The global financial crisis and its aftermath of economic and regulatory change present major challenges to the traditional operating models of banks in developed countries and are undermining the sector’s ability to deliver a sustainable level of returns to shareholders.

A new McKinsey report, The state of global banking—in search of a sustainable model, shows that despite a strong global profit performance in 2010 and the first half of 2011, the return on equity (ROE) of banks in Europe and the United States has still not recovered to the point where it covers their cost of equity. The gap is set to widen in the wake of new regulatory requirements. Without radical action to shrink balance sheets, cut costs, and increase revenues, banks will be unable to attract sufficient new capital from the investment community and to play their critical role in underpinning economic recovery and growth.

On its face, 2010 was a good year for the industry. Global banking revenues reached a record $3.8 trillion, and after-tax profits jumped from $400 billion in 2009 to $712 billion—above their 2008 level, if not the 2007 peak. But this rosy picture did not necessarily imply a bright future for banks in Europe and the United States: 90 percent of the profit improvement was attributable to a reduction in provisions for loan losses, and most, if not all, of the good news came from emerging markets. Declining cross-border capital flows, high bank credit-default-swap spreads, and persistently low market valuations all pointed to declining investor confidence in the industry’s future long before the latest alarms over sovereign debt during the summer of 2011.

As a result, investors have been reassessing the banking industry’s long-term growth prospects and rerating the sector. The major problems include the rising cost of doing business—thanks primarily to new regulation requiring banks to hold more capital and liquidity to ensure that the industry better withstands future shocks—scarcity of capital and liquidity, changing consumer behavior as a growing number of customers move to mobile and online channels, and diverging regional growth paths.

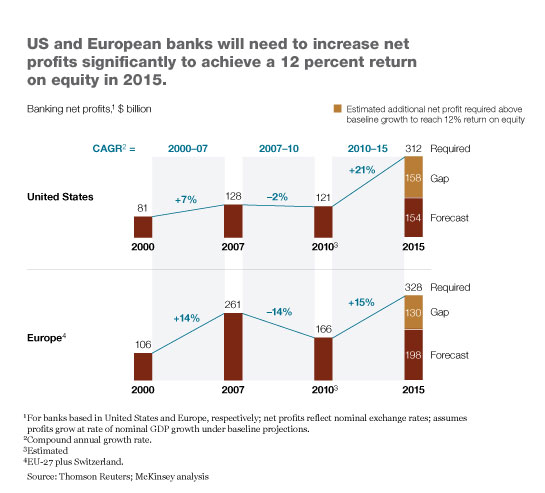

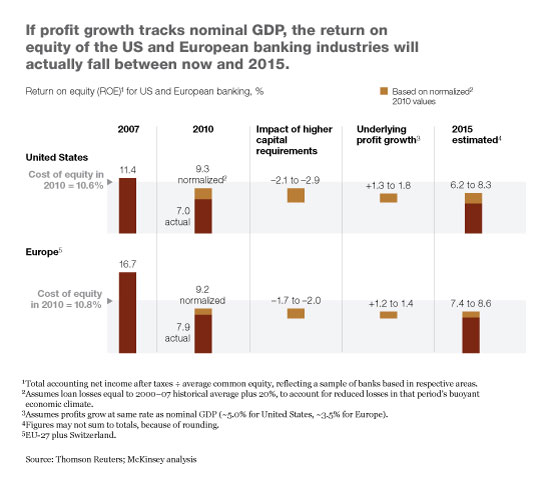

In 2010, the US and European banking industries delivered an ROE of just 7 and 7.9 percent, respectively. Even when these returns are normalized (by assuming loan losses equivalent to the 2000 to 2007 average), the 2010 ROE figures increase only to 9.3 percent in the United States and 9.2 percent in Europe. At this level, the banks’ ROE is still some 1.5 percentage points below their cost of equity. Even before the industry has digested the additional capital requirements from Basel III and other surcharges being considered by global and national regulators, banking in developed countries faces a significant returns gap (Exhibits 1 and 2).

We calculate that to achieve an ROE of 12 percent by 2015, European and North American banks will have to add more than $350 billion of net profits in the intervening period—double the current level. This sum is more than the total profits of the global pharmaceutical and automotive industries combined.

In Europe and North America, it’s clear that business as usual is not an option. Banks are squeezed for capital, profits are under pressure, and growth opportunities in the developed world appear to be in short supply. Emerging markets, we project, will contribute nearly half of all banking revenues around the world by 2020, compared with just one-third today, and will represent 60 percent of all revenue growth in banking over the next decade.

The process of transformation is already under way at many banks, but even market leaders must intensify their efforts to produce the long-term returns needed to attract investors. In our view, banks must combine three moves:

Shrink the balance sheet. Banks in both Europe and North America must find ways to work with less capital and to use what they have more efficiently. One way ahead for European banks is to shift a substantial part of their lending to the capital markets so that these banks do less direct lending and help revive the corporate-bond market. In Europe, such bonds address only 20 percent of the credit needs of companies, compared with 60 to 70 percent in the United States.

That kind of change would be challenging at both an individual bank and system level and would require an expansion of traditional debt markets and the development of low-cost alternatives to them, action to expand the investor base in the bond market, and the creation of new and safer asset- and mortgage-backed securitization markets. Ways to make balance sheets less capital intensive without shifting risks to the capital markets include a more sophisticated approach to the risk-weighted asset calculation, the optimization of credit lines, and better management of collateral. Individual banks will increase their capital efficiency by making capital and liquidity management a much more central, long-term discipline.

Rebase costs. To achieve a 12 percent ROE through cost cuts alone—taking none of the other actions we recommend—banks would have to reduce their expenses by up to 6 percent a year between now and 2015. That’s a tall order, since only about 1 bank in 50 achieved annual cost reductions of 4 percent or more in the years from 2000 to 2010. But other industries, notably telecommunications, have responded to new regulation, technology, and competition by dramatically improving their productivity. Banking remains one of the most fragmented sectors globally, and depending on the stance of national regulators some institutions should be able to pursue large-scale mergers and acquisitions.

What’s more, we have found that banks can eliminate as much as half of the cost of their branches by moving sales and service online. Some banks have shown what can be achieved through the application of lean and other techniques—for example, cutting the time to process a mortgage to 60 minutes, from days.

Capture new opportunities. Banks have overcome previous crises by finding innovative ways to increase the top line. Although opportunities may seem to be limited, we see huge scope to improve pricing, to adapt products to the needs of customers, and to find new pockets of growth (taking advantage of the better risk-management processes many have introduced in the wake of the crisis). Opportunity lies in the potential for disruptive technology in both consumer and wholesale banking—yet many of banking’s digital strategies are still in their infancy.

Action to restore the banks’ ROE to a level at least equal to, or above, the cost of equity is not only essential for the industry’s own health but also a precondition for long-term economic recovery.

Download the full report, The state of global banking—in search of a sustainable model.

Also available is a related report, Day of reckoning? New regulation and its impact on capital-markets businesses (October 2011), which argues that to compete successfully, banks will need to build their capital-markets businesses around core competencies.