As banks pursue digital adoption to improve efficiency and customer experience, they must navigate evolving customer preferences for different channels for different needs. In some cases, customers embrace new technologies for their convenience. In other cases, they cling to old ways of doing business out of habit or simple resistance to change. According to McKinsey’s latest Retail Banking Consumer Survey of 45,000 consumers in 20 countries, these cross-currents are forcing rapid changes in the way banks connect and cultivate relationships with their customers.

We found that the digital channel is increasingly important, even in countries that have been slower to adopt digital. In Italy, for example, more than two-thirds of customers now use digital channels. Meanwhile, in countries where digitization has advanced more swiftly, more than 85 percent use them (Exhibit 1).

As a consequence of higher digital adoption, customers are visiting branches less in every county we surveyed. In Germany, for example, the percentage of people visiting a branch once a month declined from 60 percent in 2012 to 31 percent in 2018, while in Sweden it dropped from 27 percent to 8 percent. Overall, customers are more and more likely to use digital channels and reserve their branch visits for special advice, to solve complicated issues, or to purchase complex products such as mortgages.

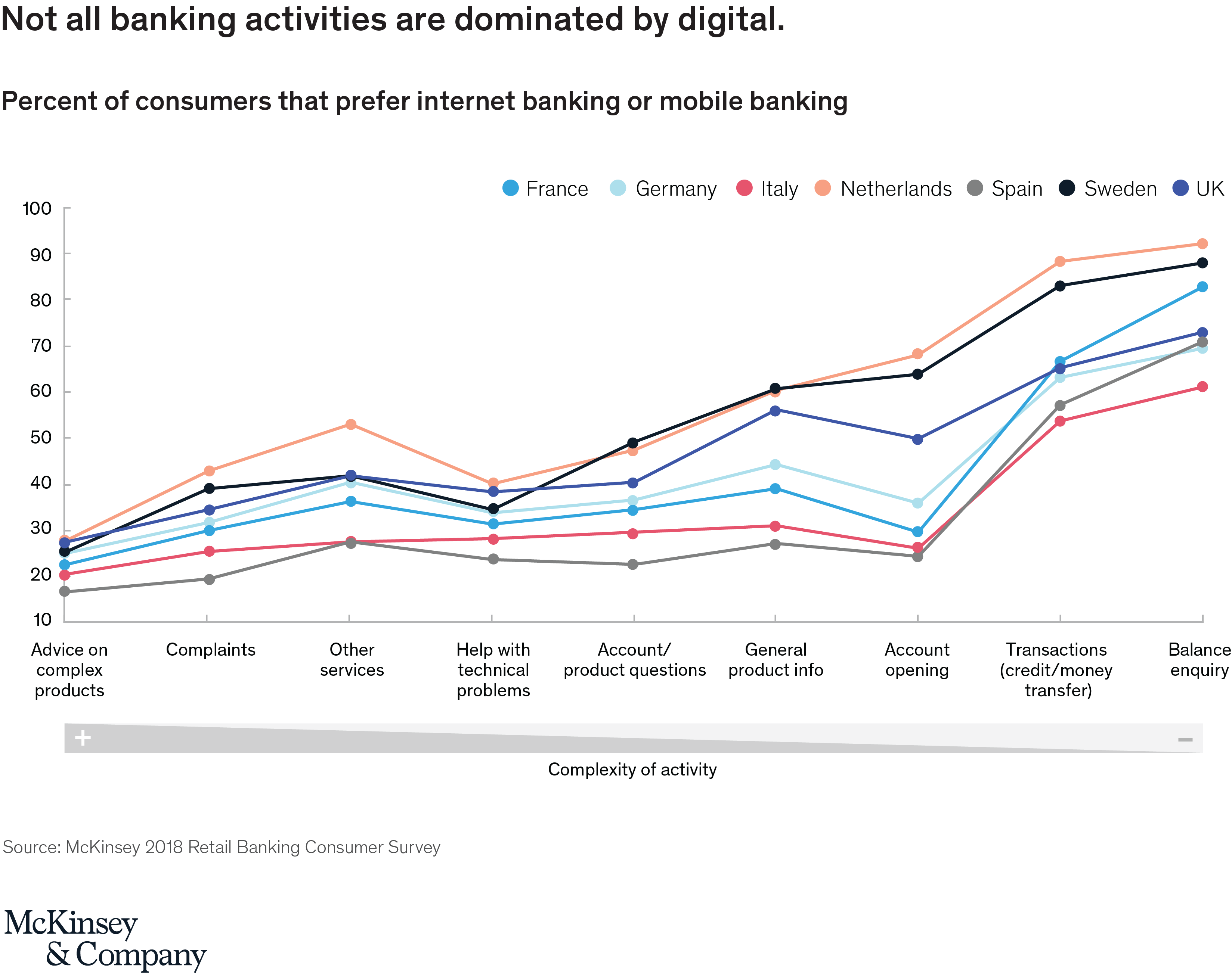

But while branch traffic is down across the board, digital does not dominate all banking activities (Exhibit 2). The physical branch still plays an important role. Besides being a place people can go to interact face to face on complex issues, having a nearby branch is one the major factors customers consider when choosing a bank. In 2018, according to McKinsey analysis, 91 percent of new bank customers in Western Europe came through the branch, while in North America that number was 77 percent.

The bank-channel story would be relatively straightforward if customers simply preferred digital channels for daily, routine transactions and the branch for account openings and the occasional complex product or service. But the reality is more nuanced. Customers are increasing channel agnostic, jumping between channels to solve problems and get answers. They are also embracing digital channels enhanced by human interaction. A prime example of this evolving behavior is the increasing use of remote advisory over the phone and internet when supported by professional relationship managers (RMs).

While these trends are broadly true across the regions we surveyed, different countries are at different stages of digital adoption—even in Western Europe—and so the on-the-ground realities will vary. The Nordic countries, for example, tend to have the most advanced digital offerings, while some of the countries in Southern Europe still rely on extensive branch networks. But there is room for improvement everywhere when it comes to running channels efficiently and delivering excellent customer experience. We see four actions banks can take to better orchestrate their channel interplay and create a next-generation distribution model for customers:

- Push remaining simple interactions to digital channels by increasing customer education. Particularly in countries where extensive branch networks still exist, such as Greece, Italy, and Spain, many simple transactions still occur at the branch. Migrating these transactions to digital channels will require educating customers and employees. Banks need to educate customers on how and why to use digital channels, especially customers 50 and older, who also usually happen to be a bank’s most profitable customers (and could be even more profitable). But banks also need to educate employees who often resist embracing digital channels because they worry about digital channels making their roles redundant. Banks need to explain that digital channels will relieve them of the most mundane tasks and free them to work on more complex, high-value activities for the bank and for customers.

- Deploy new modern branch formats that leverage digitization to enhance the customer experience, thus increasing loyalty and satisfaction. As the branch evolves from a place to do transactions to a place focused on customer acquisition and advice, branch formats need to evolve. Some forward-thinking banks are already rolling out branch designs that encourage customers to sit in a welcoming space, converse with RMs about a product or service, and when possible interact with the new technology and learn how to use it. The idea is to offer an experience not just a sales floor.

- Embrace new human-digital channels such as remote advisory. Many customers are happy to have a conversation from the comfort of their own homes. Interestingly, those in our survey generally did not want video-conferencing. They were more comfortable not being seen. The real game changer for remote advisory seems to be screen sharing. The ability for the RM and the customer to have the same view vastly improves the experience. For banks, remote advisory is a terrific way to balance capacity needs since RMs can be centrally located and don’t need to be in branches. Remote advisory got its first real foothold in the Nordic countries but is now expanding rapidly. For example, in Sweden, the percentage of consumers who received remote advice jumped from 25 percent in 2016 to 44 percent in 2018; in Germany it rose from 19 percent to 33 percent; and in the UK it increased from 29 percent to 36 percent.

- Focus on digital marketing and support capabilities to boost online product sales such as credit cards and personal loans. Banks need sophisticated capabilities to trigger online offers at the perfect moment, and to recognize when a customer who has already been preapproved requests a loan. Even if a bank gets this timing right, it still needs to ensure a simple and seamless customer experience that’s fast and intuitive. What makes this undertaking even harder is that instead of having these customer interactions within the bank’s secure digital channels, the bank is competing on the open internet with other banks as well as digitally savvy nonbanks.

We expect the trends identified in this year’s survey to continue. Consumers will embrace digital and hybrid channels while visits to the branch will further decline. What will set banks apart is their ability to optimize these channels and aggressively vie with a wide array of traditional and nontraditional competitors.