacked the problem from three directions. First, it instructed its sales force to bring into line—or drop—the smaller distributors getting unacceptably high discounts. Within 12 months, 85 percent of these accounts were being priced and serviced in a more appropriate way, and new accounts had replaced most of the remainder. Second, the company launched an intensive program to stimulate sales at larger accounts for which higher pocket prices had been realized. Finally, it controlled transaction prices by initiating stricter rules on discounting and by installing IT systems that could track pocket prices more effectively. In the first year thereafter, the average pocket price rose by 3.6 percent and operating profits by 51 percent.

In addition to these immediate fixes, the lighting company took longer-term measures to change the relationship between pocket prices and the characteristics of its accounts. New and explicit pocket price targets were based on the size, type, and segment of each account, and whenever a customer's prices were renegotiated or a new customer was signed, that target guided the negotiations.

Pocket margins become more relevant

For companies that not only sell standard products and services but also experience little variation in the cost of selling and delivering them to different customers, pocket prices are an adequate measure of price performance. Today, however, as companies seek to differentiate themselves amid growing competition, many are offering customized products, bundling product and service packages with each sale, offering unique solutions packages, or providing unique forms of logistical and technical support. Pocket prices don't capture these different product costs or the cost to serve specific customers. For such companies, another level of analysis—the pocket margin—is needed to reflect the varying costs associated with each order. The pocket margin for a transaction is calculated by subtracting from the pocket price any direct product costs and costs incurred specifically to serve an individual account.

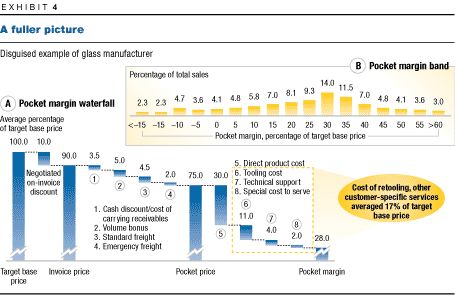

One North American company, which manufactures tempered glass for heavy trucks and for farm and construction machinery, sharply increased its profits by understanding and actively managing its pocket margins. Each piece of the company's glass was custom-designed for a specific customer, so costs varied transaction by transaction. Other costs differed from customer to customer as well. The company's glass, for example, was frequently shipped in special containers that were designed to be compatible with the customers' assembly machines. The costs of retooling and other customer-specific services varied widely from case to case but averaged no less than 17 percent of the target base price (Exhibit 4a).

As with pocket prices, a fuller picture emerges when a company examines each account and creates a pocket margin band. The glass company's pocket margins ranged from more than 60 percent of base prices to a loss of more than 15 percent of base prices (Exhibit 4b). When fixed costs were allocated, the company found that it required a pocket margin of at least 12 percent just to break even at the current operating level. More than a quarter of the company's sales fell below this threshold.

Traditionally, the pricing policies of the glass company had focused on invoice prices and standard product costs; it paid little attention to off-invoice discounts or extra costs to serve specific customers. The pocket margin band helped it identify which individual customers were more profitable and which should be approached more aggressively even at the risk of losing their business. The company also uncovered narrowly defined customer segments (for example, medium-volume buyers of flat or single-bend door glass) that were concentrated at the high end of the margin band. In addition, it evaluated its policies for some of the more standard waterfall elements to ensure that it had clear objectives, accountability, and controls for each of them—for instance, it decided to base volume bonuses on stretch performance targets and to charge for last-minute technical support. By focusing on and increasing sales in profitable subsegments, pruning less attractive accounts, and making selective policy changes across the waterfall elements, the company pushed up its average pocket margin by 4 percent and its operating profits by 60 percent within a year.

Taming transactions

The game of transaction pricing is won or lost in hundreds, sometimes thousands, of individual decisions each day. Standard and discretionary discounts allow percentage points of revenue to drop from the table one transaction at a time. Companies are often poorly equipped to track these losses, especially for off-invoice items; after all, the volumes and complexity of transactions can be overwhelming, and many items, such as cooperative advertising or freight allowances, are accounted for after the fact or on a company-wide basis. Even if managers wanted to track transaction pricing, it has often been impossible to get the data for specific customers or transactions. But some recent technical advances have helped remove this obstacle; enterprise-management-information systems and off-the-shelf custom-pricing software have made it easier to keep tabs on transaction pricing. Managers can no longer hide behind the excuse that gathering the data is too difficult.

Current price pressures should go a long way toward removing two other obstacles: will and skill. In the booming economy of the 1990s, robust demand and cost-cutting programs, which drove up corporate earnings, made too many managers pay too little attention to pricing. But now that a global economic downturn has slowed growth and the easiest cost cutting has already occurred, the shortfall in pricing capabilities has been exposed. A large number of companies still don't understand the untapped opportunity that superior transaction pricing represents. For many companies, getting it right may be one of the keys to surviving the current downturn and to flourishing when the upturn arrives. It has never been more crucial—or more possible—to learn and apply the skills needed to execute superior transaction-price management.

Related Articles