Banking utilities are significant value creators for banks, whether they are designed to optimize a bank’s cost base or provide a new solution unavailable on the market. Utilities tend to develop along a common lifecycle. Creation by a group of banks is the first stage, followed by core business development and establishment on the market, through to business expansion.

Once this third stage is achieved, we have seen an increasing number of utilities change their shareholding structure. Over the past decade, several banks have divested their utilities, moving towards a pure customer role and turning utilities into companies with a more commercial orientation.

We conducted an analysis of 12 real case studies from the payments utility sector and identified four main triggers for divestment: strategic aspiration, regulatory requirements, financial benefits, and governance conflicts. We have also observed banks selling their shares to two types of operator: financial operators (i.e., long-term investors, or the public as IPOs), or industrial players, retaining only partial (or even zero) control within the utility itself. Later in the article, we outline the key requirements for banking utilities to succeed as standalone entities.

Utilities, a value creator for the banking sector

Over recent years, the banking sector has faced continuous margin pressure and challenges from the market (such as competition from fintechs), increasing the need for cost reduction. As also discussed in McKinsey’s Global Banking Annual Review 2019, the impact of traditional cost-cutting initiatives is shrinking, calling for effective alternatives. Shifting non-differentiating activities to industry utilities is a powerful way for banks to optimize their cost base, and has been used to create powerful industry-wide players in several core domains in financial services, be it in payments processing, securities handling, or other forms of network management.

Banking industry utilities are companies typically created by competitors who collaborate to form a jointly owned provider that can supply important commoditized services. They act on behalf of a representative set of industry players, mostly using standardized, modular solutions via a single core technology and operations infrastructure. Industry utilities usually share a number of characteristics:

- Are established by competing firms to perform shared function(s) centrally

- Serve a broad membership base, typically defined along industry lines

- Customers are also “owners”

- Set rules and criteria for membership

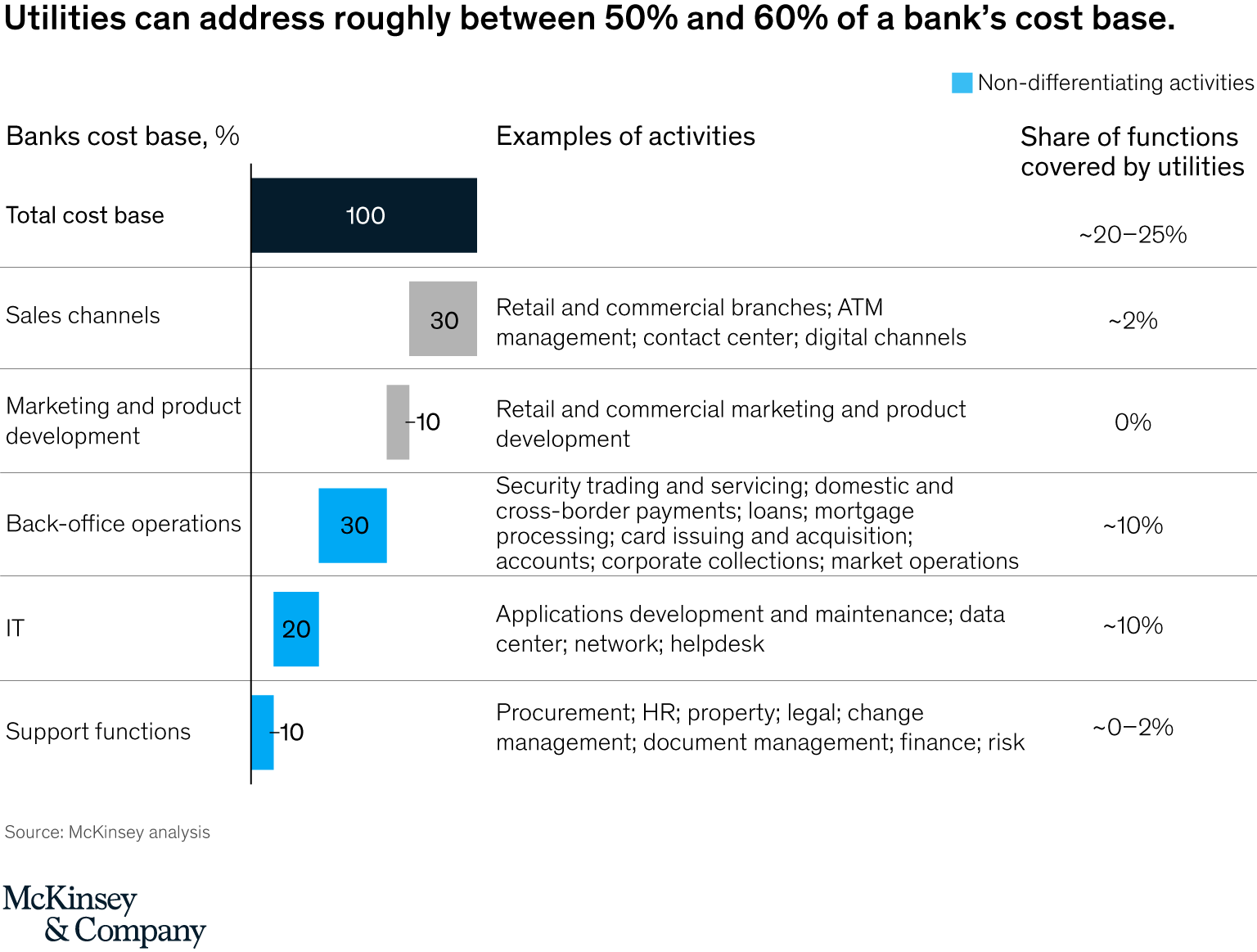

Banking utilities form the middle point of a continuum of external sourcing options ranging from full outsourcing to external provider. Today, existing operators address approximately 20 to 25 percent of a bank’s operating costs, but their potential extends to 50 to 60 percent of a bank’s cost base if taking into account the full set of non-differentiating functions (Exhibit 1).

In the banking sector utilities are often presented as an effective cost-optimization solution. However, their potential goes far beyond cost reduction: utilities generate network effects, that is, multibank interoperability, and favor the pooling of resources, expertise, and capabilities to support the development of banks’ offering to clients. This can be seen in the very first utilities, whose origins go back decades. Visa, for example, was born in the seventies from the transfer of BankAmericard from Bank of America to an association of banks with the aim of enhancing the growth of the credit card scheme (launched in 1958). Mastercard was created in the late sixties by an alliance of bank associations to provide an alternative to BankAmericard. SWIFT was founded in the 1970s by a group of roughly 240 banks from 15 different countries for an entirely different purpose: to develop a solution for cross-border payments, which were not available at that time.

Utilities are highly relevant in banking. However, they are organizations with complex governance and competitive positioning. There is reasonable justification for their creation when the following conditions are in place:

- Collaboration among market competitors will generate a reduction in risk and/or liquidity needs

- The activity the utility would handle is not a source of competitive advantage

- Provision of the service is a natural monopoly because of the inherent economies of scale and skill involved in delivering the service

- There are no trusted alternative providers

Utilities development along a common lifecycle

The creation of industry utilities has gained speed more recently, fueled by the growing need for cost optimization. The common utilities lifecycle is characterized by three main stages. The first is the setup of the utility, followed by developing and establishing the core business on the market. The third stage is expansion of the business into additional markets.

Utility setup

The creation of utilities is driven by banks willing to outsource non-differentiating activities for cost optimization or to leverage network effects to develop standardized solutions for the banking sector.

Utility creation is still an ongoing trend, highlighting the relevance and benefits generated for banks . Recent examples include TruSight, a third-party risk assessment company founded in 2017 by American Express, Bank of America, JPMorgan Chase, and Wells Fargo; and PensionsInfo, which offers back-office services in the field of pension funds and insurance, founded by a group including all Danish banks, and planned to launch this year.

There are three main approaches to creating an industry utility:

- Greenfield: A group of banks creates a new utility from scratch, mostly leveraging internal sources (e.g., MasterCard, Bankgirot, SIA, P27, Nets, TruSight).

- Spinoff from banks: A group of banks founds a utility by transferring an existing platform or solution already in place in one or more banks to the new company, similar to the carve-out of a business unit (e.g., Visa, Nexi and Euroclear).

- Partnership with an industrial company: A technological provider collaborates with a group of banks to enhance an existing solution or develop a new platform (e.g., SIX, IHS KY3P).

Banks are a driving force in utilities setup across all three approaches observed. They represent not just the founders but also the owners and customers of utilities, underlining the utility’s significant dependence on the banking system, particularly in the initial development stages.

Core business development

Once created, utilities focus on their core business, developing standard solutions for their banking customers. As utilities are created to respond to a specific common need, they usually specialize in a single activity.

The typical governance model in this phase is unchanged: usually, banks are owners and customers, and influence the development of products directly triggered by their specific needs.

Business expansion

A third stage sees utilities undergo a further expansion, broadening their portfolio offering or entering new geographies. Once this third stage is achieved, an increasing number of utilities reflect on a more standalone future. Indeed, this further step is usually supported by changes in ownership structure, inorganic growth (M&A), or both.

For instance, banks transferred the ownership of Nets to private equity firms to provide the utility with “a new owner with the expertise, commitment, and financial resources to develop the business in a rapidly changing payments industry” (Peter Lybecker, Chairman, 2014). Similarly, Nexi was transferred to private equity firms with goals including consolidating payments providers across Italy and launching M&A activity. A different model has been adopted by Worldline, which became a pan-European leader for payment services mostly through the acquisition of other utilities.

Accelerating change of ownership

When utilities achieve maturity, owners and managers start thinking about the next stage of evolution. In a scenario of increasing competition, market consolidation, and booming digitization, evolution and innovation are key requirements for utilities to succeed.

At this stage, several utilities have experienced a change in the role of banks, shifting from a user-owner role to an (almost) purely customer role, decreasing their presence within utilities’ capital and leaving the floor to financial or industrial operators. Indeed, starting with First Data in 1992, then Mastercard in 2006, and accelerating over the past decade, banks have been divesting a substantial subset of their commonly owned utilities globally.

Divestments have been occurring for all types of operator, from national operators such as Nets (100 percent shares sold to a consortium of private equity firms by 186 bank shareholders), Banksys and Equens (sold by banks to the public payments company Worldline), or Prisma (majority stake of Argentina’s payments processing system sold to Advent International), to global schemes such as Mastercard and Visa. The latter two were founded by banks and then listed on the public market, with financial institutions retaining minority shares. Other capital markets infrastructures such as the London Stock Exchange (LSE) and Euronext were demutualized and then IPOed. LSE for example, moved from a user-owned model to a new model based on transferable shares to foster a focus on customer needs and flexibility to respond to market evolution.

Building on our analysis of 12 real cases from the utility payments sector, we have identified four main triggers for utility divestment by banks. We have also investigated who banks sell their shareholdings to and what role they retain after divestment.

Four main triggers for utility divestment

The acceleration of ownership changes suggests that business development, also defined as strategic aspiration, could be just one of the triggers for a shift in the role of banks in industry utilities. Other rationales relate to regulatory, financial, or governance issues:

- Strategic aspiration: The first trigger is the desire to boost utility growth and competitive positioning, commercializing products to non-shareholder customers and/or widening the reference market (in terms of products, customers or geographies), or to invest in new technologies and innovation as an answer to changing market demand. For example, Visa’s IPO aimed also at freeing the utility from the constraints of a not-for-profit member-owned association, hence commercializing its network and becoming more competitive on the market; similarly, Nets transition to private equity owners aimed to provide the company with a clear strategic vision to foster its development.

- Regulatory requirements: Another important rationale is the advice or requirement to change the utility’s capital structure to limit antitrust risks, such as collusion between banks or foreclosure of third-party providers. The UK Payment Systems Regulator, for instance, required a reduction in banks’ shares in Vocalink to limit the risk of negative impact on competition and innovation.

- Financial benefit: The desire to capture substantial financial upside to improve profit margin, or to refund the utility’s debt, are further reasons for divestment. The full divestment of RBS’ shareholding in Euroclear to Intercontinental Exchange Holdings generated about €275 million for the leaving bank, for example, reflecting its plans for asset reduction, while the acquisition of Nexi by private equity funds allowed the company to reduce its debt.

- Governance conflicts: Governance-related reasons might include the need to smooth complex decision-making processes (“hung board”) or resolve misalignment of interests between banks with differing relevance within the utility, or between owning banks and the utility itself. Also, banking owners may want to shift to alternative providers on the market or smooth their relationship with the utility. For instance, 13 Euroclear’s shareholders asked to divest from the utility and benefited from a buy-back program.

Two main types of operator on the buy side

Banks may decide to sell their shares (partially or totally) to different types of operators. The buy side is populated by financial operators attracted by a growing business or by industrial operators aiming at becoming a well-established leader on the market by broadening their offering and customer base as well as entering new countries. The first question is therefore whether to sell to a financial or an industrial operator. In the case of a financial operator, the choice is between private placement with long-term investors or an IPO:

- Financial operator: One approach is sale to a long-term investor. This involves private placement with a financial operator (e.g., private equity and investment funds) dedicated to the development of the company acquired and to the accrual of its market value. This is the case with Nexi’s first change of ownership: banks sold 100 percent to a consortium with the aim of improving profitability and fostering growth through innovation and acquisitions. Another option is the public offer of company shares, transforming the company from private to public. An IPO also often comes as a second step after acquisition by long-term investors, who go public to raise capital to finance investment and foster growth.

- Industrial operator: This option involves merger with another utility. Acquirers are utilities seeking to broaden their product, customer, or geographic coverage, or leverage technological synergies to attain a leading position in the payments industry.

Differing levels of divestment

By divesting, banks shift from ownership and a controlling role to (almost) purely a customer role, with decreasing presence within the utility’s capital. However, opening up capital to new entities does not imply complete loss of control. Indeed, banks can opt for partial divestment as a way to retain control over the utility or to achieve a gradual and smoother exit:

- Full divestment: Full divestment involves transfer of 100 percent of shares to a new owner. Full divestment usually implies a loss of control over the utility, with original bank shareholders switching to a “pure customer” role. This is the case with Nets (2014), whose ownership was fully transferred from a membership of Nordics banks to a consortium of private equity firms. This was subsequent to a strategic review indicating that the user-owned model was no longer adequate to grant the necessary investments for further growth in the payments market.

- Partial divestment: Partial divestment entails transfer of a proportion of the shares to a new owner, retaining majority or minority shares. Partial divestment allows banks to retain a certain level of control over the utility. Euroclear is a case in point: despite divestment of all or part of their shares in Euroclear by a number of its owners, banks kept control over the clearing house. In other cases, partial divestment is part of the deal structure that requires original shareholders to retain some of their shares for a fixed period or simply allows for a smoother change.

A new business model: Four requirements to succeed as a standalone entity

Change of ownership brings about a shift in a utility’s way of working, which can lead to several benefits if supported by organizational and managerial evolution.

As standalone market players, divested utilities tend to abandon “cost-plus” and “user-owned” logic. Indeed, banks become customers that purchase the utility’s products and services at market prices, choosing among different alternatives. Divested utilities that were previously focused on minimizing costs for users move to a profit-making model with the goal of maximizing returns. Divested utilities can also explore opportunities to serve customers beyond their previous ownership, broadening their client base. Demutualization is therefore likely to have a positive impact on utilities’ margins. Real cases from MasterCard, Visa, and Nets show that the utility’s performance improves after divestment: they generally experience an acceleration in revenue growth and an improvement in EBITDA margin (an increase of 10 to 25 percentage points).

There are four main areas that independent utilities should focus on to capture the divestment upside and beat competition:

- Clear value proposition: Standalone utilities require a sharper unique selling point and value proposition to be compelling and competitive on the market, as customers will no longer be automatically fed through from owner banks.

- Strong change-management plan: A cultural and mindset change towards a more commercial orientation in the way a banking utility functions is also crucial to sustain a customer-focused value proposition. Cultural change must cascade down from top management and embrace the whole organization through the setting of clear and concrete targets and the development of strong performance management.

- Significant capability-building program to sustain innovation: Newly divested utilities need to strengthen their product development and business planning skills together with their ability to understand customer requirements, sustain innovation, and modernize their core offering. Banking utilities also need to develop strong pricing and commercial skills to be competitive on the market and capture a wide set of customers.

- Ambitious plan for further growth: Divested utilities should have an ambitious plan for evolution also supported by inorganic growth. M&A is a powerful way to accelerate capability buildup and tap into consolidation opportunities. After its IPO, Mastercard acquired around 15 companies in 10 years, integrating both new product offerings and capabilities.

The acceleration of payment utilities divestment from banks is being driven by a broad range of rationales. Our research suggests that changing the ownership structure of utilities is often a key step for mature operators to achieve the next stage of evolution. It is only investment in innovation and strong product development capabilities that allow utilities to be competitive on the market. Financial and industrial operators seem better placed to drive this change thanks to the resources and technical skills they generally have access to, enabling them to flank or replace banks in the governance of utilities. Standalone utilities should focus on the four key areas described to sustain the transition towards a more commercial role and ensure they capture their full potential.