| Our best ideas, quick and curated | JULY 15, 2022

|

| This week, why companies are still having such a hard time adjusting to the new labor market, and what new research tells us they can do to fill all the open jobs out there. Plus, an interview with Stacey Sher about the future of movies and streaming, and five trends in the luxury-car market. |

|

|

|

| It’s still quitting time. Much has changed in the business world since early 2020, but one trend has remained constant: people keep leaving their jobs in droves. In fact, 40 percent of workers McKinsey recently surveyed say they’re thinking about leaving their positions in the next three to six months. That widespread disgruntlement is the same as 2021 levels. |

| But it’s not just about quitting. Workers are also switching jobs and industries, moving from traditional to nontraditional roles, retiring early, or starting their own businesses. They’re taking a time-out to tend to their personal lives or embarking on sabbaticals. Call it the Great Attrition, the Great Resignation, or the Great Reshuffling; any way you slice it, competition for talent remains fierce. At the current and projected pace of hiring, quitting, and job creation, openings likely won’t return to previous levels for some time. Organizations are going to be looking to fill roles for months to come, even if the economic outlook darkens. |

| New views of work. “The Great Attrition is making hiring harder. Are you searching the right talent pools?” reveals that many workers no longer want a traditional position with traditional pay and perks. This new research—including a survey of more than 13,000 respondents in six countries—shows that many people are reevaluating what they want from a job (and from life), and they’re looking for something more, less, or different. Employees frequently cite the feeling of always being on call, unfair treatment, unreasonable workload, low autonomy, and lack of social support as things undermining their well-being. They want more flexibility, more mental-health support, and more meaningful work. Companies are addressing these problems, to be sure, but they’re still coming up short. |

| Different talent pools. A central problem is that organizations keep trying to hire “traditionalist” workers using the same tried-and-true methods. Instead, they have to look in different talent pools, including people who have retired but might go back to work for the right situation. McKinsey’s research delves into five different employee profiles, or personas, to offer companies a new way of looking at the workforce. We broke them down into traditionalists, idealists, do-it-yourselfers, and others. These groups show that companies have to get more creative with their employee value proposition to solve this attrition problem for the longer term. |

|

|

|

| OFF THE CHARTS |

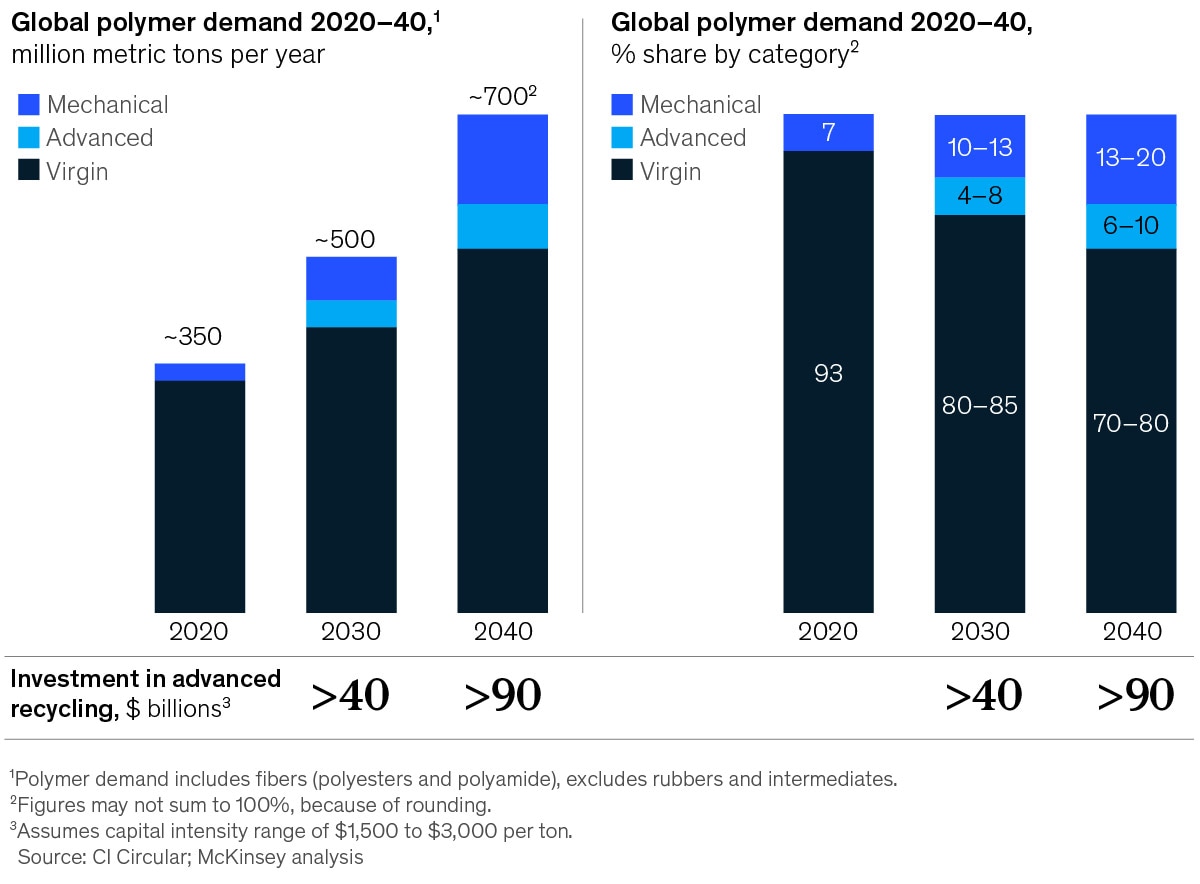

| Ramping up recycling |

| As interest in the circular economy grows, emerging recycling technologies are accelerating. Advanced recycling offers one potential solution to the increasing demand for circular polymers by expanding the types of plastics that can be recycled, allowing for the creation of polymers that can be reformed and reused. If existing constraints were resolved, advanced recycling could grow to 20 million to 40 million metric tons, providing investment opportunities of more than $40 billion.

|

|

|

|

|

|

|

|

|

| INTERVIEW |

| Artists and audiences in the streaming era |

| Stacey Sher, the producer of acclaimed films such as Pulp Fiction and Erin Brockovich, has had a front-row seat to the rise of streaming and its effect on how stories are told and consumed. In a conversation with McKinsey about the evolution of film and TV, she spoke about the postpandemic outlook for the moviegoing experience, the excitement of storytelling opportunities in streaming, and much more. “We’re in a time of flux, in a time of change, and what was on its way toward being broken is being broken in a different way,” she said. |

|

|

|

|

| MORE ON MCKINSEY.COM |

| Five trends shaping the luxury-car market | Sales of luxury cars continue to surpass the mass market in growth, profitability, and buzz. Here are five developments that will shape the luxury market over the coming decade. |

| Game on | Video entertainment, in all its forms, will become more immersive, gamified, and personalized by 2030. Four McKinsey experts imagine the future. |

| Customer care in 2022 | Customer experience is more important than ever—yet it has never been more challenging as companies face a perfect storm of increasing call volumes, talent shortages, and rising customer expectations. |

|

|

|

|

|

| WHAT WE’RE THINKING |

| Jennifer Spaulding Schmidt |

| Jennifer Spaulding Schmidt, a senior partner in the Minneapolis office, works with global consumer companies on large transformation programs and growth strategies. She also leads McKinsey’s apparel, fashion, and luxury work in the Americas. |

|

|

|

|

| Companies across sectors continue to struggle with supply chain challenges. One of the most counterintuitive approaches I have seen comes from an apparel retailer, whose solution is to turn competitors into collaborators and customers. |

| Most brick-and-mortar retailers are still catching up with the massive shift to e-commerce, which has accelerated during the COVID-19 pandemic and may well account for a third of all retail sales by 2030. When you’ve built an extensive network of stores, shifting to a business model in which you receive half of your sales from an online channel is a structural challenge. Suddenly, the old approach—all of your inventory landlocked in a distribution center in the middle of the country—doesn’t make operational sense. |

| Many retail chains started dealing with this problem a few years ago by shifting significant inventory to their stores—in effect, turning them into mini e-commerce order fulfillment centers. This model works when orders contain only one item that is close to the person who made the purchase. In most retail operations, the cost to pack a single item during downtime is seen as acceptable. |

| But retailers have learned that orders typically contain two or three (or more) items that usually aren’t available in the same location. The cost of paying multiple salespeople to pick and pack an order—as well as the extra shipping costs for that multiitem order—adds up quickly. Making matters worse, forward-deploying inventory to hundreds or thousands of locations makes it harder for retailers to keep up with unpredictable customer demand, which is something of the norm in fashion. |

| This apparel retailer decided it could do better by restructuring its supply chain. It opened more than a half dozen smaller fulfillment centers. The centers provided practically all the inventory that the retailer’s stores and online customers needed and could deliver it in a hurry. By replicating a model more common in fast-moving, highly predictable consumer goods, this retailer reduced online order costs by 15 percent per order. The company also slashed working capital by pulling seven weeks of inventory from stores and selling more goods at full price, since it didn’t have to mark down items stranded in stores. |

| This is where the story takes an interesting twist. Once the retailer saw how well its new supply chain network was working, it realized that it had landed on a possible new business. Nearly all of its competitors faced the same problem and a future of supply chain costs accelerating faster than revenues. Why couldn’t the retailer apply its new expertise to a cooperative model that provided the scale benefits and inventory balancing that only the largest big-box retailers could normally achieve? The math suggested that the retailer would need 250 businesses of its own size to match the scale economies of the larger multicategory retailers. Could it further evolve the model with technology, robotics, and analytics to offer supply chain as a service to its competitors? |

| It’s early days still, but the answer seems to be yes. This retailer bought two online logistics companies that had helped it establish the network and found ways to aggregate orders from different businesses to save parcel costs. The net result is $1 in savings per order, which is meaningful for midmarket retailers. It’s a frenemy strategy that encourages and creates incentives for open-source collaboration among competitors. |

| By now, many of us take online ordering and speedy delivery for granted. But I believe that their continued acceleration will roil the retail industry for a long time to come, even when the pandemic is a distant memory. |

| — Edited by Barbara Tierney |

|

|

Share this What We’re Thinking |

|

|

|

|

|

|

|

| BACKTALK |

| Have feedback or other ideas? We’d love to hear from you. |

|

|

|

|

Did you enjoy this newsletter? Forward it to colleagues and friends so they can subscribe too.

Was this issue forwarded to you? Sign up for it and sample our 40+ other free email subscriptions here.

|

|

|

|

|

Copyright © 2022 | McKinsey & Company, 3 World Trade Center, 175 Greenwich Street, New York, NY 10007

|

|

|

|