COVID-19 is a humanitarian challenge that has shaken the life of nearly every person on the planet. Beyond the pressing personal and public health questions, it has also upended the day-to-day business and financial lives of companies and fundamentally changed client and employee behaviors. Accordingly, the distance economy, emphasizing remote working, omnichannel customer self-service, and digital interaction all are likely here to stay. With respect to private banking, the crisis is expected to bring a dramatic shift for an industry that for generations has valued private and in-person contact with clients.

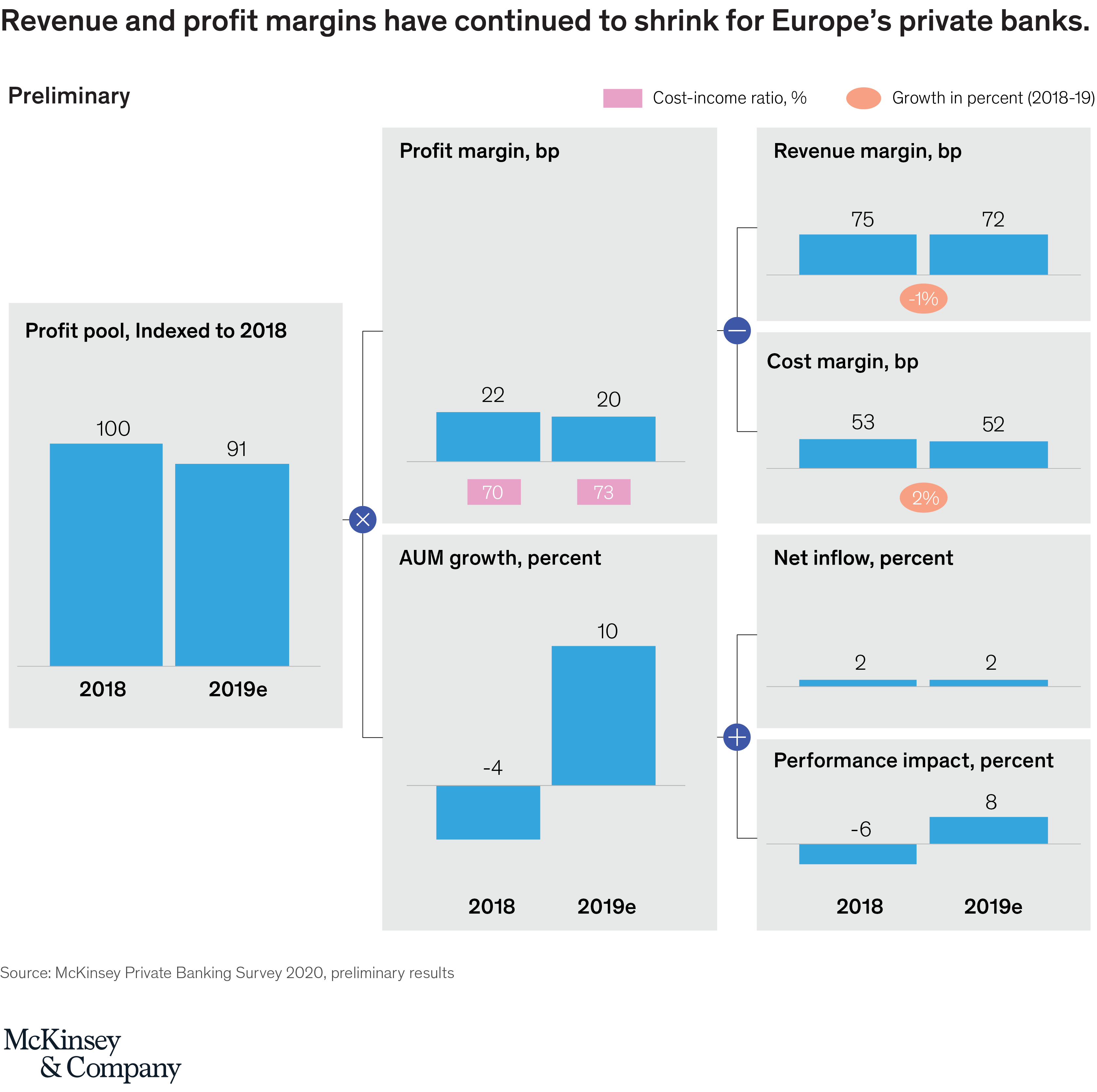

While early indications from first quarter of 2020 suggest that some private banks may have briefly earned higher management fees on pre-crisis assets under management (AUM), and benefited from increased trading activity as the crisis took hold, there is little doubt that the industry will continue to grapple with the significant pressures of the pre-COVID 19 environment—not to mention fresh challenges—especially since it enters 2020 with a difficult starting point. Despite a ten-year bull run that fueled client asset growth, private banks have realized steadily declining revenue margins for the past seven years (dropping to an average of 72 basis points of AUM for 2019); rising cost-to-income ratios (at 73 percent, reaching their highest level since 2009); and shrinking profit margins (from a high of 37 basis points of AUM in 2005 to roughly 20 basis points). These are all preliminary results of McKinsey’s 2019 European Private Banking Survey (Exhibit 1).

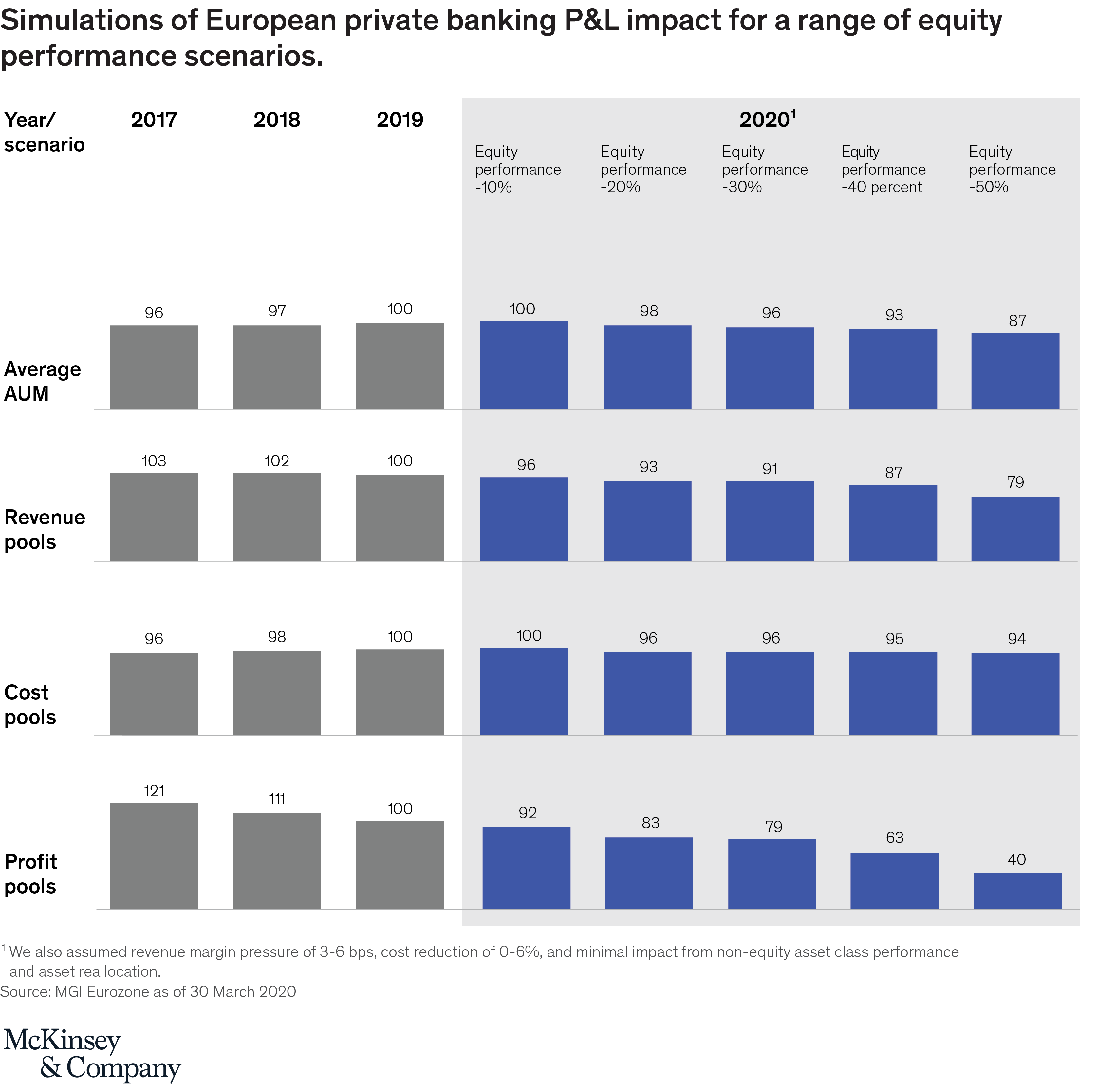

We have explored a range of potential outcomes in 2020 with equity performance ranging from -10 to -50 percent and corresponding assumptions on revenue margin pressure and cost decreases (Exhibit 2).[1] While we expect private banking to show greater resilience than the more capital- and credit-intensive retail and commercial banking sectors, we nevertheless see significant potential impairment in revenues and profits for private banking in 2020. For example, in a -40 percent equity performance scenario, average industry AUM could contract up to 7 percent, leading to a drop in the revenue pool of up to 13 percent, and a sharper drop-off in profits of up to 37 percent.

Looking further ahead, the industry will likely face the double headwinds of falling revenues and rising costs. A lower post-correction client asset base may lead to reduced management fees, while sustained low interest rates will narrow lending margins, and investors will be cautious in returning to the risk markets (especially in lower wealth segments). And while these pressures will have an impact on revenues, headcount reductions will likely be muted at least in the short-term, even though significant investments will be required to succeed in a new normal. This dynamic will lead to a widening divergence between industry leaders and the rest, sparking consolidation (willing or unwilling), especially among subscale firms with less than €10 billion AUM.

This unprecedented crisis can also lead to positive change in all aspects of private banking. Sound personalized advice is more relevant than ever for clients, as they seek to protect and rebuild their portfolios for the next generations. Significant cost savings realized from cutbacks in travel, facilities, and bespoke events can be channeled to much-needed investments in productivity enhancement and digital capabilities.

We suggest a number of actions private banks can make now, while preparing for sweeping strategic moves, as the industry adapts to the new normal, to macroeconomic uncertainty and market volatility, and to changing customer and employee behavior.

- Reinforce client interest in digital servicing and interaction, through a series of short-term digital channel deployments to broaden client reach and enhance client experience. Examples include videoconferences, self-service banking, continuous and personalized digital advice powered by advanced analytics, and greater cybersecurity and privacy risk protection.

- Prioritize target segments for growth, even in a recessionary environment, and win them with differentiated value propositions, integrated user journeys, and premier service and innovative products (implemented through growth “war rooms” and risk-return management).

- Support employees in more productive remote working, by offering relationship managers tailored virtual learning programs in sales excellence, and digital workbenches. Launch automation at scale, beginning from high-volume low-value tasks, especially where it can reduce the need for the physical presence of employees.

- Develop forward-looking high-level initial target business and operating model prototypes that reflect the new and safer ways of working called for in the post-COVID-19 environment. Review the bank’s geographical footprint to identify locations that can be closed or scaled down, keeping in mind that most jobs can be done remotely, or through distributed teams.

- Start building the bank’s investment budget by scrutinizing planned operating costs and investments, in preparation for both economic uncertainty and opportunities to invest for growth.

Full results of McKinsey’s 2019 Private Banking Survey will be published in summer 2020, and will include discussions of strategic priorities enabling private banks to thrive in the post COVID-19 environment.

The authors would like to thank Rashi Dhingra, Ankit Khandelwal, and Ishani Rajpal for their valuable contributions to the survey.

[1] We also assumed revenue margin pressure of 3 to 6 basis points, cost reduction of 0 to 6 percent, and minimal impact from non-equity asset class performance and asset reallocation.