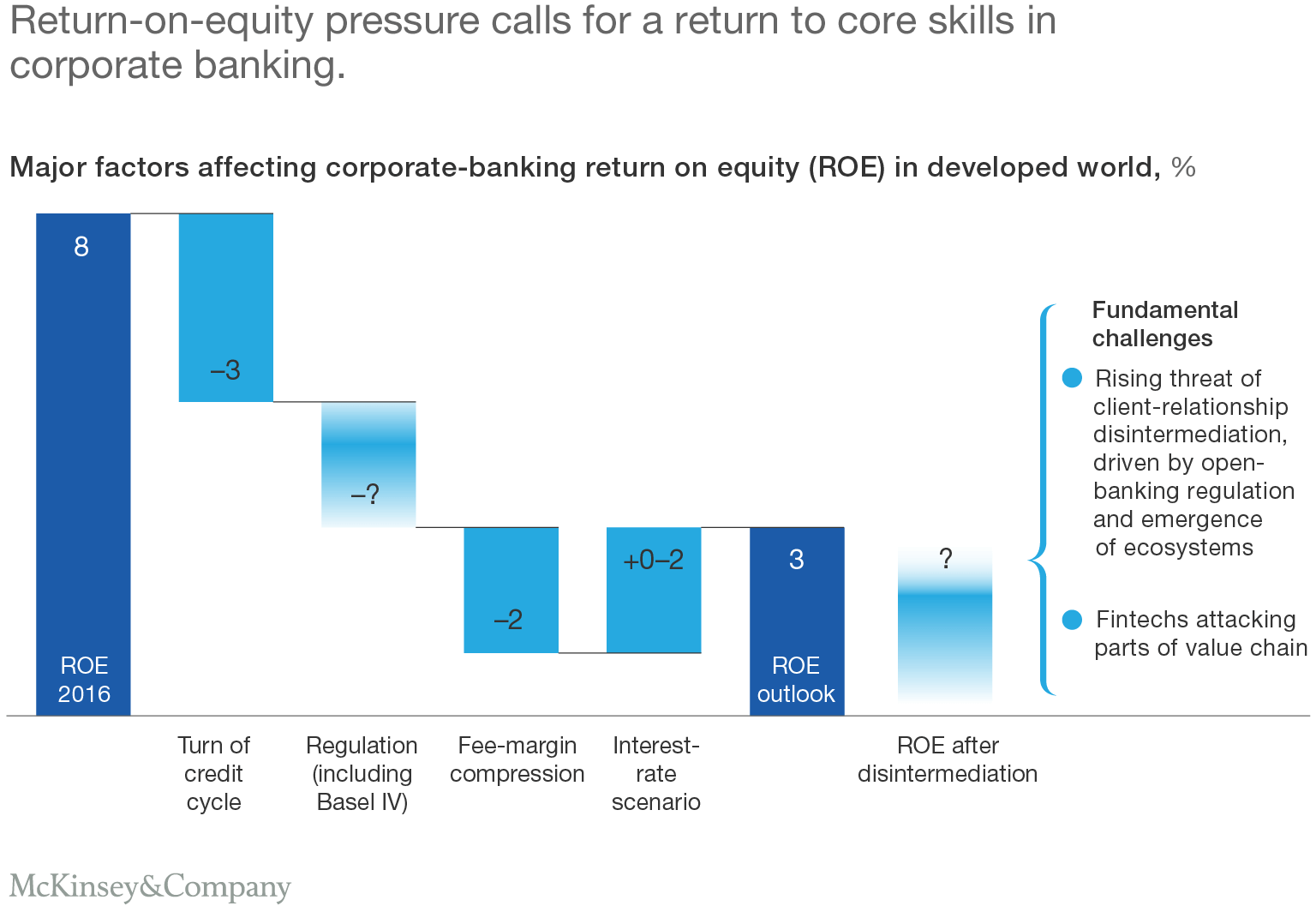

Corporate banking—once a sector that delivered strong returns—has lost its luster in recent years. The sector has generated steady revenue growth of 5 percent CAGR since 2009, with a modest uptick to 9 percent ROE in 2016. The outlook does not appear to get brighter. A cyclical economic reversal over the next five years will likely bring about a normalization of risk costs. In addition, banks will face ongoing regulatory requirements to set aside more capital and comply with strict liquidity and funding rules. Combined, these factors will depress ROEs to a potential low of 3 percent before mitigation and usher in an era of lower baseline profitability (Exhibit 1).

A cyclical downturn and further regulation are not the only prospective challenges for corporate banks. Fintechs, platform-based ecosystems, and leading banks in the sector are targeting the parts of the value chain that offer both direct access to the customer and the highest profitability (53 percent ROE)—such as origination/sales and payments. Attackers are also likely to benefit from legislation such as Europe’s second Payment Services Directive and the United Kingdom’s Open Banking initiative that seeks to widen access and encourage competition in the small- and medium-size-enterprise and midmarket-corporate arenas.

These challenges raise the question of whether today’s corporate banking model fits the purpose. McKinsey estimates that ecosystems will replace numerous value chains in the next ten years to account for $60 trillion in revenues and 30 percent or more of global gross economic output. Corporate banking leaders need to consider how they can play active roles in ecosystems in the coming years.

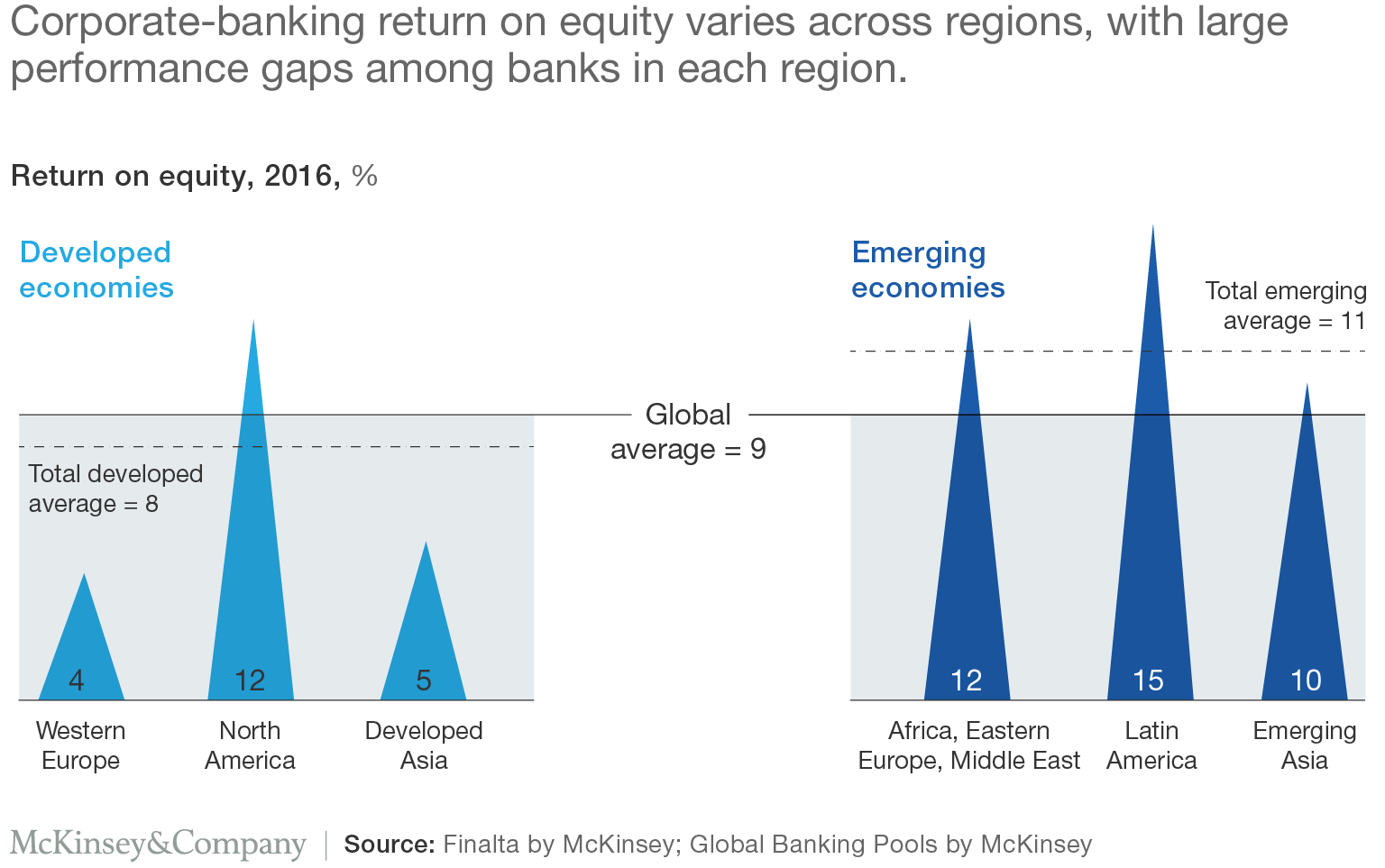

Globally, there is an ROE gap of more than 15 percentage points between top- and bottom-quartile corporate banks (Exhibit 2). A decade ago, location was the key factor accounting for the gap between leaders and laggards. Today, beyond risk selection and management skills, successful corporate banks distinguish themselves through superior cross-selling capabilities, loan-pricing skills, and cost efficiency. Encouragingly, these areas offer banks tangible opportunities to improve performance.

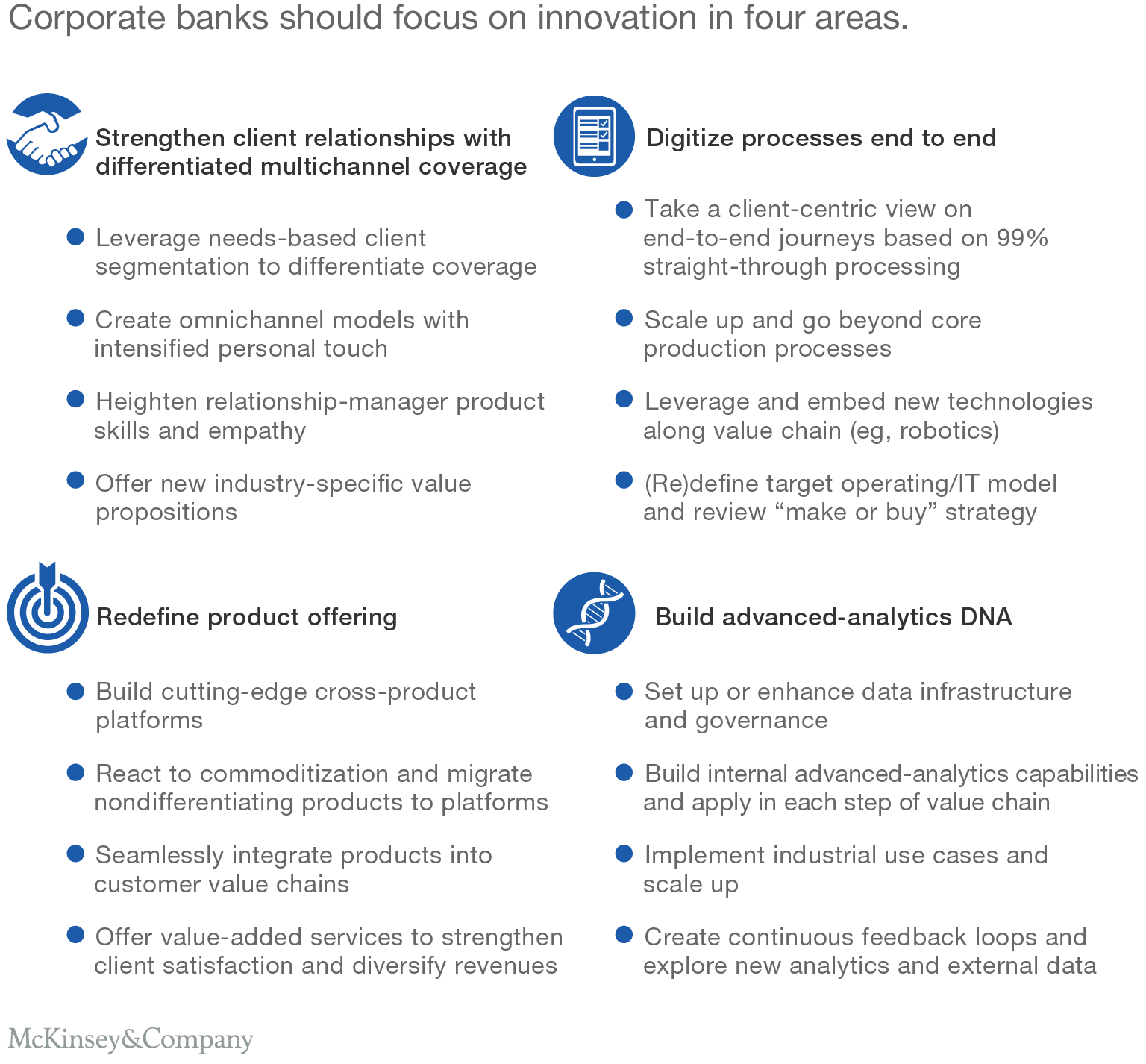

To retain market share, broaden revenue pools, and avoid disintermediation, corporate banks need to offer a more distinctive value proposition by drawing on their expertise, data, and strong relationships. In pursuing these objectives, they must determine the roles they will play in ecosystems and use technology to increase efficiencies and serve customers better. Specifically, McKinsey sees the following four transformational levers for corporate banks:

- Strengthen client relationships with differentiated multichannel coverage. To fight disintermediation, banks must strengthen client relationships by using needs-based segmentation, differentiated omnichannel coverage, and industry-specific value propositions. Relationship managers need support to develop new skills to provide a higher level of service to high-value clients.

- Digitize processes end-to-end. Banks can increase customer satisfaction and reduce costs by building digital customer-centric journeys, embedding innovative technologies (such as robotics) along the value chain, industrializing core production, and redefining the IT and operating models.

- Redefine the product offering. In response to commoditization and the convergence of flow and credit products, banks should build cross-product platforms, migrate nondifferentiating products onto those platforms, seamlessly integrate with client value chains, and offer value-added services.

- Build an advanced-analytics DNA. Banks need to close the gap with Silicon Valley’s customer centricity by enhancing data governance and infrastructure, building advanced-analytics capabilities, scaling up use cases, and pursuing continual improvement.

In their efforts to transform, corporate banks will face complex competitive, technological, and demand dynamics. They will need organizational agility, an aspirational vision, investments in talent and front-to-back agile delivery, a multiyear road map and budget, and a client-value-driven IT architecture. Corporate banking has traditionally been considered more of an art than a science; however, current challenges demand management rigor and technological expertise.

The corporate bank of the future will be more responsive and ready to compete. Getting there, however, will require much work. Banks will need to reimagine their front, middle, and back offices and develop leadership skills in innovation, risk management, and service (Exhibit 3). Those that succeed will achieve as much as double-digit revenue growth, as high as a 20-percentage-point drop in cost-to-income ratios, and an ROE advantage of ten percentage points against lagging peers.