More than four in five Americans used some form of digital payment in 2021, continuing a long-standing trend. The findings of McKinsey’s 2021 Digital Payments Consumer Survey—an ongoing research initiative in its seventh year—also indicate the continuation of several behavioral trends from the previous year’s survey, conducted during COVID-19’s initial wave. Furthermore, responses on cryptocurrency and “buy now, pay later” (BNPL) financing indicate that these topics have moved further into the mainstream for the American consumer.

Solidifying digital gains, amid some retrenchment

The 82 percent of Americans using digital payments—defined to include browser-based or in-app online purchases, in-store checkout using a mobile phone and/or QR code, and person-to-person (P2P) payments—in 2021 exceeds last year’s 78 percent and the 72 percent of five years ago.

Omnichannel use of digital payments continues to grow over time, although it experienced a dip from 2020’s all-time high of 58 percent. Some shifts in digital adoption during 2020 and 2021 appear to be related to the COVID-19 pandemic and may prove to be transitory. In-app payments are an interesting case in point: with more consumers staying at home, ride-share usage declined as would be expected, while meal delivery increased. In fact, online payments was the only category of digital payments to register growth, up 12 percentage points in 2021, possibly as a result of pandemic-related behavior changes including more time spent at home (and ordering more products remotely).

The behavior of the 35–54 and 18–34 brackets has converged to a greater extent than many might have expected. In-app payments is also the category with the widest age disparity; its adoption rates are three times higher for 18-to-34-year-olds than for customers 55 and older. Across all age groups, adoption of P2P and digital in-store payments lag that of online and in-app payments. The relatively slow adoption of these two categories may also result from the pandemic’s impact on customer behavior; for example, increased online shopping and fewer in-person interactions involving splitting of bills (and thus fewer opportunities for P2P).

Consumers’ level of trust in financial services companies and tech firms remains similar to last year’s, with the relative rankings of various players consistent across age groups. Banks and traditional payments networks (Visa, Mastercard) continue to lead in trust, although familiar tech firms (Amazon, Apple, and PayPal) continue to narrow the gap. Newer fintechs generally register lower consumer trust, perhaps because they have not gained name recognition and familiarity.

Regardless of provider, however, younger respondents consistently express higher trust in digital solutions.

BNPL proving effective; crypto growing rapidly

For two of the most widely discussed industry innovations—BNPL and cryptocurrency—our research reveals favorable yet different usage patterns.

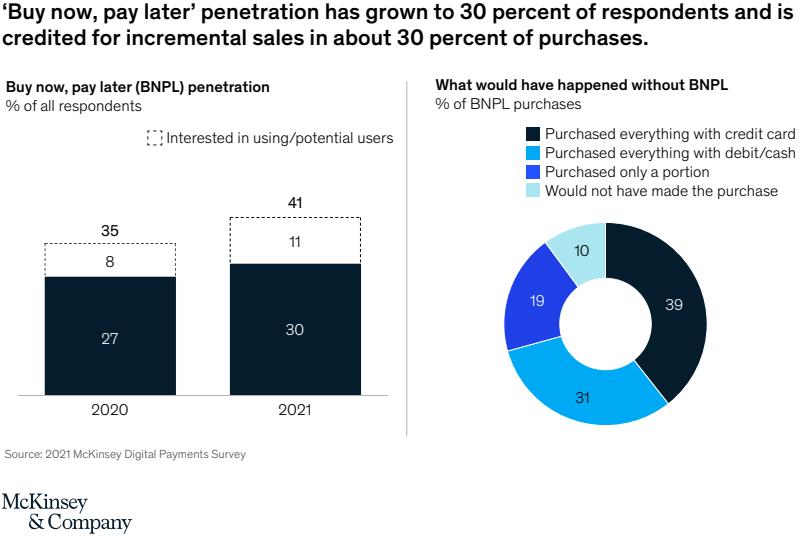

Asked about BNPL, 30 percent of our survey respondents report having financed a purchase with this type of service (Exhibit 1). Although this share is only three percentage points higher than 2020’s, attitudinal data seem to support the value proposition put forth by BNPL providers—and given the product’s increased availability we believe usage may be growing faster than penetration.

Of the respondents who used BNPL, 29 percent report that without this financing option they would have made a smaller purchase or not purchased at all. Another 39 percent say they chose BNPL over use of a credit card, and the remaining 31 percent indicate BNPL was a substitute for a debit card or cash. Separately, “a lower-cost financing option” was the most commonly cited reason for BNPL use (31 percent).

BNPL’s impact on incremental sales varies significantly across verticals. We see the highest incremental conversion rates in certain discretionary categories—apparel, laptops, and beauty products, for instance—where up to 20 percent of respondents say purchases would not have occurred without BNPL. Incremental conversion is far lower (3 to 5 percent) in less discretionary categories, such as tires and auto parts, home appliances, and home improvement.

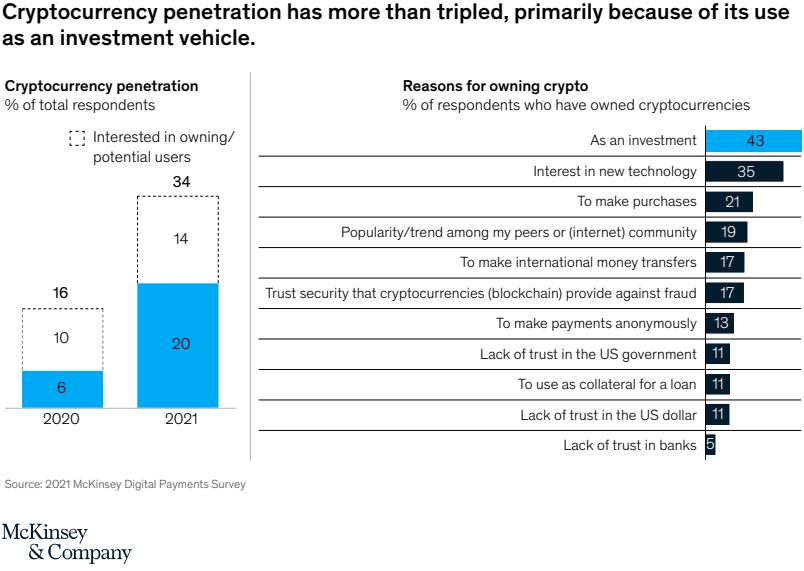

Turning to cryptocurrency, its penetration remains nominal on a broad level, but its steep adoption curve is striking. One in five respondents report holding or having held crypto assets, up from 6 percent just a year earlier (Exhibit 2). Among the 74 percent of respondents familiar with but not owning crypto, 41 percent say a key reason for not yet having used crytpo is their lack of functional understanding—an indication of further room for growth.

Of past and present cryptocurrency owners, 43 percent say they are motivated by its investment potential; of that group, 41 percent say they allocate at least 5 percent of their portfolio to the vehicle. Bitcoin continues to dominate this market, with three-quarters of those having owned cryptocurrency including Bitcoin in their portfolios. Surprisingly, however, among the broader population Bitcoin’s 15 percent penetration does not significantly outpace that of Dogecoin and Ethereum (11 percent each).

Fewer respondents own cryptocurrency for making purchases. Twenty-one percent cite transactions as their primary objective, often pointing to anonymous payments and international transfers as use cases. Roughly one-fifth reference a lack of trust (in the government, banks, or the US dollar) as their motivating factor.

Digital wallets making further dents in leather

Fifteen percent of digital-wallet users say they leave their residence regularly without their old-school version. Another 11 percent indicate they consider doing so only when they do not plan to purchase anything or know they can use a digital wallet.

Following widespread promotional efforts designed to coax consumers to enter card credentials, most respondents using digital wallets have now loaded multiple cards. Of those who say they have done so, 40 percent indicate that they frequently (every couple weeks or more) switch to an instrument other than their default option. The most commonly cited reason given for toggling between cards is funds availability, followed by a desire to isolate different purchase types on separate cards and redemption of promotions or discounts.

While the COVID-19 pandemic slowed penetration of some forms of digital spending, the overall trend continues toward greater use of digital options. Innovations in digital payments, like BNPL and cryptocurrency, are also beginning to take root and show the potential for future growth. Consumers tell us that BNPL is enabling them to complete more purchases than they otherwise would. Despite cryptocurrency’s steep growth curve, a high percentage of non-users appear persuadable given further education—although interest to date has been driven by the instrument’s investment potential over its payments utility. Given another year to adjust to the pandemic’s ongoing economic effects, it will be fascinating to see how these digital trends progress in 2022’s survey.

Click here to download a PDF of this article.