Several years ago, something interesting happened in the infrastructure software sector: IBM and a number of other companies pledged some of their own patents to the public to create IP-free zones in parts of the value chain. They did so when a 2004 report showed that Linux, the open-source operating system that had emerged as a viable, low-cost alternative to established operating systems, such as Microsoft Windows and Unix, was inadvertently infringing on more than 250 patents.1 By voluntarily pledging not to enforce hundreds of IBM’s own patents so long as users of the IP were pursuing only open-source purposes, the company led the creation of an alliance of patent holders dependent on (and willing to defend) open-source software against lawsuits.2 One result: IBM substantially increased the share of its new products based on Linux.

This example seems specialized and unusual; after all, who would give away patents to make more money from innovation? But as open-source innovation, “crowd sourcing,” and engaging with open communities become increasingly prevalent, could IP-free zones appear in the competitive landscape of other industries? Having studied the case of infrastructure software closely,3 we believe executives can gain some insight into this possibility by asking three questions that underpin the logic of competing by protecting the open space—open competition, as you might call it:

Do specialized firms offer proprietary solutions within certain layers of my industry’s value chain?

Do integrated firms seek to cut development costs in my industry by drawing on open technologies to substitute for these proprietary solutions?

Are the underlying technologies complex—consisting of so many bits and pieces that a significant number could inadvertently infringe on proprietary IP held by specialized firms?

The more affirmative the answers to these questions may be, the more likely it is that the interests of specialized vendors of proprietary solutions will collide with those of firms drawing on open innovation, which could involve any type of open good, from software to the genetic code to crowd-sourced designs for parts or tools. That’s because if the answer to question 1 were yes, specialized firms would stand to lose business if integrated firms (question 2) cut them out of parts of the business. And the more complex the technologies are (question 3), the more likely it is that competitive offerings of specialized and integrated firms will overlap and, in turn, that specialized firms will choose to defend their IP.

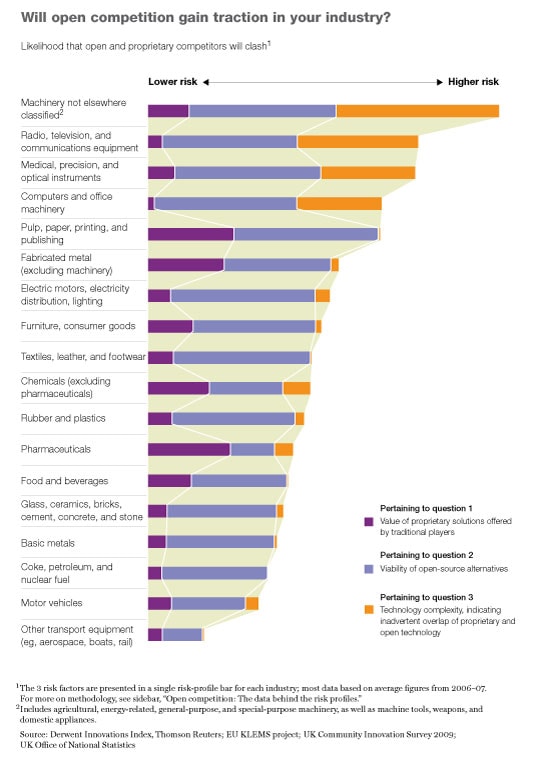

While some executives will find it easy to answer these questions, others will be in less comfortable terrain. To give the latter food for thought, we assembled publicly available EU and UK data to approximate the likelihood that adopters of open innovation could, at some point, clash with proprietary firms in a given industry unless they took precautions (exhibit). Specifically, we sought proxies for the amount of economic surplus available and the number of private players going after it in different industries, for the viability and attractiveness of alternative open solutions that could redistribute some of that value, and for the technological complexity that’s a precondition of the inadvertent overlap of proprietary and open technologies. While the metrics were crude and imperfect, we see glimmers of change along this industry continuum and some examples of the varying ways open platforms could shape innovation and competition. (For more details on the methodology, see sidebar, “Open competition: The data behind the risk profiles.”)

Consider construction cranes, a subset of the “machinery not elsewhere classified” sector (at the top of the exhibit). Software runs all the drive, calibration, safety, and security systems on modern cranes, and some crane manufacturers have started to adopt open-source software.4 To what extent has this development created a patent-infringement risk and a need to recalibrate innovation strategies? In the pharmaceutical industry (further down the exhibit), several players have formed consortia to ensure that basic genetic information remains accessible to them all. These same players revert to a proprietary model in downstream drug development. They deploy shared research in highly competitive branded products, thus highlighting the potential for diverse patterns of IP-based competition.

Finally, in motor vehicles (near the bottom of the exhibit), barriers to entry are significant because of the minimum efficient scale for factories and steep learning curves. Interestingly, even in this sector, the OScar Project has developed an open-source car design (which anyone can download), and Fiat has developed, for the Brazilian market, a fully crowd-sourced car, the “Mio,” incorporating more than 10,000 suggestions from volunteers.5

While we think this analysis may serve as a useful benchmark, we’d be the first to acknowledge that business executives are best placed to interpret the results. We hope that the industry tableau we’ve presented and the questions we’ve raised will provoke a productive debate in your organization about the evolution of the IP landscape and what it means for you.

For specialized innovators, a strategic discussion might start by determining the extent to which open innovation overlaps with core IP. The inverse is true for more integrated players, which could begin by assessing the potential savings from open solutions, the legal risks they could entail, and the investments required to reduce those risks through the creation of an IP-free zone.

For companies in both categories, relationships are crucial. Specialized innovators may find it desirable to work toward mutually beneficial royalty deals with suppliers and buyers that have adopted open solutions. Integrated players that want to pursue the IP-free option will need allies (which might even include established competitors) to share the cost of reshaping the ecosystem.

Finally, in a world of more open competition, it may become increasingly important to look continually for ways to boost the competitive differentiation of core IP. That might involve extending existing products or technologies with proprietary services that are difficult for open communities to replicate.

Related Articles

Using knowledge brokering to improve business processes