Unsecured lending volumes in the United States are at an all-time high, thanks to improving eligibility rates, enhanced awareness and access, and continued investments in new lending models and start-ups. A key source of growth for some lenders and worry for others has been the acceleration in use of point-of-sale (POS) financing. Most traditional issuers are still in the early stages of assessing their POS lending strategies, so many are not entirely aware of the scale and pace of disruption. We see four key factors having an impact on the POS lending segment: shifts in consumer and merchant awareness and preferences, a broadening market share in smaller ticket purchases and higher prime segment, increasing competition, and a more important role for integration of POS financing into the pre-purchase phase of the customer journey. Several business models offer a choice of tactics for seizing the opportunities that result.

Consumer and merchant awareness and preferences are shifting

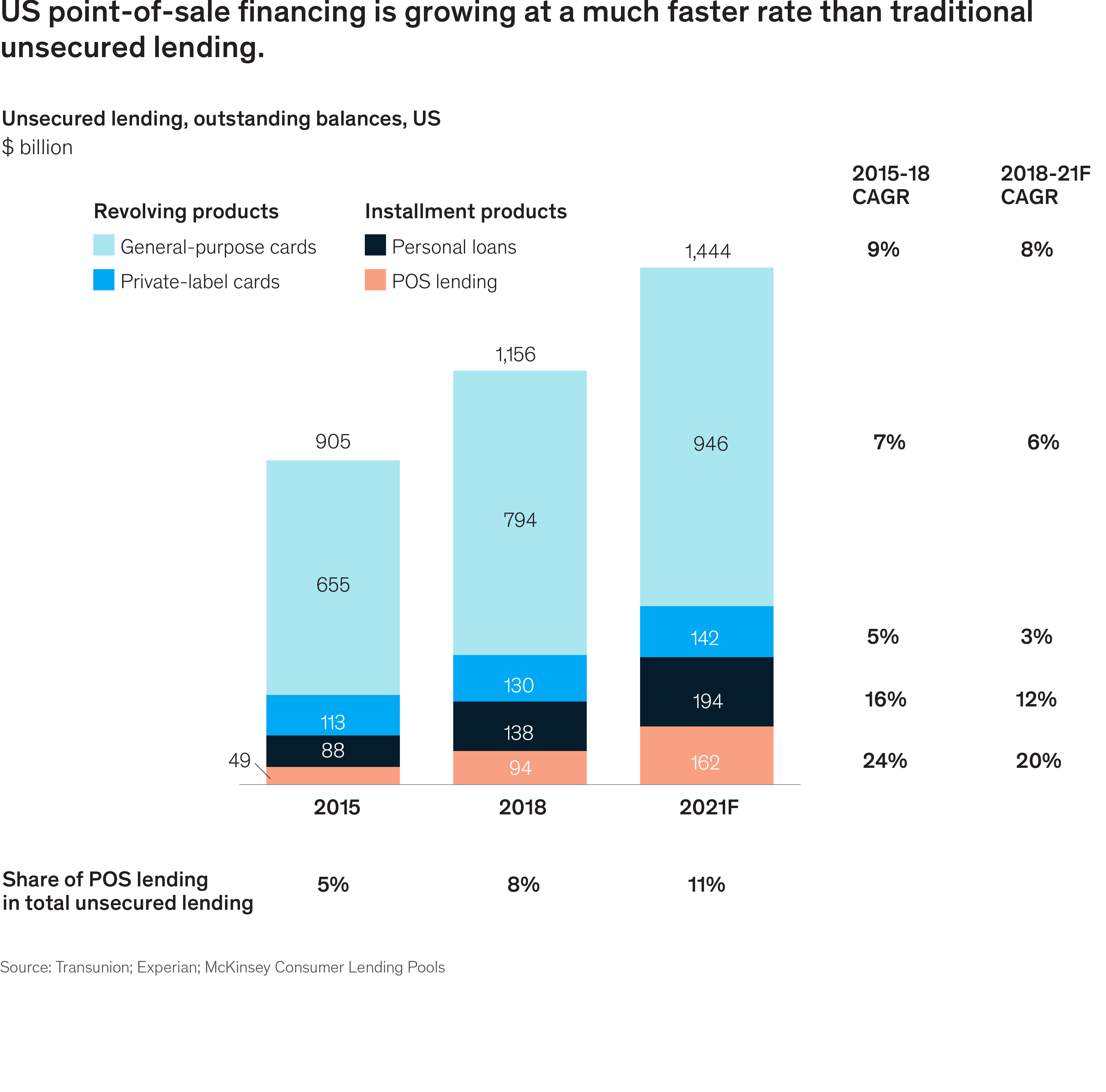

While point-of-sale financing is a proposition that has been around for a while, the pace of its growth has accelerated in response to enhanced integration of POS financing offers into purchase processes, better application experiences, and newer business models. Based on McKinsey Consumer Finance pools, the total US outstanding balances originated through POS installment lending solutions stood at $94 billion in 2018 (Exhibit 1). Those balances are expected to exceed $110 billion in 2019 and to account for around 10 percent of all unsecured lending. This volume has more than doubled between 2015 and 2019 and has taken three percentage points of growth from credit cards and traditional lending models, worth more than $10 billion in revenues.

Although a recession would test the viability of certain business models within POS lending, the underlying shift in consumer awareness is here to stay. So is borrowers’ growing preference to borrow at point of sale and get a line of sight to paying down balances, potentially at lower rates subsidized by merchants. Additionally, as emerging digital merchants rely on POS financing to drive growth, larger merchants also are more willing to engage with and integrate POS financing solutions, as Walmart is doing with Affirm.

POS financing is capturing greater shares of smaller-ticket purchases and higher-prime segments

Initially, POS loans mostly targeted lower-prime or higher-ticket segments, such as those seeking a loan for home remodeling. Today, however, newer entrants, such as Afterpay, Klarna, and Sezzle, are displacing credit card spending more directly. Purchasers with ticket sizes as low as $200 to $300 are shifting to shorter-tenure (four- to six-week) POS financing. These smaller-ticket (less than $500) POS loans, which are estimated to total $8 billion to $10 billion in 2019, are growing at rates exceeding 40 to 50 percent.

Additionally, a rising number of premium merchants are offering financing at 0 percent APRs from POS financing providers. These services, combined with a seamless application experience, are starting to attract prime customers. In 2019, around 55 percent of origination volume is expected to be from the prime segment (buyers with credit scores above 680).

Increasing competition is transforming the economics of POS lending

As consumer and merchant awareness increases, so does competition, and this results in changing economic and risk models in POS financing. Around 50 to 60 percent of loans originated at point of sale are either partially or entirely subsidized by the merchant. As merchants become more willing to bear interest costs, lenders are experimenting with new pricing models. In sectors with a high cost of acquisition and high margins, such as jewelry and luxury retail, merchants are willing to fully subsidize APRs.

As POS lenders are starting to partner with smaller merchants, risk models also are changing. For smaller merchants, lenders are now underwriting both the merchant and the consumer.

Integration of POS lending into the pre-purchase phase of the consumer journey is now essential

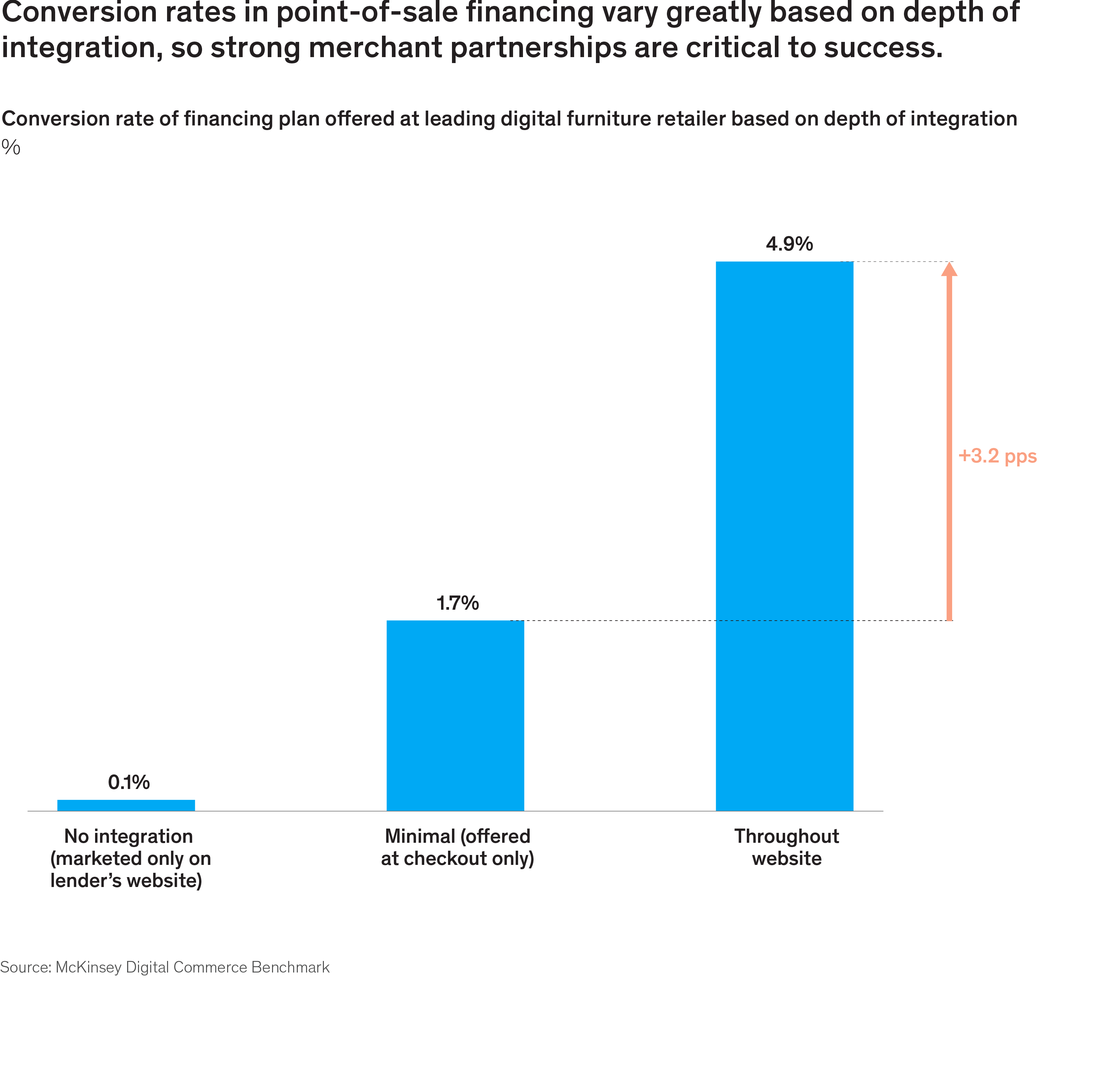

Around 75 percent of consumers who finance large-ticket purchases decide to do so early in the purchase journey, before the actual purchase. Embedding their offerings earlier and more directly in the consumer’s purchase journey increases the likelihood of consumer adoption. And integration of financing offers throughout the consumer journey, from research to checkout, increases the conversion rate by two to three times, relative to a simple integration at checkout (Exhibit 2). Additionally, deeper integration drives stickiness, so it is tougher for competitors to displace lenders at point of sale.

Key business models are emerging in POS financing

As the players engaged in a land grab for merchants increase in quantity and diversity, the competition for merchant access in POS lending also is growing. Traditional players exploring a play in POS financing have a limited period to enter the market and grow. In 18 to 24 months, laggards either will be unable to compete, because most merchants will already have POS financing partners, or will need to pay a heavy premium to get into the market.

To get into POS lending, traditional lenders typically explore a mix of five business models. Some of these also apply to acquirers and entities with direct merchant access:

- Rent out the balance sheet. Banks can partner with established POS financing players to originate loans. This strategy offers only limited and indirect access to consumers but nonetheless permits entry to the market with minimal investment.

- Join a marketplace. Banks can lend in online ecosystems that bring multiple lenders to merchants. This avenue offers greater consumer access and brand presence at a low initial investment. It also affords greater control over underwriting. For merchants, it offers higher approval rates and limited integration fatigue.

- Rent a technology platform. Banks can rent existing POS financing technology platforms to monetize their merchant relationships and balance sheet without needing to invest in building a POS lending infrastructure in-house. This path monetizes existing merchant relationships but requires greater investment in business development.

- Become an end-to-end solution provider. With a greater up-front investment and market development effort, banks can construct their own end-to-end POS financing operations and engage the fintechs head-on.

- Innovate around the card platform. For a simple alternative that grants consumers lower interest rates and line of sight, banks can enhance their card offerings with installment loans within existing credit card accounts to capture a larger share of consumer borrowing and monetize unutilized credit lines. Integrating card-enabled installments at point of sale can be an industry disruptor, and first movers will be able to see significant upside in wallet share.