Competition in the banking industry is intensifying. Neo-banks are winning market share and serving customers at around one third of the cost of traditional banks. Fintechs are targeting lucrative niches in the value chain. Big tech players, with their large customer bases, pose a real threat and a few incumbents are investing heavily in innovation, putting laggards in the shade.

Attackers are growing their businesses and attracting customers with the help of modern core technology architecture, which enables them to innovate faster and operate more efficiently. Not surprisingly, incumbent banks are increasingly concerned about the limitations of their own core architectures and their relatively slow pace of change. As a result, some 70 percent of banks are reviewing their core banking platforms, according to a McKinsey survey of 37 banking executives in May 2019.

We see four key areas in which legacy platforms inhibit performance:

- Cost. Cost is more important than ever given low industry return on equity (ROE). Yet technical debt in legacy systems consumes large chunks of IT spend—one mid-sized bank spent two-thirds of its digitization budget on this alone. Clunky legacy systems are associated with manual software delivery (manual regression testing and deployment) and low straight-through-processing rates (accumulated layers of complexity leading to fragmented and manual operational processes), which conspire to keep costs higher than necessary.

- Time to market. Being able to launch products quickly is a critical competitive differentiator in the current crowded marketplace. However, faster product delivery is restrained by monolithic architectures (leading to multiple interdependencies and bottlenecks), poorly documented legacy code (causing over-reliance on a small number of subject matter experts), and manual delivery processes.

- Personalization. Customers increasingly expect a personalized experience. But banks often store data in multiple product-aligned core systems, which inhibits catering to individual needs. For instance, one major bank had to invest in a major two-year program just to offer customers a combined view of savings accounts and investment products.

- Ecosystems. Partnerships are becoming critical to creating the products and services of the future. Yet current architectures lack the connectivity to third parties that would enable innovation (e.g., property related services for mortgage buyers).

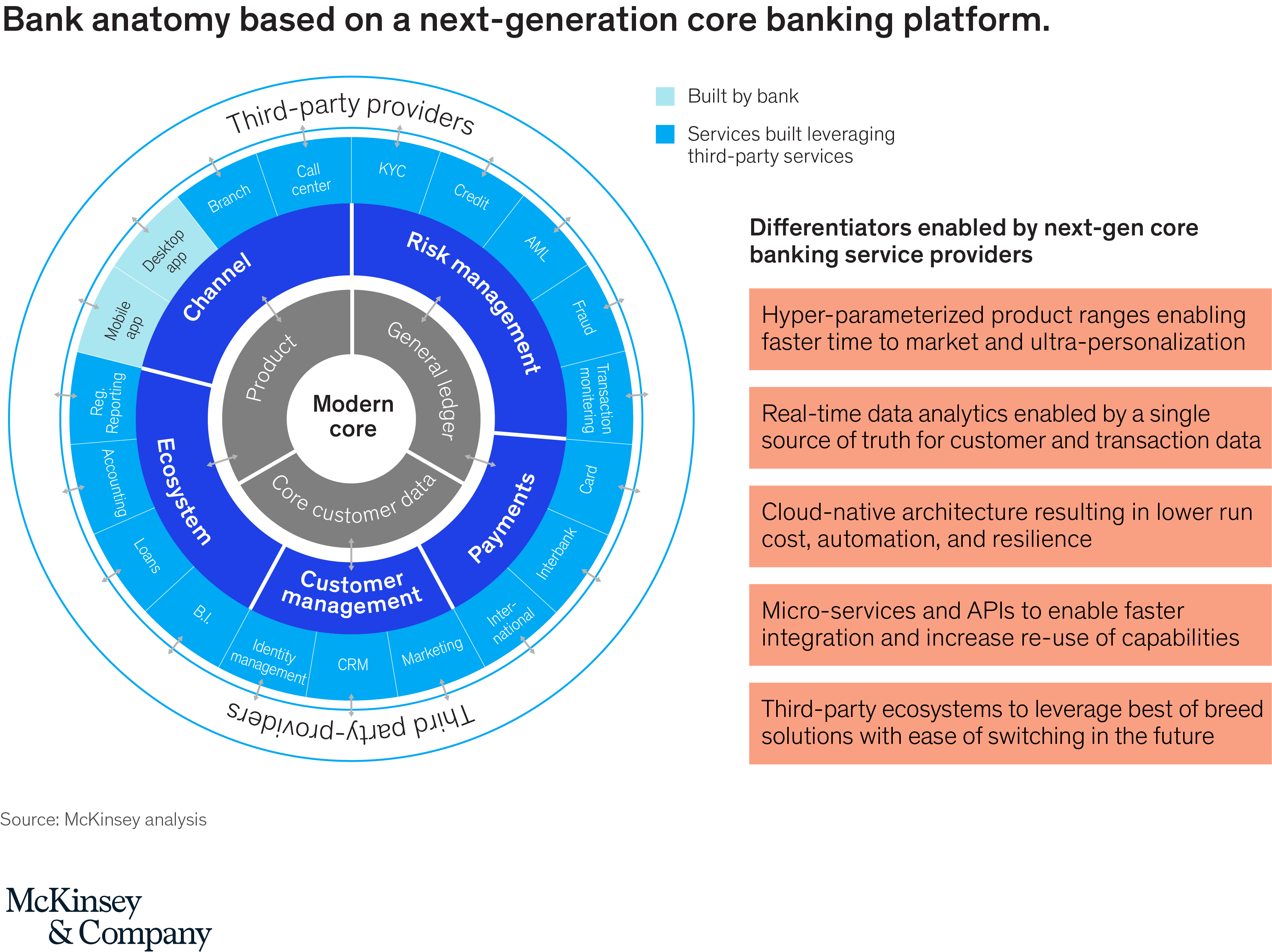

The good news for incumbents is that the tools are at hand to address these challenges. In particular, a new generation of cloud-native core banking platforms is emerging, including Mambu, 10X, Thought Machine, and FinXact, alongside offerings from the traditional core platform vendors. These promise to help banks radically modernize and bring the possibility of benefits including (Exhibit 1):

Exhibit

- Reduced IT costs. Banks can cut spending through higher developer productivity and removal of technical debt. They can achieve further efficiencies by leveraging cloud-based services (which enable them to deploy new products and scale infrastructure quickly) and by using development tools that support automation (DevSecOps).

- Accelerated time to market. Banks can more easily and speedily develop new products and services, aided by hyper-parameterized configuration capabilities. Higher levels of standardization make it simpler to leverage modern tools such as automated testing and therefore to implement more frequent deployment cycles.

- Data and a customer-centric proposition. Data capabilities are set to become a critical differentiator. Modern platforms support integrated data sets and a single source of truth. These in turn create the ability, in real time, to offer personalized experiences and run advanced analytics for sharper decision-making (e.g., for front-line staff).

- The ability to scale through partnerships and innovate. New platforms enable rapid scaling and less expensive development of ecosystems and ancillary services. Integration is easier with modular architectures and communication via APIs.

Given these benefits, it’s not surprising that more than 65 percent of the banks we surveyed are exploring the potential of next-generation platforms. Indeed, around the world, several have announced partnerships and are on the way to realizing significant benefits.

As attackers and some incumbents move forward, banking leaders remaining on the sidelines have three practical options (Exhibit 2):

Exhibit

- Full replacement of the core with a new tech stack. Banks often pursue this course of action when they urgently need to replace their core platforms because of obsolescence or regulatory imperatives. However, it can be risky. It requires extensive data migration and the benefits are typically only realized when the final customer is migrated and the legacy systems are decommissioned. Banks generally choose a traditional platform as the replacement, reflecting concerns that next-generation platforms are not yet fully proven or focused on a subset of products and features.

- Progressive modernization. Most banks have pursued this strategy. It comprises retaining the legacy platform but progressively minimizing it as they build a modern architecture around it. It is often seen as a safe option if the current architecture is viable for the next five to ten years. Most advanced banks start with the most critical customer journeys and a “strangler pattern”—hollowing out frequently-used functionalities and rebuilding them as microservices. Still, while the approach is lower risk than the first option, transition timelines are generally slow and banks may not achieve the desired levels of efficiency and time-to-market.

- A greenfield banking proposition built on a new tech stack. CXOs focused on staying ahead of the curve often pick the greenfield option because it enables them to launch new offerings and deliver value quickly. It is often considered less expensive than the other options and safer because the existing customer base is not exposed until the proposition and technology are proven. With many banks exploring next-gen core platforms, this option arguably provides the best way to elicit the most value. A few institutions are also exploring the possibility of migrating a large incumbent customer base using a “reverse takeover” approach.

In terms of budget, the majority have earmarked $10 million or more over the coming year (sufficient for experimentation), with around 20 percent planning to invest $20 to $40 million, according to our survey.

The platform decisions leaders make now will set their direction of travel for the next five years or more. They need to think carefully about their next move. Still, there is scant opportunity for delay. The industry is approaching an inflection point, at which technology leaders will put clear blue water between themselves and the competition. The bottom line? CXOs need a clear strategy to avoid being left behind.