Last year, the McKinsey Banking Consumer Survey was extended for the first time to Portugal. The results show that Portuguese banking customers are well ahead of banks in digital adoption—which means that Portuguese banks have a big opportunity to innovate on network shape, new formats, refreshed customer conversations, remote advisory, and digital sales and service. It is time for bank leaders to rethink the multichannel approach and introduce a strategy that reflects customer preferences.

The survey confirmed the scale of the opportunities. Digital adoption is high (61 percent of customers)—but it outstrips banks’ capabilities to deliver digital services (Exhibit 1). For example: the majority of customers would consider digital channels to open an account (61 percent), apply for a credit card (59 percent), or apply for a consumer finance loan (50 percent), but only a fraction of these actually do it. When we asked the customers why they don’t do more activities online the most common answer was, “What I do in branches can’t be done by other channels,” even amongst the more affluent and informed customers.

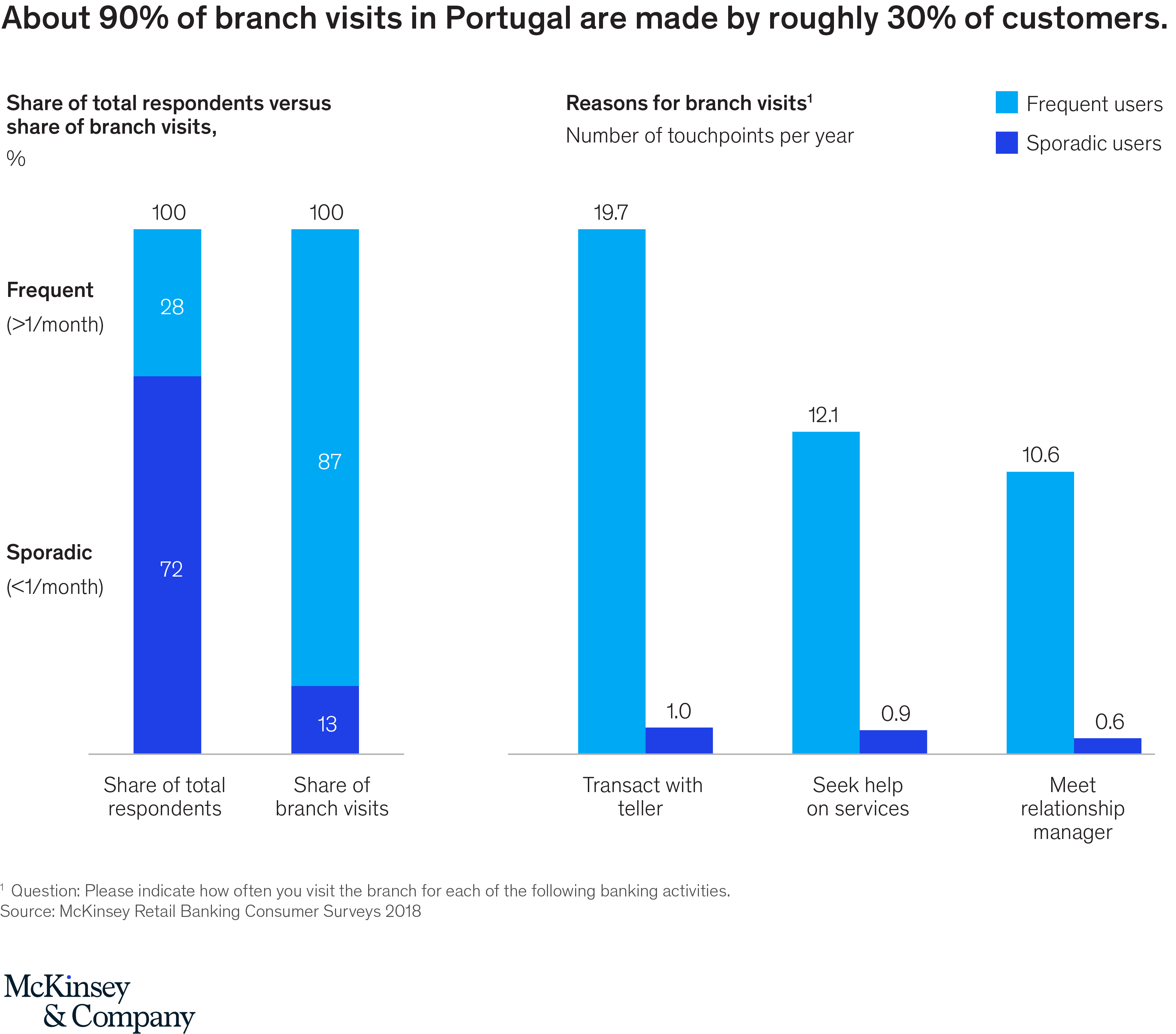

Portugal has always been a branch haven in Europe. In fact, the country is still among the leaders in branch density despite severe rationalization in the last five years. But the love for branches is being kept alive by a minority of customers. According to our research, 87 percent of bank branch visits are made by 28 percent of customers (Exhibit 2), which means that Portuguese banks are keeping branches open for less than a third of their customers. These tend to be older clients, who are highly focused on personal service and security. There is a clear opportunity to further rationalize the branch network, to migrate transactions (to ATM and digital), and to deploy a more automated, leaner and paperless branch operating model.

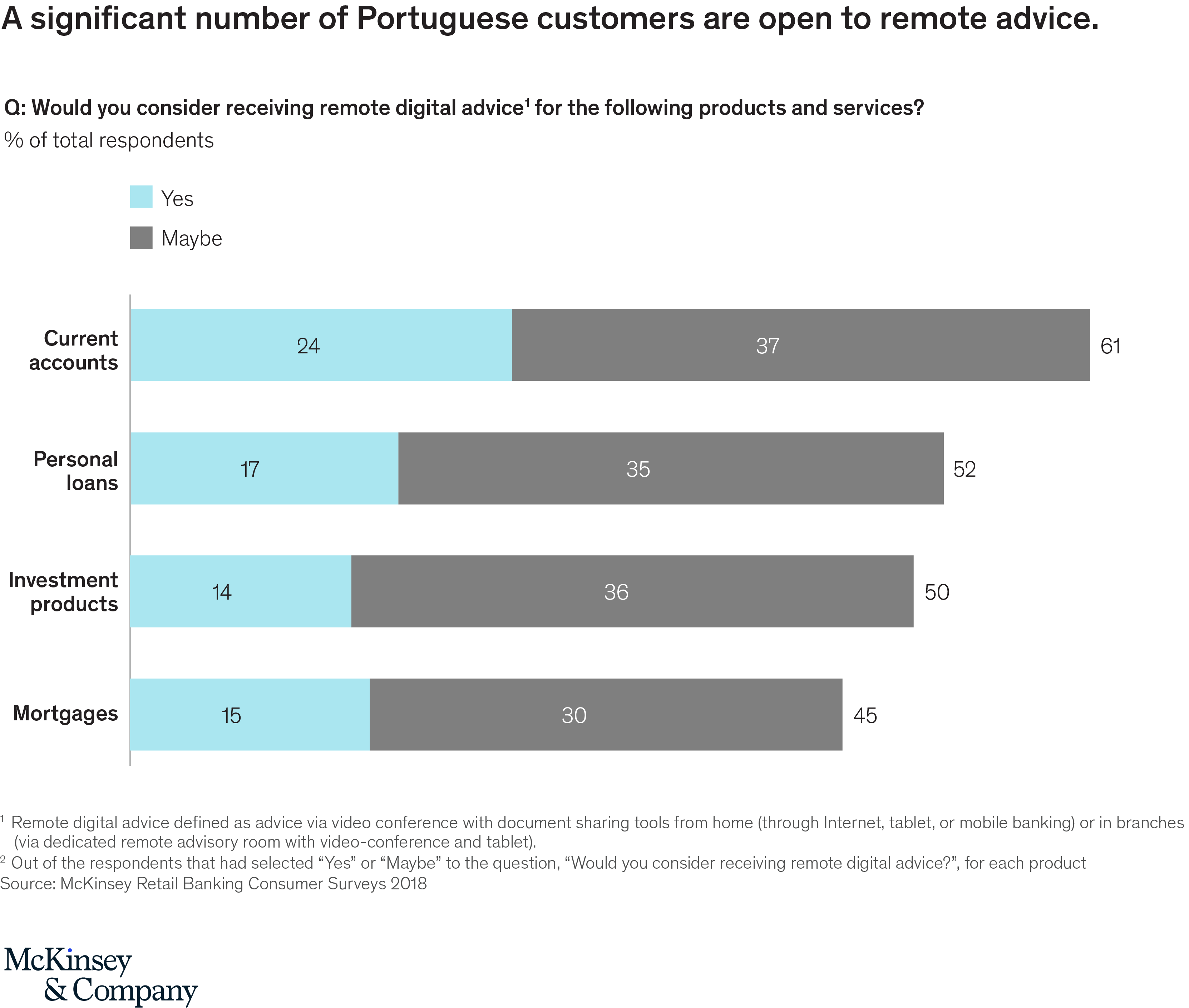

Another common perception is that Portuguese banking customers highly prefer face-to-face advice. Our research counters this idea—customers in Portugal actually show a high preference for remote digital advice, even in the most complex areas (Exhibit 3); for example, 45 percent are open to the idea of receiving remote mortgage advice. Migrating customers to a remote advisory model can significantly reduce the cost to serve. For example, the load factor of a remote relationship manager (RM) can be two times the 300 to 400 customers/RM in branch; and remote advisors show increased sales effectiveness—more than 40 percent meetings per RM and more than 30 percent banking income per meeting.

With that said, branches are still very important for customer acquisition in Portugal. Footprint remains key—branch proximity and access is still cited by new customers as a main factor in choosing their bank.

So how can banks grab the remote and digital opportunity while still serving those customers that prefer traditional channels? As customer preferences shift, banks need first to set new roles and targets for their channels. As in other markets, Portuguese bank branches will focus more on advice and complex interactions—a shift away from their traditional focus on transactions and cash. But these big changes in the network must always be accompanied by an improved staffing model that features multiskilling and flexibility.

Banks are moving towards a concept of branches where all employees can advise customers, and with opening hours and days aligned with customer traffic. This trend has proven its ability to reduce total in-branch FTE costs by about 8 to 10 percent. A European bank transformed its tellers into basic bankers—that is, they keep their teller roles handling counter transactions, enquiries, and support, but are also trained with skills including digital onboarding, remote advice support, simple product needs, and offering an introduction to mortgages. With these additional skills, at off-peak hours they can turn from tellers into basic bankers and contribute to sales growth.

This fluidity indicates the scale of the opportunity for banks that re-set their multichannel model to reflect customer evolution. This requires a digital approach to sales and service using advanced analytics both to acquire and retain clients, and to understand customers better at every stage of their journey. This must involve active customer satisfaction management.

The message coming out of our survey is crystal clear. Coaxing customers toward digital channels, combined with new “smart branches,” offers enormous potential.